How the US dollar, as a reserve currency, restricts US trade policy Research Brief | 58th edition – May 2023

The trade dispute between the United States and China in 2018 and 2019 increased trade policy uncertainty, leading to a marked appreciation of the US dollar (USD). The obvious explanation for this is the special role played by USD investments in the global financial system as a safe haven for investors in times of high uncertainty. The USD appreciation triggered in this way in 2018 and 2019 enabled Chinese exporters to lower their prices in US dollars. As a result, the impact of the additional import tariffs imposed at the time by the United States on Chinese products was significantly reduced.

World trade has been rocked by a number of dislocations in recent years. During the pandemic, disruptions in supply chains led to bottlenecks in many places. The Russian war of aggression against Ukraine and the European energy crisis exposed the problems of unilateral trade dependencies. In many countries, increasing consideration is therefore being given to relocating critical production operations within domestic borders (onshoring) and to focusing on trade relations with allied countries (friendshoring). Disentangling the ties interlinking world trade could, especially in view of increasing geopolitical tensions, trigger new frictions between existing trading partners and thus trade policy uncertainty (TPU). The question therefore arises as to what impact rising TPU would have on the affected parties.

As we show in a study (Khalil and Strobel, 2021) for the case of the United States, increases in TPU can surprisingly limit the effectiveness of the country’s protectionist trade policy. This is because, owing to the special role it plays in the international financial system, the US dollar often appreciates globally in times of uncertainty, which partially reverses the effect of US import tariffs.

This relationship was observed in the trade dispute between the United States and its major trading partners – particularly China – in 2018 and 2019. At that time, the United States was accusing many of its trading partners of unfair competition and imposed additional import tariffs, especially on Chinese goods. The aim of this was to make Chinese products more expensive for US customers and make access to the US market more difficult. The average tariff rate on Chinese goods was raised by a total of around 12 percentage points in several stages. China responded with retaliatory tariffs. Interestingly, there was a significant concurrent appreciation of the US dollar – both against the Chinese yuan and against a broad basket of currencies. This, in turn, could have reversed the impact of US protective tariffs, as it reduced the price of imports from China for US buyers. At the time, however, many observers were not paying much attention to the effect from the exchange rate.

