Firms’ returns to scale: new evidence from European firm-level data Research Brief | 73rd edition – February 2025

The advantages or disadvantages firms experience as a result of their size, referred to in the economic literature as returns to scale, are of central importance in many economic models. Increasing returns to scale, whereby unit costs decrease as output volume increases, could explain productivity differences between Europe and the United States. We present fresh evidence on the returns to scale of European firms: most exhibit constant returns to scale, but a non-trivial share also show increasing returns to scale.

Productivity growth has been markedly higher in the United States than in Europe for some time now. One possible explanation for this is that the European internal market is more fragmented than the US market. Despite decades of efforts, there are still numerous legal, physical and cultural barriers to intra-European trade in goods and services. These obstacles could make it more difficult for firms in Europe to grow and to fully exploit the advantages of greater size – referred to in the economic literature as increasing returns to scale. If a firm exhibits increasing returns to scale, its unit costs decrease as output volume increases, making the firm more profitable, productive and competitive. At constant returns to scale, however, unit costs are independent of output volume. The degree to which there are constant, increasing, or decreasing returns to scale is fundamental not only as an explanatory factor for productivity developments, but also for a whole range of other economic relationships, such as the emergence of market power.

As a result of digitalisation, in particular, it is conceivable that minimal growth constraints will be an important factor in business success and that firms will more often exhibit increasing returns to scale. For example, the use of digital technologies frequently entails high fixed costs but comparatively low variable costs, which can make their use more efficient in larger firms. In addition, digital technologies often benefit from network effects, where utility increases along with user numbers. Social media platforms are a case in point: their benefits for each individual user grow as more users join.

Against this backdrop, we provide new, more comprehensive evidence on European firms’ returns to scale. Based on administrative firm-level data from five euro area countries (Belgium, France, Italy, Portugal, Spain), we estimate production functions for almost all sectors of the economy (at the 4-digit, 2-digit and 1-digit NACE levels) over a recent period of time (2008 to 2018), and derive returns to scale from them. By contrast, previous studies typically only had access to data for individual sectors (such as manufacturing), less recent time periods and individual countries (primarily the United States). In addition, we apply a recently developed estimation technique to estimate production functions, which eliminates the shortcomings of other common estimators in identifying parameters. We also extend the estimation procedure in order to allow for imperfect competition.

