How interest rate expectations respond to monetary policy in a low-interest-rate setting Research Brief | 20th edition – August 2018

In the low-interest-rate setting, the Eurosystem’s accommodative monetary policy has been relying to a greater extent on non-standard measures and forward guidance on the future path of policy rates. A new paper examines how these measures have worked across the term structure and how market expectations have evolved during the phase of low interest rates. The results illustrate that the Eurosystem can continue to influence market participants’ interest rate expectations at the effective lower bound by way of unconventional monetary policy measures.

The Eurosystem reduced its key rates on numerous occasions over the past years and additionally introduced a raft of non-standard measures in an effort to move inflation back towards a level of just under 2% over the medium term. These non-standard measures, which included the monetary policy asset purchase programme (APP) and forward guidance on the future path of policy rates, aimed, amongst other things, to influence expected future short rates and reduce the term premiums priced into longer-term interest rates.

Our recently published Bundesbank Discussion Paper uses a term structure model to explore how these measures impact on interest rates for different maturities in the euro area. This research is based on the overnight index swap (OIS) yield curve. Our model particularly enables us to examine how policy rate changes and non-standard monetary policy measures affect, on the one hand, market participants’ expected future short rates and, on the other, the term premium – that is, the compensation for taking on interest rate risk.

One key element of our model is that it includes an effective lower bound (ELB), which we have calibrated to take into account both current and expected future changes in its level. This means that our model is capable of mapping how policy rates have gradually moved into negative territory since the summer of 2014. Our model estimation also considers short and long-term interest rate surveys to ensure that expectations derived from the yield curve for the future path of short rates are as consistent as possible with the survey results (this topic is also addressed by Priebsch, 2017). This gives us a term structure model which delivers high-quality estimation results, above all in the short-term segment of the yield curve, and simultaneously generates expected future short rates which are economically plausible.

Market participants’ interest rate expectations reflect credibility of monetary policy

