Monthly Report: How cross-border payments are influenced and the role the German banking system plays in this

Germany is an open economy in which a great many economic transactions are conducted with non-resident counterparties every day. These may be, for example, the export or import of goods, a trip abroad, or the purchase of foreign securities. Every one of these transactions involves a cross-border payment. Being interconnected internationally is very much second nature for people living, working and doing business in Germany and many other countries. The banking system – in other words, domestic monetary financial institutions (MFIs) including the central bank – takes care of the payment side of all cross-border transactions. The current issue of the Monthly Report looks at how different developments within and outside Germany affect the associated liquidity flows.

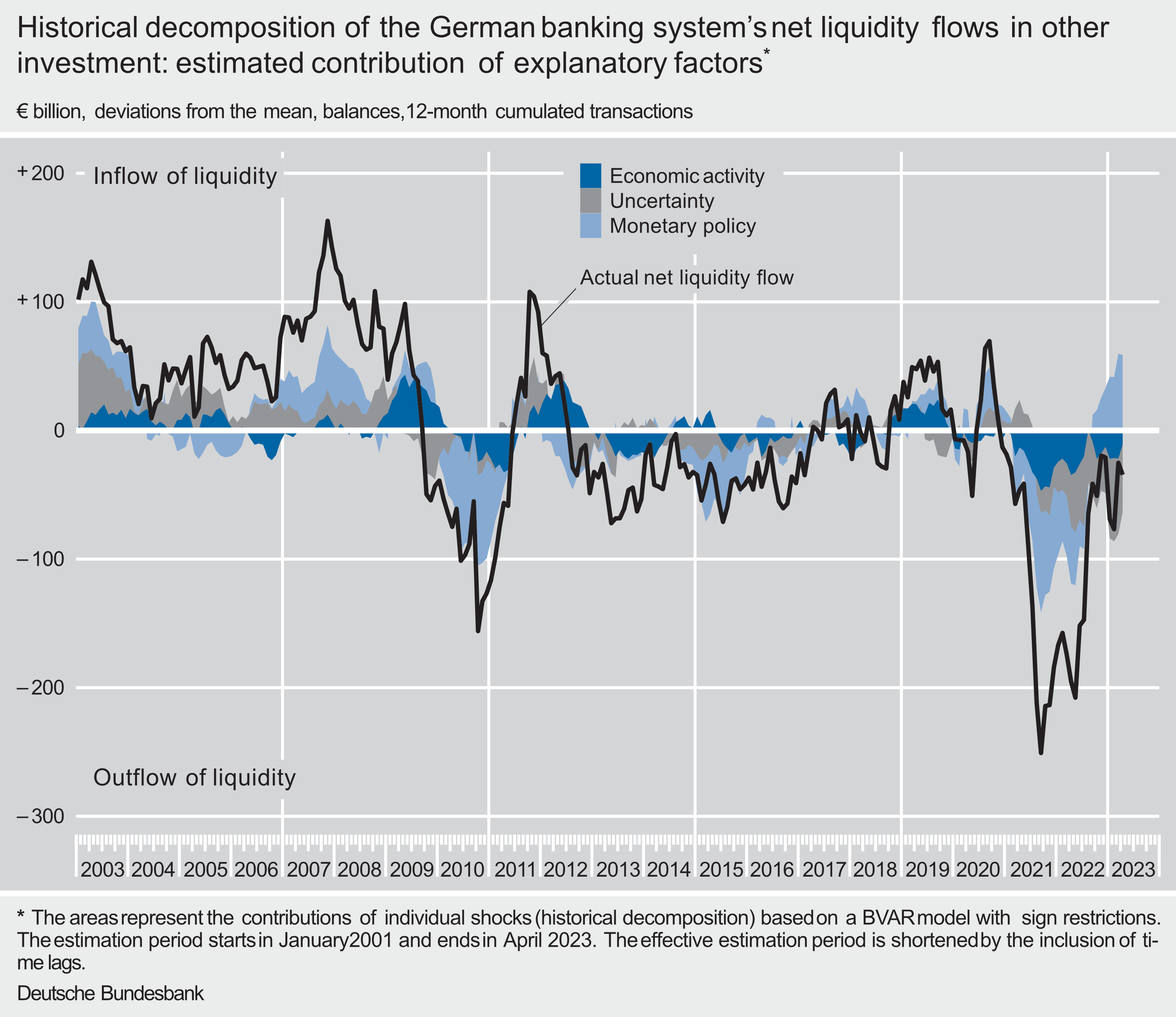

Economic activity, uncertainty and monetary policy are key factors

The economists note that one important driver of cross-border economic activity is economic developments – specifically, how those abroad compare with those in Germany. If, for example, the economy is running better abroad than it is in Germany, they explain, demand for German products rises. Exports of goods to other countries would increase at a brisker pace than imports of goods, making it more likely that current account surpluses will be recorded. All other things being equal, these would involve liquidity inflows via the German banking system.

Sentiment in financial markets is also crucial, according to the report. In a calm market environment, investors are more willing to accept higher risks. In times of heightened uncertainty, however, investors often seek out safe havens in order to hedge against abrupt asset losses. If a global crisis sees demand focus mainly on US securities, liquidity will flow out of the German banking system. Where investors wishing to hold euro-denominated instruments are aiming first and foremost to shield their assets from critical developments elsewhere in the euro area, they focus their interest primarily on German government debt securities. This means that liquidity flows into the German banking system.

Monetary policy also has an influence on cross-border transactions, as outlined in the report. For example, a more restrictive monetary policy – as compared with monetary policy in other parts of the world – has various effects which tend to result in liquidity flowing into the German banking system from other (non-euro area) countries. Monetary policy also plays a role via its effects on the exchange rate, asset prices or cross-border lending.

