The effects of government support measures such as the gas price brake Research Brief | 67th edition – July 2024

Energy prices skyrocketed as a result of the Russian war of aggression. Government stabilization measures such as the gas price brake were intended to support overall economic development. Our study compares the effects of two fiscal stabilization measures for companies: subsidies in the form of quantity-limited price guarantees and production-independent direct transfers. It turns out that the effectiveness of the measures depends on the availability of the good.

Energy prices skyrocketed as a result of the Russian war of aggression. Government stabilization measures such as the gas price brake were intended to support overall economic development. Our study compares the effects of two fiscal stabilization measures for companies: subsidies in the form of quantity-limited price guarantees and production-independent direct transfers.

The Model

In our study (Hinterlang et al., 2024), we use a multi-sector macroeconomic model with endogenous market entry and exit through a competition channel. The model represents the interconnections between 53 production sectors, including clean and brown energy. All sectors use gas as an essential input factor. Gas is assumed to be fully imported. Apart from that, the economy is closed. The model is calibrated for Germany.

Simulations of fiscal measures

In a baseline scenario, we first simulate an exogenous increase in gas prices without fiscal policy measures. We assume that the price temporarily rises and returns to the original equilibrium after the shock. The basic production structure and energy efficiency do not change due to the shock. Then, we simulate two policy measures under two different assumptions regarding gas prices and supply. For both measures, the level of support is set at 70 percent of the previous gas consumption of the respective sectors. The level is based on the measure taken in Germany in the form of transfers.

- Measure 1: Quantity-limited price guarantee (subsidy). Each sector receives 70 percent of its pre-crisis gas consumption at the original price. The remaining consumption must be purchased at the current market price. The measure reduces average production costs (through the subsidized gas price). For modelling reasons, we assume that average production costs are relevant for the production decision of companies. Deviating from this assumption, for example because the marginal price played an important role in the decision-making process, could lead to the incentive effects of both measures being closer together. This is because companies would consider the subsidy below the 70 percent threshold as a transfer.

- Measure 2: Transfers based on initial consumption levels. Companies receive a sector-specific transfer. This is fixed for each company and compensates for the difference between the market price and the original price for 70 percent of pre-crisis gas consumption. This has no direct impact on production costs and therefore not on the production decision, which depends on the gas price.