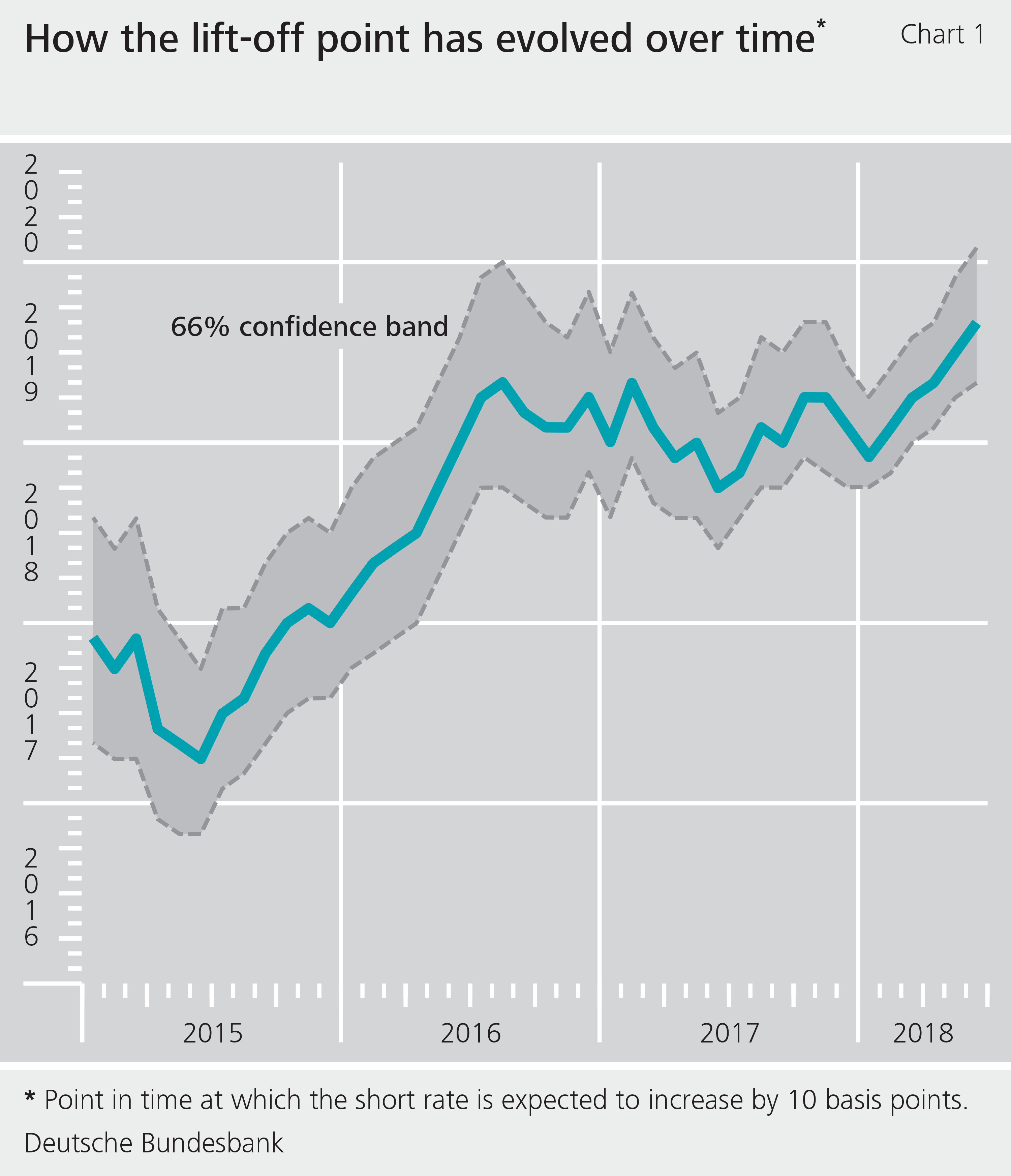

Our model allows us to analyse how market participants adjust their expectations regarding future short rates over time and to identify the point in time at which they most expect policy rates to pick up again. Figure 1 shows how the distribution of this expected lift-off point has evolved. In mid-2015, market participants were expecting to see an initial 10-basis-point hike in interest rates in roughly two years’ time, but as the APP continued and the deposit facility rate was reduced further, this lift-off point gradually shifted into the future. It can be said, then, that the Eurosystem succeeded in prolonging market participants’ expectations about how long short rates would remain low. The expected lift-off point started moving back towards the present day at around the end of 2016. It was during this period that persistently low short rates combined with rising long-term rates to steepen the yield curve. In its June 2018 press release, the ECB Governing Council articulated its assumption that the net asset purchases will be discontinued at the end of 2018 and that key ECB interest rates will remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path. According to our model estimations, market participants believe that an initial interest rate hike at the end of September 2019 is the most likely scenario in the current setting.

