Bundesbank increases risk provisioning

The emergency monetary policy measures taken in response to the coronavirus pandemic have impacted noticeably on the Deutsche Bundesbank’s balance sheet. Given the attendant risks, the Bundesbank has therefore stepped up its provisions for general risks. “This greater level of risk provisioning is the main reason why the Bundesbank is posting a balanced annual result for 2020 and not distributing a profit for the first time since 1979,”

Bundesbank President Jens Weidmann said at the press conference in Frankfurt am Main to present the annual accounts. In the previous year, the Bundesbank distributed a profit of €5.9 billion to the Federal Ministry of Finance.

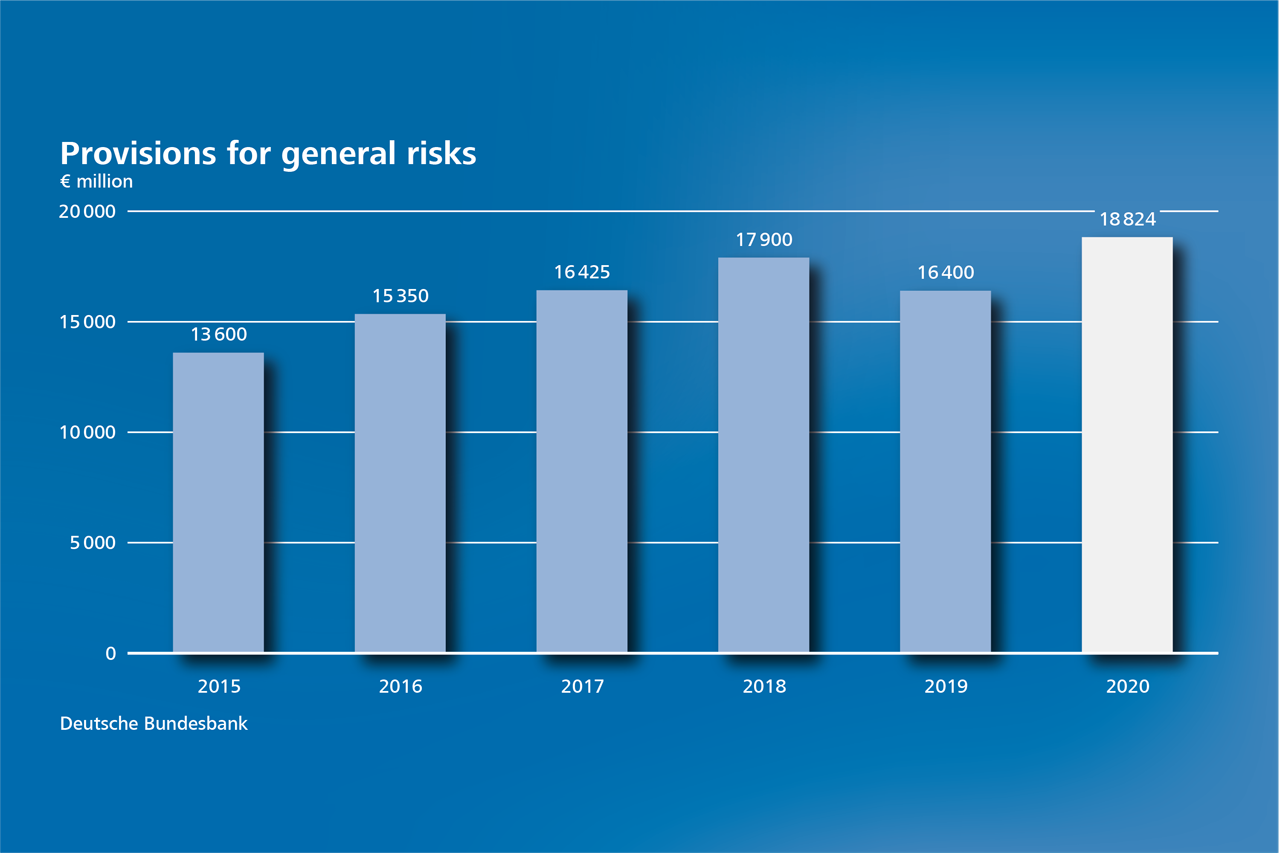

Provisions for general risks were raised to €18.8 billion because the model-based assessment had flagged a considerable increase in risks, with interest rate risk and default risk in the monetary policy portfolio rising, in particular. “That is why, in a first step, we have topped up the provisions for general risks by €2.4 billion. However, this step only goes some of the way towards covering last year’s increase in risk,”

the Bundesbank President explained. “We are therefore expecting another top-up of the provisions for general risks for the current financial year, especially since the risk situation is not likely to change in any major way.”