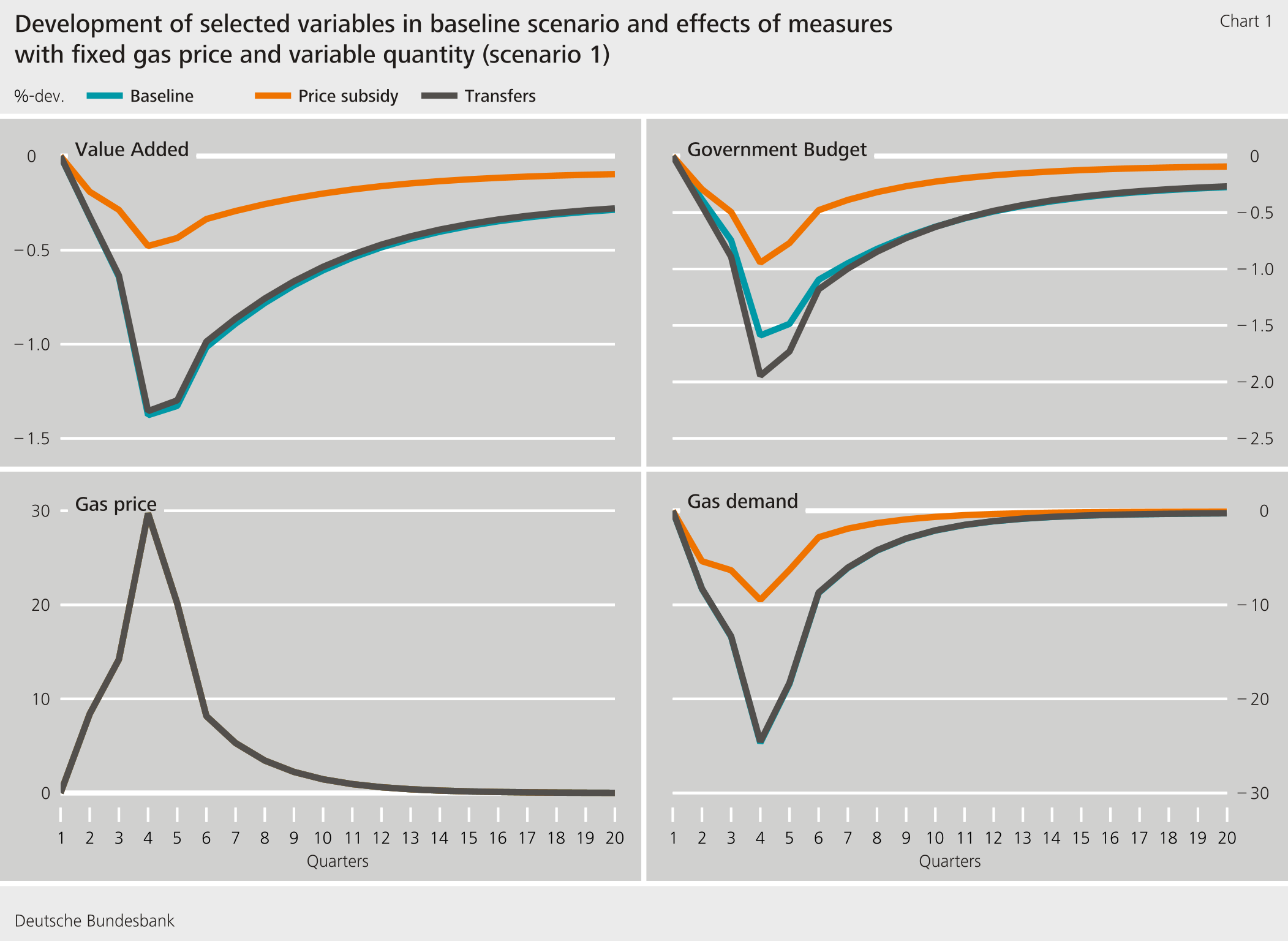

Sharp price increase in the baseline scenario

Chart 1 shows the paths of the baseline scenario (petrol) and the effects of the measures (transfer in grey, price guarantee in orange) with variable gas quantity. In the baseline scenario, the import price for gas rises steeply. The demand for gas decreases significantly (largely without affecting the gas price). Consumption, investment, and overall economic production decline. Industries that consume a lot of energy suffer particularly.

Price guarantee provides stronger stabilization in the case of fixed reference prices

In this case, we assume that the gas price (after the shock) does not react to the strength of domestic gas demand, but the quantity is variable (elastic supply).

The subsidy of import prices for gas leads to a strong increase in gas demand and production compared to the baseline scenario (Figure 1), as the measure reduces average costs for gas consumption. Under the above assumption, these costs are crucial for the company's calculation. The incentive to save gas decreases. Consumption, investment, and production are significantly stimulated. The measure partially finances itself.

In contrast, direct transfers to companies have only minor effects on production and gas demand compared to the baseline scenario. Although more companies remain in the sector (due to fewer bankruptcies), which reduces price premiums and prices. However, since the support measure does not target the gas price itself, it has a comparatively small effect on production. Gas demand only increases slightly, as the incentive to save gas remains largely intact.

