Connectedness between exchange rates: how machine learning opens up fresh insights Research Brief | 28th edition – September 2019

Are the exchange rates between certain currencies more closely connected than those of other currencies? Answers to this question can be provided by econometric methods. A new study shows how machine learning can deliver useful insights into this issue.

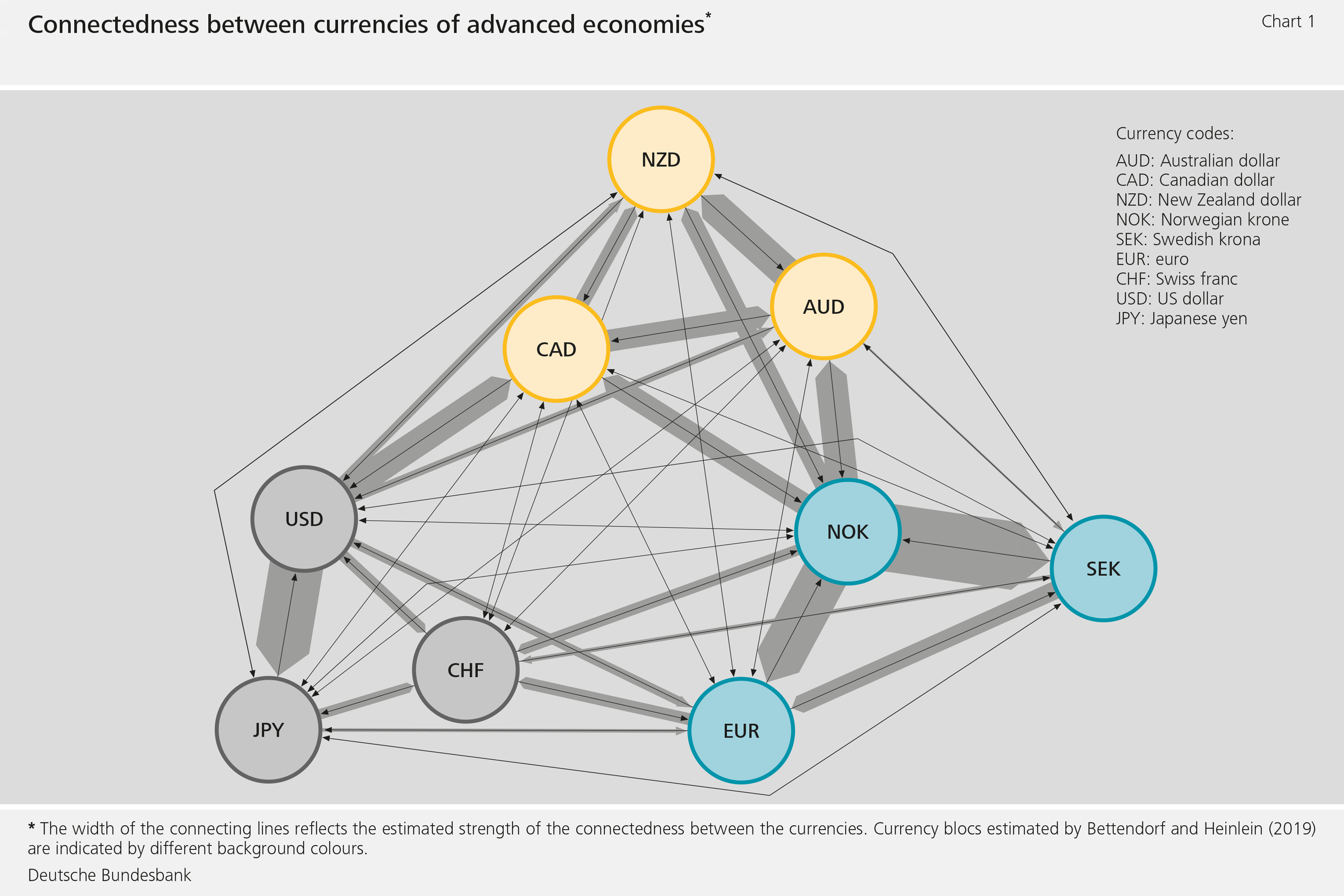

Exchange rates are of major importance for macroeconomic developments and are often a topic of political debate. In a recent study (Bettendorf and Heinlein, 2019), we study how bilateral exchange rates between various currencies are connected. We show that the US dollar and, surprisingly, the Norwegian krone exert a relatively strong influence on other currencies. Such a causal relationship between two currencies exists if the pattern of one currency’s exchange rate can be explained by that of the other currency.

