Monthly Report: How pension reforms might work

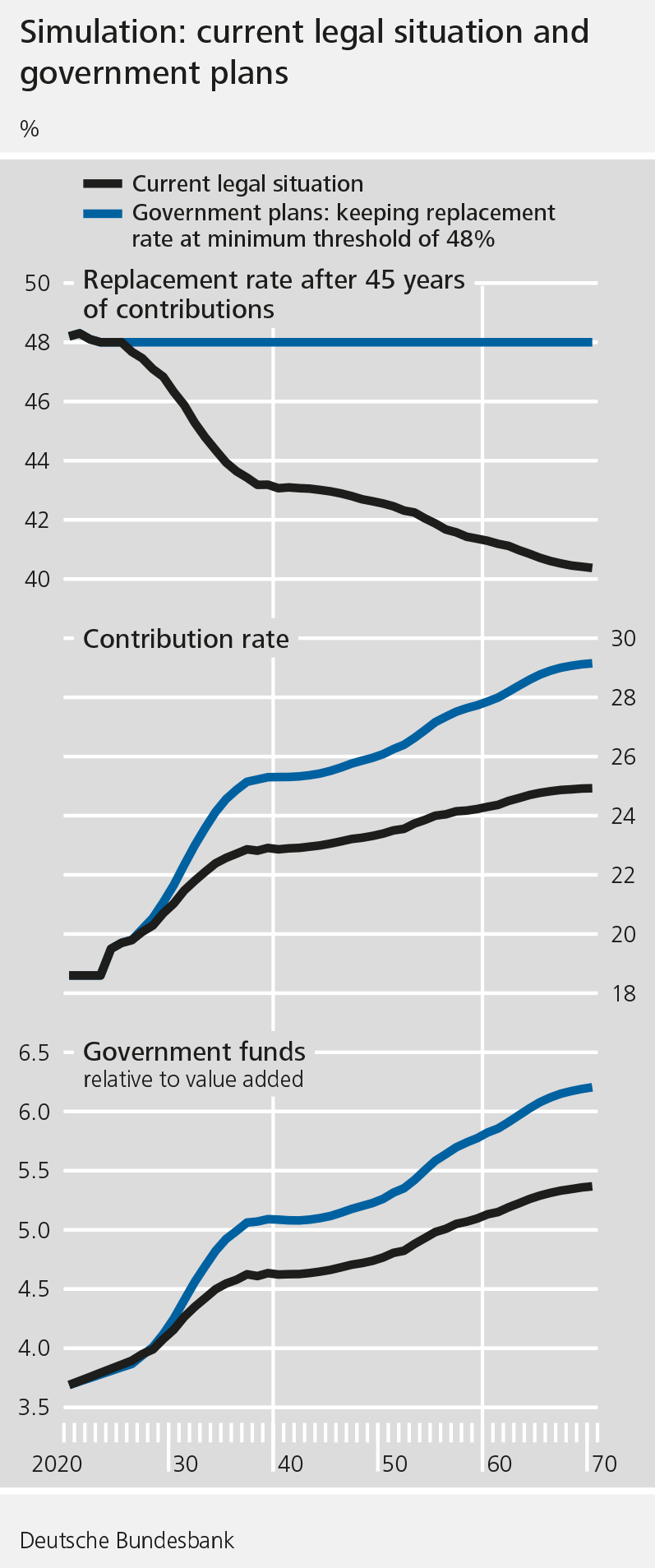

Demographic developments will put the finances of the statutory pension insurance scheme under pressure in future. For one thing, an increasing number of baby boomers will have reached retirement age by the mid-2030s; for another, life expectancy is rising. Up to and including 2025, the contribution rate and replacement rate will still be subject to thresholds: the contribution rate (which is currently 18.6%) may not exceed 20%, while the replacement rate may not fall below 48%. As the latter already stands at 48%, pensions will initially rise at roughly the same pace as wages until 2025.

However, it will probably not be possible to free up these additional funds without cutting expenditure elsewhere or increasing taxes,

” the experts write.

| Variables relating to pensions |

Replacement rate (simplified): Ratio of the standard pension to average earnings after deduction of applicable social security contributions, before tax (standard pension: after 45 years of contributions at the average wage, retirement at statutory retirement age). Statutory retirement age: Age limit for receiving the standard old-age pension with no deductions. This rises gradually for individuals born in and after 1947. The statutory retirement age for individuals born in and after 1964 is 67 (from 2031). Contribution rate: Percentage of gross wages and salaries as a contribution to the pension insurance scheme (collected up to the maximum social security contribution threshold). Generally speaking, pension entitlements are based on contributions paid. Government funds: The Federal Government uses tax funds to pay grants for non-insurance-related benefits and contributions for child-raising periods. Government funds are largely linked to the contribution rate and per capita wages. |

Economists simulate alternative options

How else could the pension scheme look after 2025? This is the question the Bundesbank’s experts have explored in the current Monthly Report, basing their calculations on the approaches used in many other European countries.