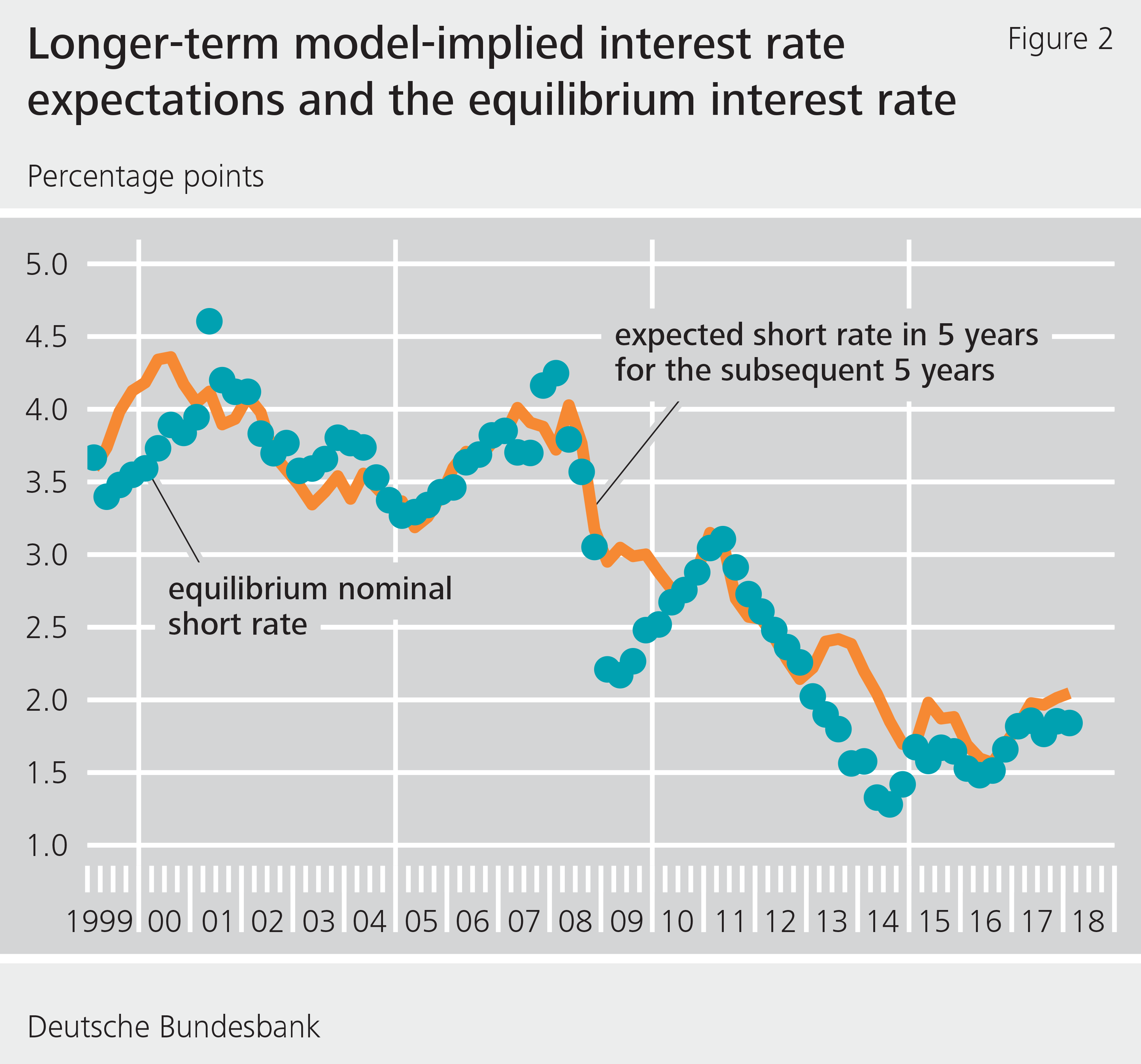

Our model indicates that longer-term expectations surrounding future short rates have declined since the financial crisis in 2008 (see figure 2). This development is much like the path of an equilibrium nominal interest rate derived from macroeconomic models, as estimated for the euro area by Holston et al (2017). The nominal interest rate is said to be in equilibrium when the demand for goods matches the supply of the same over a longer horizon and inflation remains stable. In keeping with the equilibrium nominal interest rate model, interest rate expectations in the longer-term maturity segments of the yield curve are geared to its level. Trends in key real and nominal macroeconomic variables, including developments in an economy’s growth potential as well as inflation, thus appear to have a major bearing on the formation of longer-term interest rate expectations (see also Crump et al, 2018).