{kind=link}

{kind=link}

The result for the year 2020 was impacted not only by risk provisioning but also, and in particular, by an increase in interest expense and a decrease in interest income. The Bundesbank was compelled to pay more interest because the emergency measures meant that credit institutions were able to obtain funding from it at more favourable rates and made greater use of this funding option. At the same time, interest income contracted because income from securities held for monetary policy purposes and foreign exchange operations fell and the higher income from the negative remuneration of deposits did not make up for this decline.

Considerable expansion in total assets

As a reflection of the monetary policy support measures and the general uncertainty surrounding the coronavirus pandemic, the Bundesbank’s total assets grew by 42% over the past year. According to Johannes Beermann, the Bundesbank Executive Board member responsible for accounting and controlling, “Not only is the growth rate potentially record-setting, but the figure of €2.53 trillion in total assets is considerably higher than the previous all-time high of €1.84 trillion reached in 2018”

.

On the assets side, it was particularly the longer-term refinancing operations and the pandemic emergency purchase programme (PEPP) which caused the increase in total assets. These were joined by liquidity inflows from other European countries, which caused Germany’s TARGET2 claim on the European Central Bank to surpass the €1 trillion mark for the first time and close the year at €1.14 trillion. On the liabilities side of the balance sheet, the domestic provision of liquidity via refinancing operations and asset purchases combined with liquidity inflows from abroad led to a considerable increase in deposits during the past year.

Higher inflation attributable to one-off factors

At the press conference, Mr Weidmann also addressed developments in the German economy. Owing to the second wave of infections and the measures taken to contain the pandemic, the Bundesbank is expecting a marked decline in aggregate economic activity in Germany for the current quarter. This relapse, however, is set to be considerably less severe than the economic slump observed in the first half of 2020, he said. As soon as the mandatory and voluntary protective measures are gradually lifted, the German economy would be able to get back on the road to recovery. The Bundesbank President emphasised the extent to which the economic outlook hinges on how the pandemic will unfold going forward: “Effective vaccines have been developed more swiftly than widely expected. If these are successful in helping to overcome the pandemic, the German economy will see a lasting recovery.”

Nevertheless, he sees the outlook as remaining subject to a great degree of uncertainty. At present, it therefore seems improbable to Mr Weidmann that Germany will see a very large surge in demand this year that would exceed the normal level of capacity utilisation in its economy. As things currently stand, however, one-off factors are likely to help push the Harmonised Index of Consumer Prices (HICP) inflation rate in Germany to more than 3% by the end of the year, although only temporarily. “For this reason, our economists are now expecting an annual average rate of inflation in 2021 that is just somewhat higher than their December forecast of 1.8%,”

Weidmann noted.

Financing conditions still exceptionally favourable

Mr Weidmann also provided context to the recent increase in euro area sovereign bond yields. He noted the monetary policy importance of taking into consideration the overall financing conditions of enterprises, households and general government, which was why many variables were at issue, not just one. The Bundesbank President emphasised the absence of a drastic tightening of financing conditions for enterprises, households and general government. “Financing conditions remain very favourable by historical standards,”

he said, also indicating that not every increase in financing costs was necessarily problematic from a monetary policy perspective. For instance, nominal interest rates could rise if monetary policy were successful in lifting excessively low inflation expectations. “We would naturally not stand in the way of this development,”

the Bundesbank President noted. A more favourable economic outlook could likewise be associated with rising interest rates. Mr Weidmann therefore emphasised the need to closely monitor developments and carefully analyse the background.

Do not blur responsibilities with regard to climate protection

The Bundesbank President referred to climate protection as one of the most pressing tasks of our time, in which time was of the essence. However, care should be taken to ensure that the lines of responsibility separating central banks and politicians do not get blurred. In his view, for central banks in general, three aspects particularly need to be at the fore: comprehensively understanding the impacts of climate change and climate policy, incorporating financial risks, and promoting transparency in this regard. The Bundesbank is working hard at strengthening its analytical capabilities, he added. These efforts included upgrading macroeconomic models in order to explore the effects of climate policy measures, including with regard to inflation and the objective of price stability. In addition, stress tests are planned for the years 2022-23 to capture the impacts of various CO2 price paths on financial stability in Germany. Mr Weidmann added that climate-related financial risks could also affect central banks’ securities holdings, including monetary policy portfolios. Central banks should therefore also integrate those climate-related risks into their risk management framework. In Mr Weidmann’s opinion, it is therefore important in this regard to improve the information base through reporting obligations for securities issuers and standards for ratings. That way, central banks could also help boost transparency surrounding climate-related financial risks in the market.