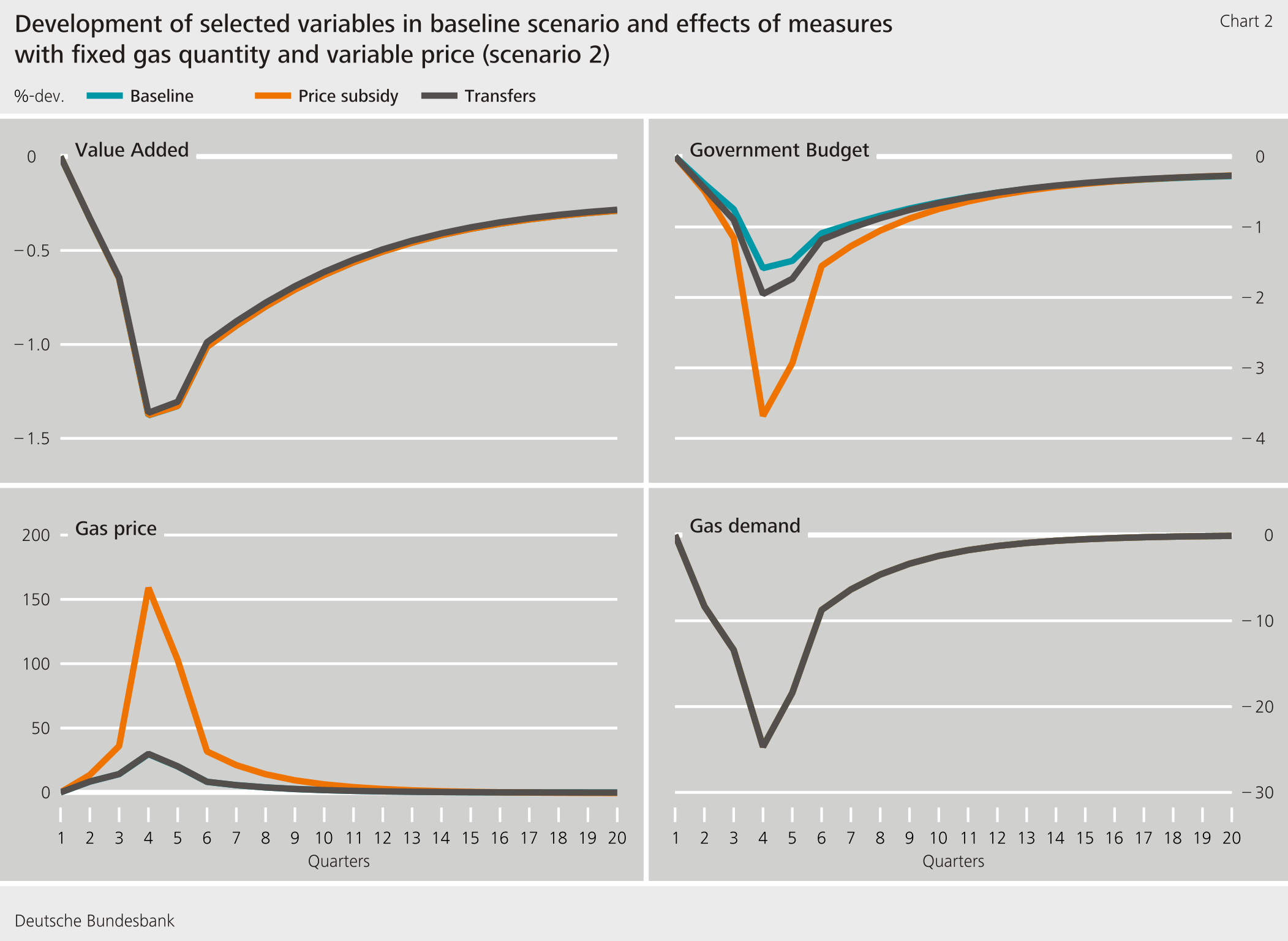

Transfers provide stronger stabilization in the case of fixed delivery quantities

In this case, we assume that the gas supply is unchanged (inelastic supply) and the gas price must adjust.

Chart 2 illustrates the effects when the gas supply does not respond to demand. In this case, the subsidies further drive up the gas price because the incentive to save gas is greatly reduced. The sharp price increase further hampers production in energy-intensive industries. The fiscal support largely dissipates in a price effect (which benefits the gas-supplying foreign countries). At the same time, the government's costs for subsidies increase immensely, which in turn has a negative impact on private household budgets and overall economic demand. Direct transfers do not have these problems. The incentive to save remains intact, and the gas price does not rise further. Production continues to be slightly stabilized, as bankruptcies are avoided. Therefore, in such a scenario, direct transfers to companies are the economically more sensible policy measure.

Conclusion

The results show that the effectiveness of differently designed stabilization measures depends crucially on the scenario, in our case primarily on the availability of natural gas. However, the findings can also be relevant for other important imported goods such as rare earths or microchips. Subsidies for production costs work better in the case of pure price shocks, while direct transfers to companies are preferable in the case of actual scarcity because they maintain the incentive to save. Furthermore, the design of the measures is important. With quantity-limited price guarantees, incentive effects can be maintained if the subsidized quantity is set sufficiently low. The effects of the instruments can also be similar depending on the design and circumstances. The political decision in Germany to pay transfers to companies appears understandable against the background of the uncertain gas deliveries at that time.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

List of references

- Hinterlang, N., M. Jäger, N. Stähler und J. Strobel (2024). On curbing the rise in energy prices: An examination of different mitigation approaches. Deutsche Bundesbank. Discussion paper 09/2024.

| The authors | |

| Natascha Hinterlang Ökonomin, Zentralbereich Volkswirtschaft, Deutsche Bundesbank | Marius Jäger Ökonomin, Zentralbereich Volkswirtschaft, Deutsche Bundesbank |

| Nikolai Stähler Ökonom, Zentralbereich Volkswirtschaft, Deutsche Bundesbank | Johannes Strobel Ökonom, Zentralbereich Volkswirtschaft, Deutsche Bundesbank |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

356 KB, PDF