Our study is based on a model inspired by Diebold and Yılmaz (2009). The authors assume that certain economic time series, such as data on different exchange rates, are connected. The pattern of a time series here is shaped by unexpected events – known as innovations or shocks. These events can be assigned either to the time series itself or also to other observed time series, with the shocks affecting the individual series both at the time of occurrence and with a time lag. Statistical procedures (VAR models) can be used to estimate these connections and then to calculate the contributions which shocks to individual time series make to the movement of all the time series under observation (forecast error variance decomposition). These contributions are a measure of how closely the series are connected.

What our study shows is that the results of such an estimation depend, in some cases considerably, on how the contemporaneous relationships between the time series are incorporated. Contemporaneous causal structures, especially, had not been fully taken on board in earlier studies, which is why in our study previously used procedures led to at times considerably biased results. We solve this problem by using an algorithm for machine learning (see Spirtes et al., 2001). This algorithm uses statistical methods to search for contemporaneous causal structures between the variables. These causal structures are thus obtained from the data and not, as in other studies, defined by the user. This means that our study generally models contemporaneous causal effects better than previously applied procedures. Monte Carlo simulations by Bettendorf and Heinlein (2019) likewise indicate that the approach can tend to lead to more precise estimation results, especially with regard to the contemporaneous causal structures.

US dollar and Norwegian krone especially independent

For our study, we looked at ten major currencies from the beginning of 2010 to end-2017: Australian dollar, Canadian dollar, New Zealand dollar, Norwegian krone, Swedish krona, euro, Swiss franc, US dollar, Japanese yen and pound sterling. The pound sterling was taken as the reference currency (the "numéraire"), i.e. all the countries’ exchange rates are each defined as bilateral rates against the pound sterling. We were therefore unable to include the pound sterling itself in the study (for more on this topic, see Bundesbank (2019), pp. 17 ff.).

The results of our study (see Figure 1) suggest that the US dollar and Norwegian krone were relatively independent currencies during the observation period. However, they exerted a comparatively strong influence on other currencies. The Swiss franc and New Zealand dollar, by contrast, barely influenced other currencies. The euro was influenced not only by the US dollar, but also by the Norwegian krone and Swedish krona. The euro itself influenced, in particular, the Swiss franc, which was probably due in significant measure to the temporary introduction of a minimum exchange rate against the euro by the Swiss National Bank.

Whence the strong influence of the Norwegian krone?

The comparatively strong influence of the Norwegian krone on other currencies is a surprising finding. This could potentially reflect Norway’s role as an oil exporting country, as oil price movements could feed into exchange rates. These developments are then misinterpreted as spillover effects. They can also affect exchange rates between currencies which themselves are not classed as commodity currencies. Viewed from this angle, one could argue that the impact of the Swedish krona on the euro is ultimately a diverted effect originating from the Norwegian krone.

Three currency blocs

In a further step, our study uses statistical procedures to cluster exchange rates into currency blocs. The exchange rates of the currencies contained within a single currency bloc show relatively similar patterns, yet follow distinctly different paths to those in other blocs. The observed currencies can be clustered into three groups:

- Safe haven currencies and carry trade financing currencies (Swiss franc, US dollar, Japanese yen): these currencies are regarded as particularly safe and are therefore in demand in an uncertain global economic environment.

- Commodity currencies (Australian dollar, Canadian dollar, New Zealand dollar): these currencies’ economies are key exporters of commodities; exchange rates are therefore heavily impacted by the prices of these commodities.

- European currencies (euro, Norwegian krone, Swedish krona): Norway and Sweden, alongside the euro area Member States, are members of the European Economic Area (EEA). The Norwegian krone is also closely connected with commodity currencies (see Figure 1), yet its connections to European currencies are even stronger.