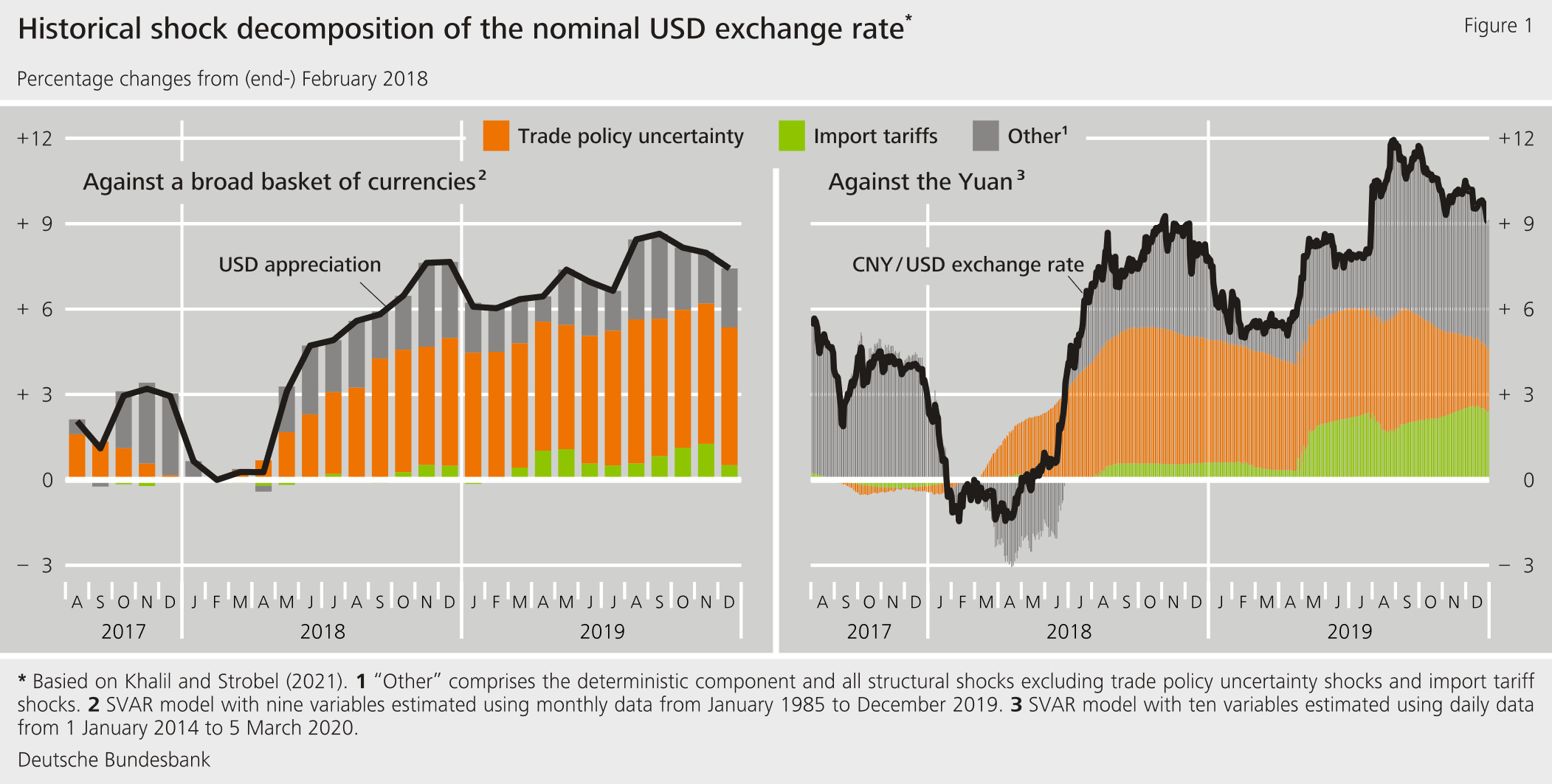

Trade policy uncertainty brings about marked US dollar appreciation

In order to analyse the reason for the USD appreciation at the time in greater depth, we estimate a structural vector autoregressive model, in which we take into account the US import tariffs themselves as well as other macroeconomic and financial market channels. In contrast to previous studies, we also incorporate TPU as a possible determinant. To this end, we use an established measure developed by Caldara et al. (2020) that is based on the relative frequency of terms related to trade policy uncertainty in articles in major US newspapers.

The estimations suggest that the significant increase in TPU associated with the trade dispute was the main reason for USD appreciation. US trade policy at that time was characterised by ongoing disputes with key trading partners. Market participants were finding it increasingly difficult to gauge possible trade policy developments. Decomposing the US dollar’s movements against a broad basket of currencies into the contributions of various explanatory channels shows that the bulk of USD appreciation is attributable to TPU shocks (see Figure 1, left panel). According to this analysis, TPU also played a considerable role in the appreciation of the US dollar against the yuan (see Figure 1, right panel). By contrast, the additional import tariffs actually imposed were of only minor importance.