How conventional and unconventional monetary policy affects the yield curve

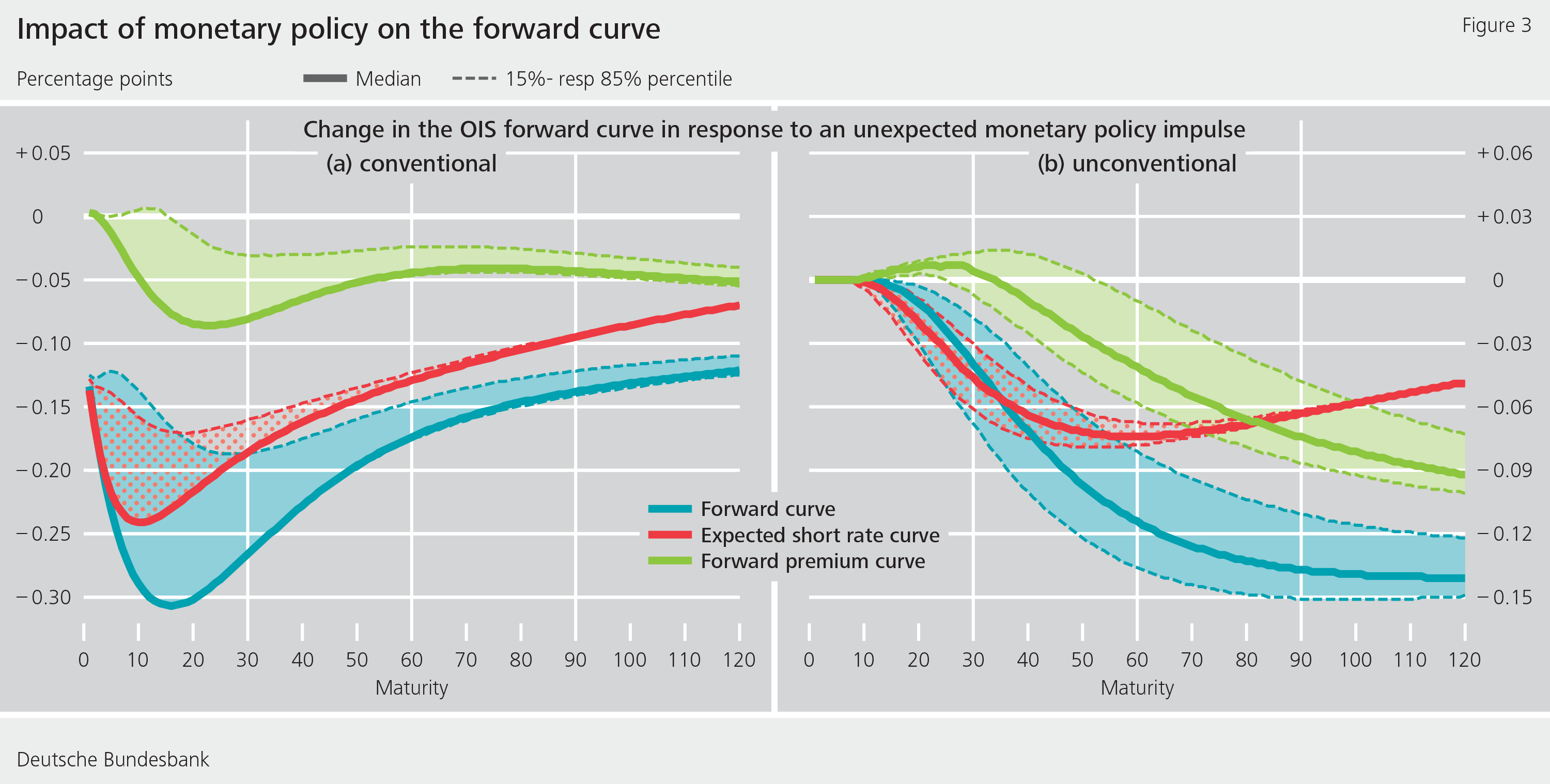

By performing further analyses with our model, we can gauge how the yield curve responds to monetary policy measures, depending on how close interest rates are to the ELB. To this end, we identify conventional and unconventional monetary policy shocks by recording changes in selected financial market prices on monetary policy event days (including monetary policy meetings, speeches and interviews). This reveals that an unexpected cut in the policy rate makes the forward curve, which plots current expectations for short rates at future points in time, significantly steeper (see figure 3a, blue line). The red line shows that declining interest rate expectations in the shorter-term maturity segment of up to two years are mainly to blame – market participants, it would appear, adjust their expectations for further policy rate moves in the same direction. This tells us that conventional interest rate policy includes a communicative component and thus a signal effect as to how short rates are likely to evolve going forward. The more policy rates converge to the ELB, the blunter conventional accommodative monetary policy measures become. This is because the closer policy rates get to the ELB, the more constrained the forward curve will be to the downside, as indicated by the shaded areas in figure 3a.

Another point our analysis reveals is that non-standard monetary policy measures impact on the long-term maturity segment mainly by way of the term premiums demanded in the market (figure 3b, green line). By contrast, interest rate expectations align, especially in the medium-term maturity segment. Altogether, it can therefore be said that non-standard monetary policy exerts a strong and persistent influence on the yield curve.

Conclusion

Our paper develops a non-linear term structure model which can be used to derive insights from data on market interest rates and survey-based interest rate expectations as to how monetary policy measures affect interest rate expectations at the effective lower bound (ELB). Our findings illustrate that the Eurosystem is also capable of influencing market participants’ interest rate expectations at the ELB. The effects of conventional interest rate policy are mainly evident in the expected path of the yield curve, but diminish as the ELB becomes less binding. Unconventional monetary policy, on the other hand, works primarily by changing the term premiums priced into the interest rates for long-term assets.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Crump, R K, S Eusepi and E Moench (2018), The term structure of expectations and bond yields, Federal Reserve Bank of New York Staff Reports, No 775.

- Geiger, F and F Schupp (2018), With a little help from my friends: survey-based derivation of euro area short rate expectations at the effective lower bound, Bundesbank Discussion Paper, No 27.

- Holston, K, T Laubach and J C Williams (2017), Measuring the natural rate of interest: international trends and determinants, Journal of International Economics, 108, pp 59-75.

- Priebsch, M (2017), A shadow rate model of intermediate-term policy rate expectations, FEDS Notes, Washington: Board of Governors of the Federal Reserve System, 4 October 2017.

| The authors | |

Research economist at the Deutsche Bundesbank, Directorate General Economics |

Research economist at the Deutsche Bundesbank, Directorate General Economics |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

3 MB, PDF