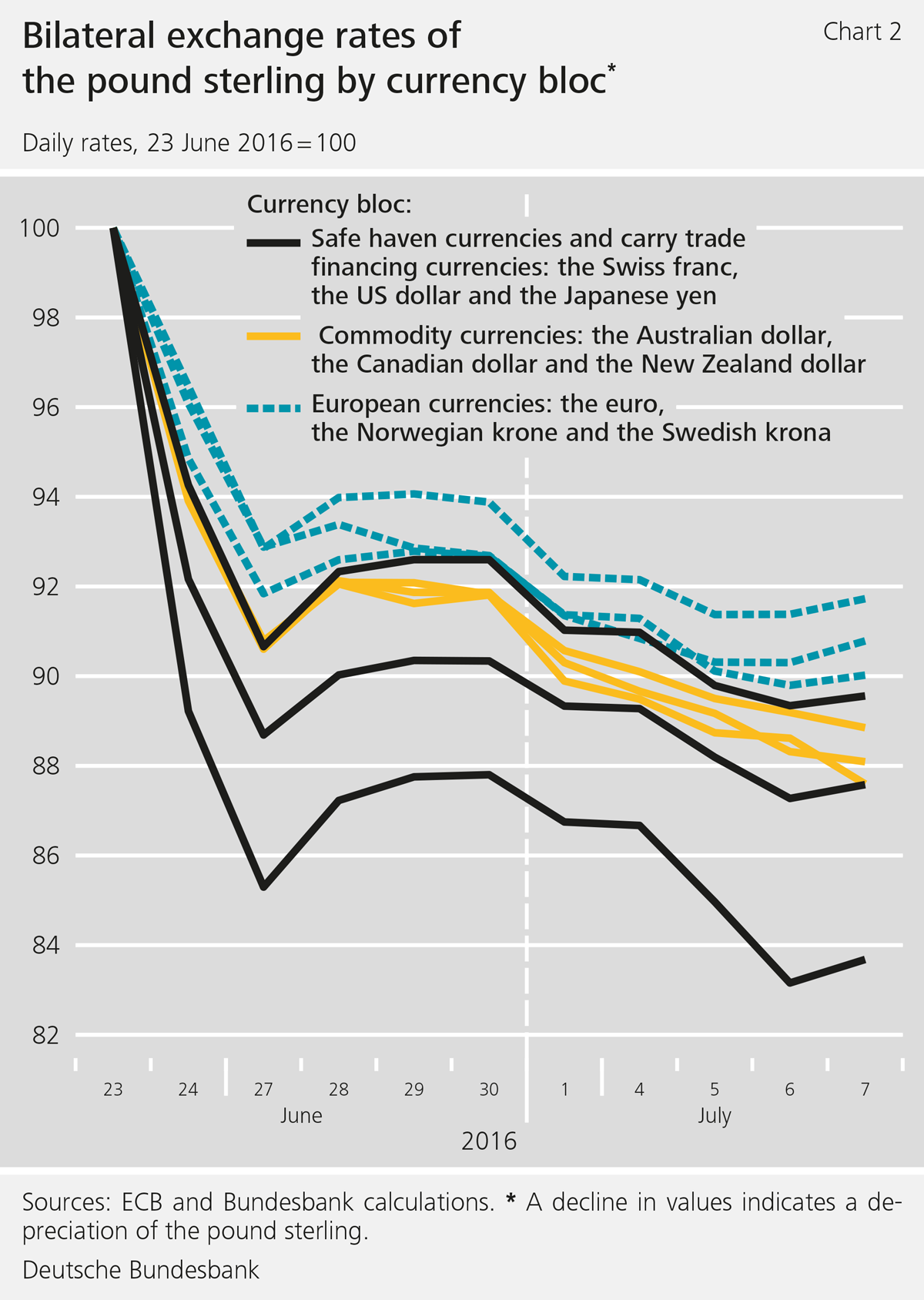

In order to establish whether the identified currency blocs fulfil the above definition, we have taken as an example the paths charted by each individual exchange rate following the referendum on the UK’s exit from the European Union and analysed them. Figure 2 shows the paths of the various pound sterling rates grouped by currency bloc. Although the pound sterling depreciated considerably against all the observed currencies, there are relatively strong relationships in place within and, in some cases, also between the various blocs. The exchange rates of the commodity currencies (bloc 2) and the European currencies (bloc 3), in particular, showed very similar paths.

Conclusion

Our study shows how machine learning can help extract additional insights from a traditional statistical model. We find that the US dollar and Norwegian krone exert a relatively strong influence on other currencies. In addition, we successfully identify three currency blocs whose exchange rates are systematically interconnected.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Bettendorf, T. and R. Heinlein (2019), Connectedness between G10 currencies: Searching for the causal structure, Deutsche Bundesbank Discussion Paper No 06/2019.

- Deutsche Bundesbank (2019), Parallels in the exchange rate movements of major currencies, Monthly Report, July.

- Diebold, F. X. and K. Yılmaz (2009), Measuring financial asset ret urn and volatility spillovers, with applications to global equity markets, The Economic Journal, Vol. 119, pp. 158-171.

- Kilian, L. and H. Lütkepohl (2017), Structural Vector Autoregressive Analysis, Cambridge University Press.

- Spirtes, P., C. Glymour and R. Scheines (2001), Causation, Prediction , and Search, 2nd edition, Cambridge, MA: MIT Press.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

3 MB, PDF