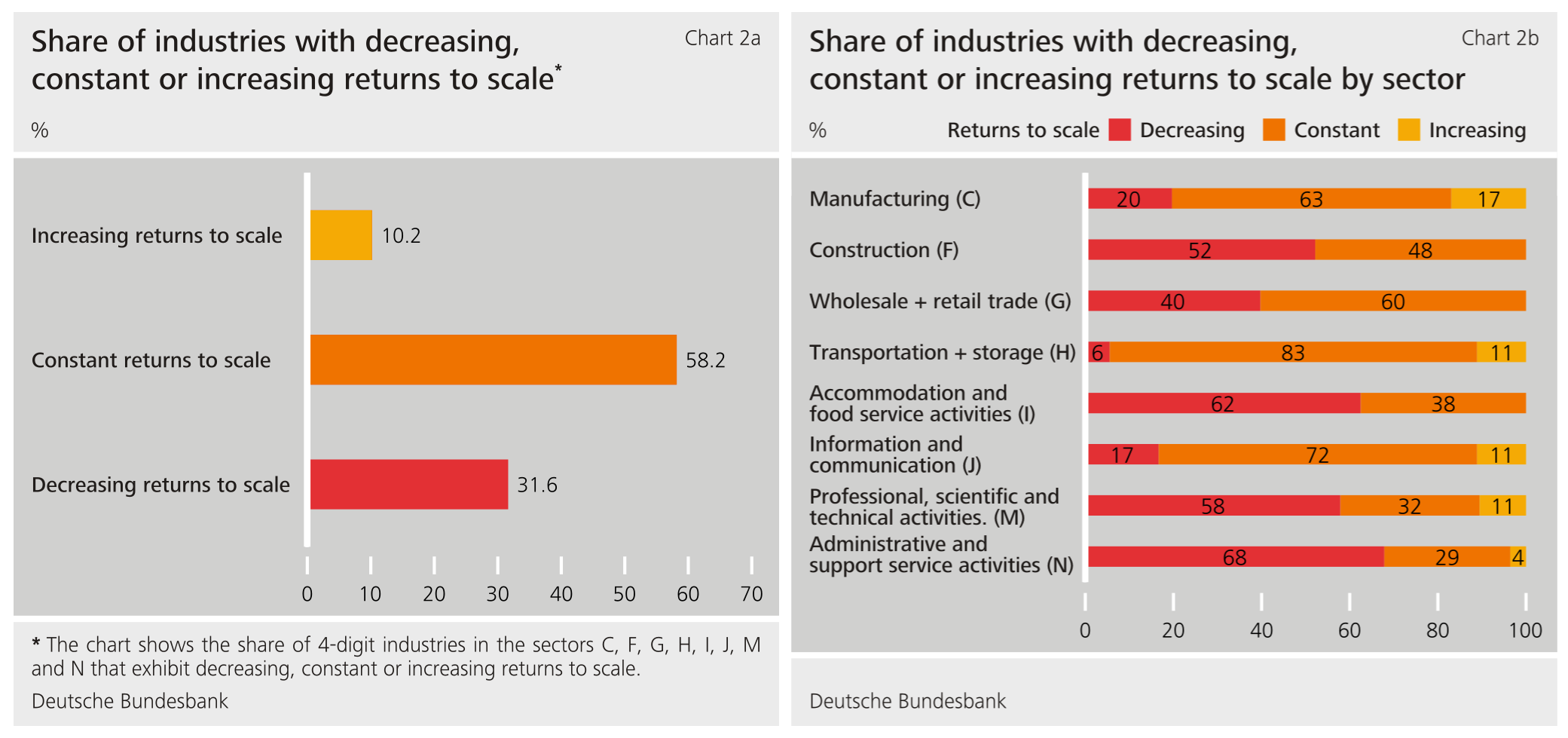

According to our results, the majority of economic sectors typically exhibit constant returns to scale. However, a non-trivial share also exhibit decreasing or increasing returns to scale. This applies to the main results at least, and could be due to a distortion of estimation coefficients. If the estimation procedures are altered to allow for the possibility of imperfect competition between firms, the share of economic sectors with declining returns to scale largely disappears. By contrast, the share of sectors with rising returns to scale increases somewhat. Especially in manufacturing, the transport sector and the IT sector, there are numerous industries with increasing returns to scale. In service industries, on the other hand, there are relatively often decreasing returns to scale.