Using a specialised model, the Bundesbank’s experts examined how the three factors described above – economic activity, uncertainty and monetary policy – are currently affecting cross-border liquidity flows.

In 2021, the economists write, monetary policy and economic activity tended to be conducive to liquidity outflows out of the German banking system. Since mid-2022, however, monetary policy has had a more restrictive effect, once again bringing more liquidity inflows to Germany. Uncertainty and economic activity, on the other hand, have had a dampening effect on cross-border liquidity flows until recently. Russia’s war of aggression against Ukraine marked a turning point in Germany’s external relations and sparked greater uncertainty. This led to increased demand for US securities around the world. The war has also weighed on the German economy and, together with rising commodity prices, caused a drastic reduction in Germany’s current account surplus.

Governing Council of the ECB tightens monetary policy

The Governing Council of the ECB has raised interest rates markedly since mid-2022, in addition to ending net asset purchases under the asset purchase programme (APP). In March 2023, the ECB and the national central banks began to reduce their asset holdings. In the years prior to this, asset purchases for monetary policy purposes had led to strong balance sheet expansion at central banks.

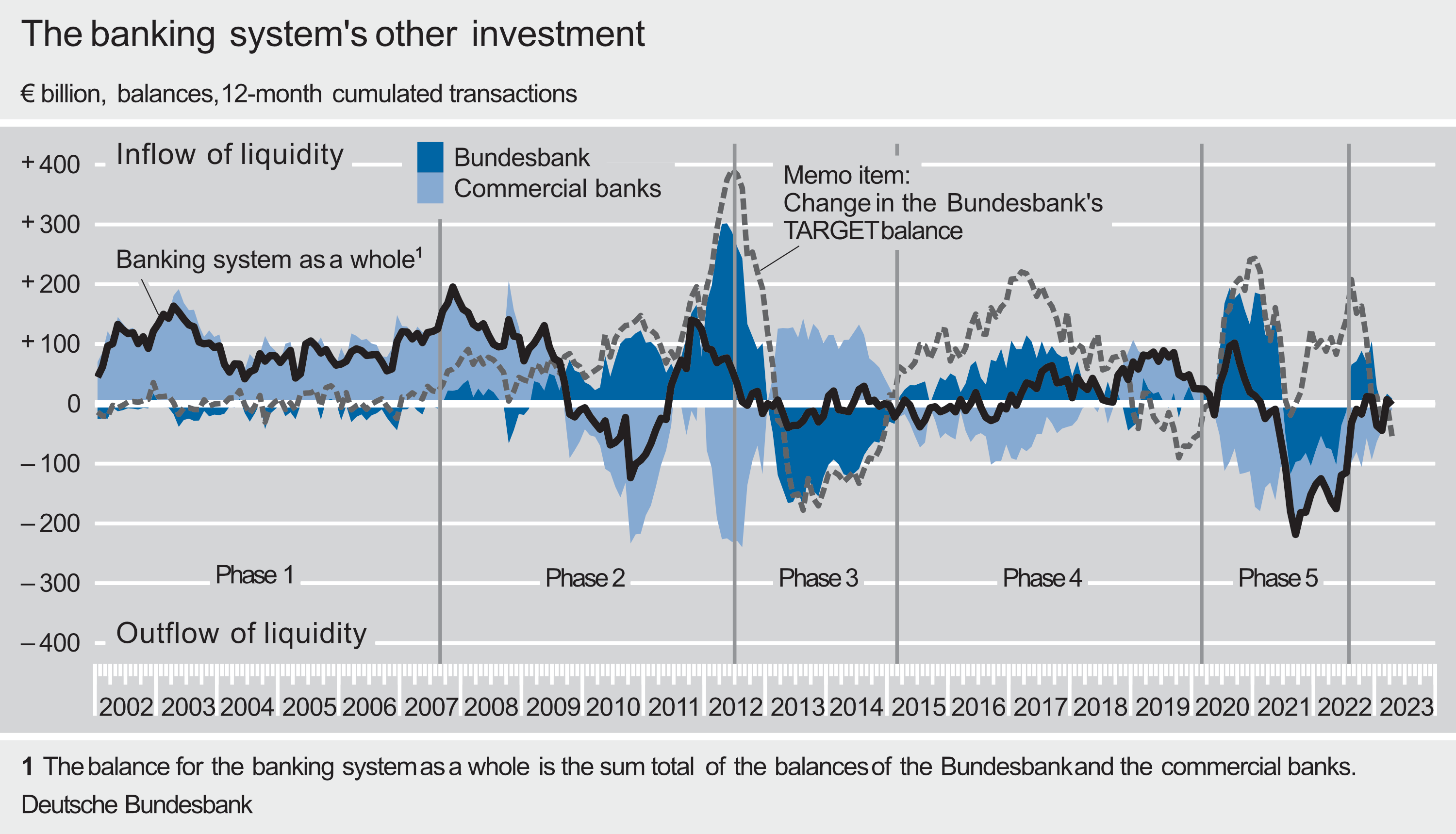

Private interbank market has lost importance since financial crisis

The economists also looked at the allocation of roles within the banking system with regard to cross-border liquidity flows. Up until the global financial crisis, commercial banks provided each other with sufficient funds in the private interbank market – including across borders, they write. However, the private interbank market became less important with the onset of the financial crisis and the sovereign debt crisis in certain euro area countries. Since then, liquidity provision by central banks has played a greater role, including in cross-border capital flows. The report therefore concludes with the message that the Bundesbank advocates reducing excess liquidity in the Eurosystem. It would then once again increasingly fall to commercial banks to lend funds at market conditions, and allocate scarce resources in this way. This is a clear affirmation of the market economy system, in which this task generally falls to private agents.