Real estate markets: lending is not heightening risk

Since 2010, loans for house purchase in Germany have seen a positive growth trend, which has again picked up markedly in recent months. Housing prices have also risen in the same period. Economists fear that the distinct increase in loans for house purchase will add more fuel to the real estate price rises in Germany and could thus foster exaggerations in the real estate markets. They are also discussing whether banks' credit standards could have encouraged the price rise in the real estate market. The Bundesbank's economists are now issuing the all-clear signal for lending policy.

According to the Bundesbank, the most likely reason for the increase in loans for house purchase was the robust housing demand among households, which was boosted by historically low interest rates and households' healthy income and asset situation. This assessment is also backed by the results of the Bank Lending Survey (BLS), a Eurosystem survey of banks' lending business, which reveals that demand for loans for house purchase has seen very dynamic growth, while credit standards have not been loosened.

Growth rates comparatively moderate

Bundesbank analyses show that the growth rate for loans to households for house purchase accelerated distinctly in the past year. In December 2015, an annual growth rate of 3.5% – the highest increase in more than 13 years – was recorded. By historical standards, though, the current growth rates are fairly moderate – the long-term average is just under 5%. In the mid-1990s, loans for house purchase in Germany even saw annual growth rates of 11%, when tax incentives were offered as part of the efforts to reconstruct eastern Germany.

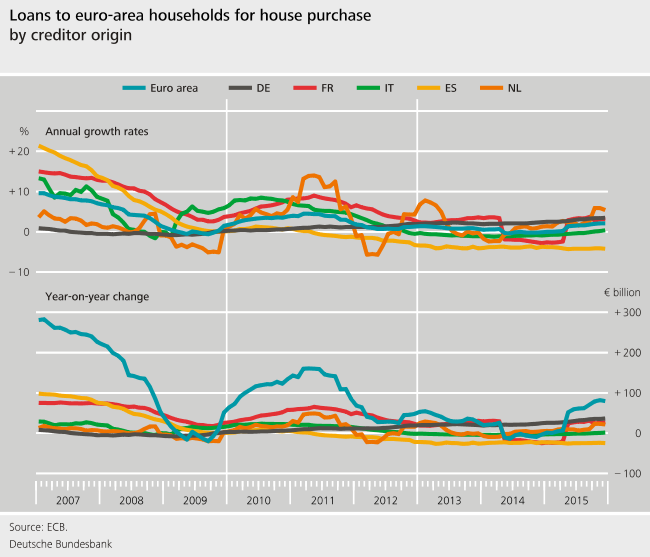

Compared with other European countries, too, the current development in loans for house purchase in Germany is not unusual. In terms of both the annual rates and the level of lending, the growth in loans to households was largely on par with France and the Netherlands.

Level playing field

BLS data support the view held by the Bundesbank's economists that it is demand, and not supply, that is providing the positive momentum for loans for house purchases. This is mainly indicated by the banks' responses to questions about changes in their credit standards, ie the general standards for granting credit defined by the bank. This does not include the lending rates – these are set out in the terms and conditions. According to the managers taking part in the survey, banks have kept the minimum requirements for potential borrowers constant as a whole in the past few years, with a slight bias towards tightening. In the course of the recent rise in property prices, they therefore did not take any higher risks when granting loans by easing the requirements for borrowers.

The respondents reported that since the start of the survey, demand for loans to households for house purchases at the German institutions taking part in the BLS was subject to significant fluctuations at times, while credit standards, on the other hand, have hardly changed over the past few years. Before the financial crisis, demand was thus characterised by a number of shorter positive and negative periods of change, before collapsing in 2008. Demand has shown very dynamic growth momentum overall since the beginning of 2009. This prolonged period of growth was driven by favourable housing market prospects, strong consumer confidence and the low general interest rate level. The latter was not examined as a factor until the first quarter of 2015.

Alternative investment opportunities become less attractive

The Bundesbank believes that current framework conditions – historically low interest rates and the funding environment, the dwindling attractiveness of alternative investment opportunities and the healthy income and asset situation – suggest that more credit applicants are ultimately fulfilling the unchanged requirements of the banks. Furthermore, these factors presumably contributed to a greater number of households showing interest in taking out a loan, enabling banks to grant more loans. This assumption is also supported by the fact that the surveyed banks have recorded only minor changes in the share of rejected loan applications, reported in the survey since the first quarter of 2015.