The role of the US dollar as a global reserve currency is crucial

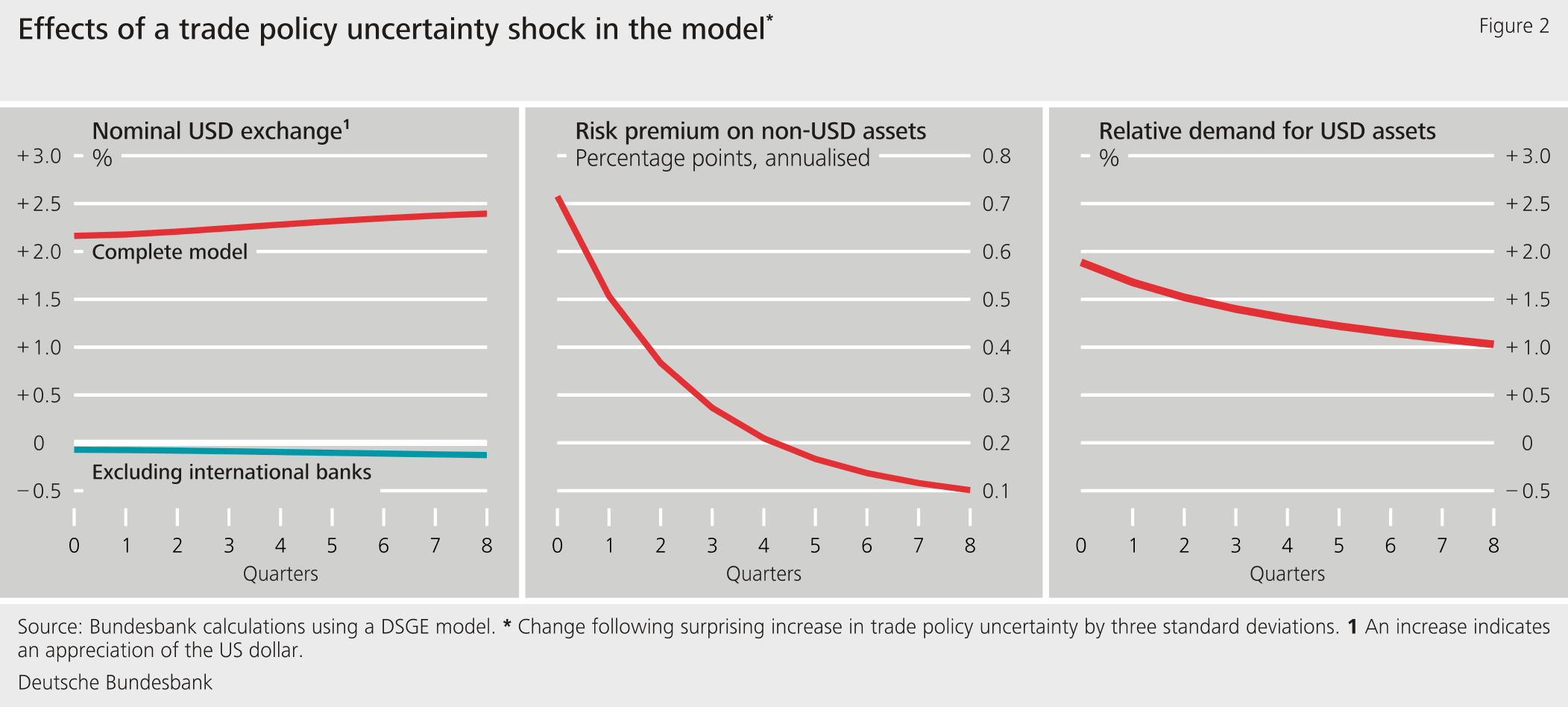

This finding can be explained by the fact that USD-denominated assets are generally considered to be comparatively safe by international standards. We illustrate this in a macroeconomic model comprising two regions (the United States and the rest of the world) with close trade and financial market ties. The governments of both regions can impose import tariffs. TPU is modelled by an increasing expected variance in future tariff paths, while the role of the US dollar as a reserve currency is modelled by a higher collateral value of corresponding assets. A major role is played by international banks that hold financial assets from both regions. Banks’ borrowing is limited by the collateral value of their assets (see Gertler and Karadi, 2013). As TPU increases, financial market prices fall. Banks’ capital decreases and they are required to shrink their balance sheets. They can counteract this by restructuring their portfolio to contain USD-denominated assets. This causes the US dollar to appreciate.

In this model, Chart 2 shows the consequences of increasing TPU of around the scale observed in March 2018. In the model simulation, the relative demand for USD assets increases and banks demand a risk premium on assets from other currency areas. The US dollar appreciates markedly. In a comparison model in which banks are not balance sheet constrained, this channel is not effective (see the blue line in the left panel).

Limited effectiveness of import tariffs in the United States

An analysis with detailed foreign trade data also suggests that Chinese exporters used the scope created by USD appreciation to lower their prices. For Chinese intermediate goods, which were hit particularly hard by US import tariffs in 2018 and 2019, our estimations show that exporters lowered their prices in US dollars by around 0.75% in response to a USD appreciation of 1%. As a result, a large part of the tariff-related rise in the price of Chinese imported goods was offset again.

Conclusion

In an environment characterised by trade policy disputes and rising TPU, the effectiveness of specific trade policy measures such as import tariffs remains limited for the United States. The role of the US dollar as a global reserve currency is crucial in this context. This important transmission channel should not be ignored in trade policy disputes.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Caldara, D., M. Iacoviello, P. Molligo, A. Prestipino, and A. Rato (2020), The economic effects of trade policy uncertainty, Journal of Monetary Economics, Vol. 109, pp. 38-59.

- Gertler, M. and P. Karadi (2013), QE 1 vs. 2 vs. 3... : A framework for analyzing large-scale asset purchases as a monetary policy tool, International Journal of Central Banking, Vol. 9(1), pp. 5-53.

- Khalil, M. and F. Strobel (2021), US trade policy and the US dollar, Deutsche Bundesbank Discussion Paper No 49/2021.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

534 KB, PDF