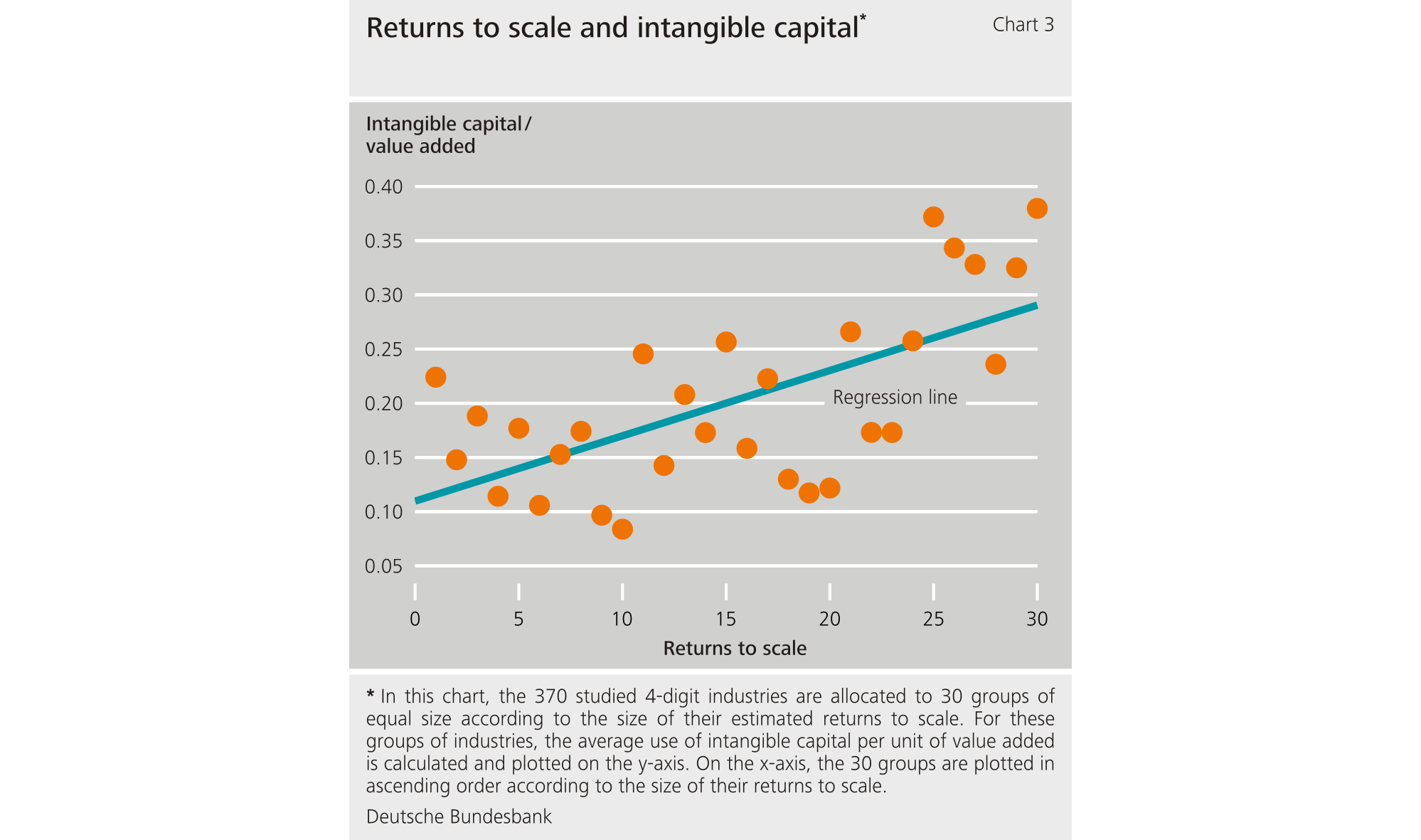

The results also point to a positive relationship between industries’ returns to scale and their use of intangible capital (not only items such as software and databases, but also expenditure on research and development). This is in line with the hypothesis that digitalisation is associated with increasing returns to scale. We also identify a positive relationship between industries’ returns to scale and their trade intensity.

Looking at European and US business statistics also illustrates that, despite the overall markets generally being of a similar size, firms are typically significantly smaller in Europe than in the United States. According to the U.S. Census Bureau, US firms have an average of 20 employees; according to Eurostat, by contrast, EU firms average only five employees. There are also large differences in firms’ market capitalisation. These differences are broad-based across the various economic sectors. However, they are particularly evident in the IT industry, where, according to our results, the share of sectors with increasing returns to scale is also relatively high.

All in all, our results indicate that the majority of firms in Europe show constant returns to scale, but a non-trivial share also exhibit increasing returns to scale. While the research paper does not explicitly investigate the causes of the differences in productivity growth between the EU and the United States, based on our results, it seems quite conceivable that the fragmentation of the European internal market could be dampening the growth of European firms. This applies, at least, to the industries in which, according to our estimates, firms exhibit increasing returns to scale. Here, fragmentation could be preventing firms from fully exploiting returns to scale. These relationships therefore suggest, not least, a need to further deepen the European internal market. This could not only promote growth, but also strengthen the innovative power and competitiveness of European firms at the global level.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

702 KB, PDF