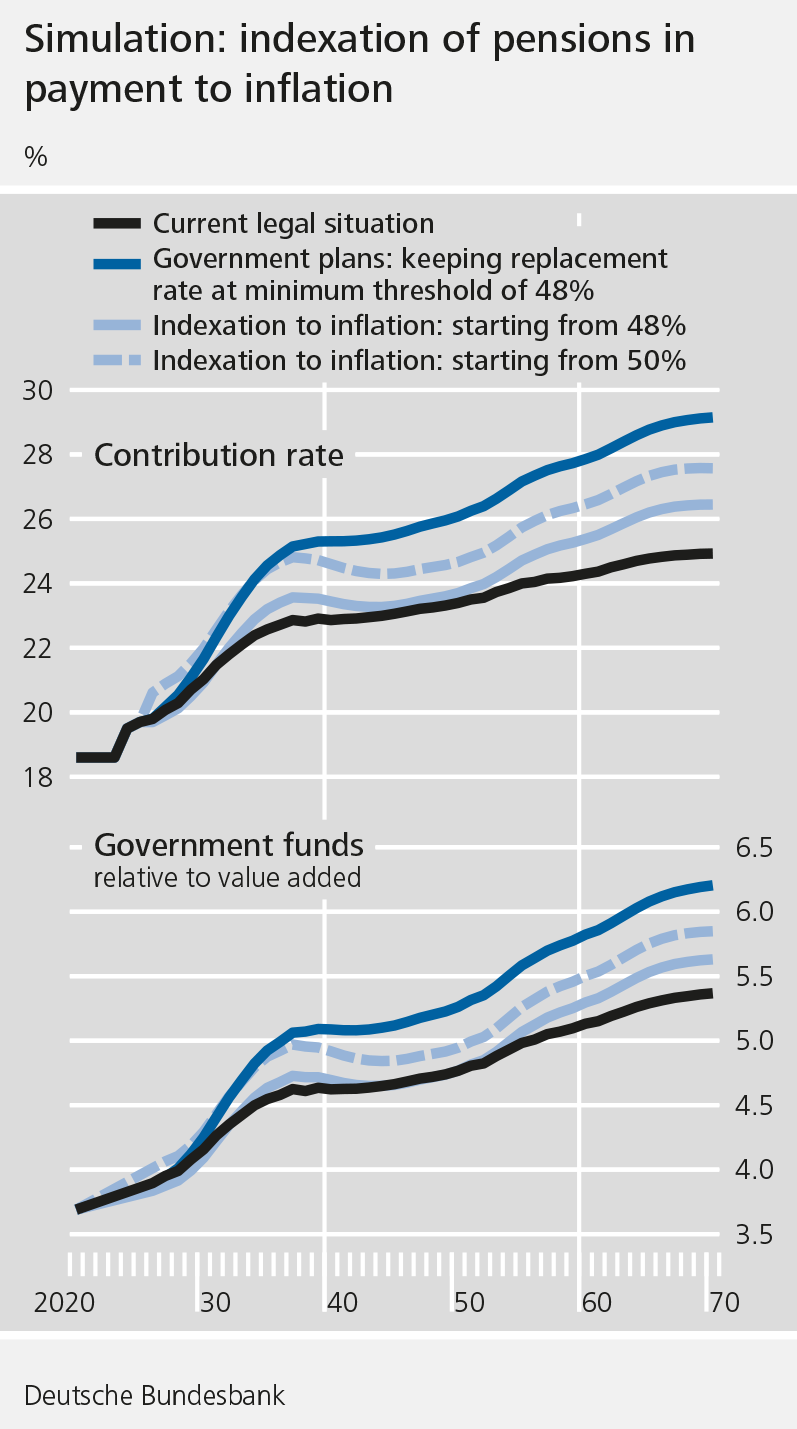

On average, the replacement rate would be just under 44% (instead of 48%) over an average pension-drawing period. If the starting value for the replacement rate were set higher, the gaps relative to the government plans would be smaller. This clearly illustrates the relationship between the replacement rate, the contribution rate and government funds, the experts conclude. However, they also note that if pensions in payment are linked to inflation, they will move in line with real wages. All other things being equal, the contribution rate needs to be higher if trend growth in real wages is slower. The latter would still weaken the revenue base, but would no longer hamper growth in pensions in payment. Likewise, if trend growth in real wages is higher, the contribution rate can be lowered. This would introduce a new uncertainty into the scheme – one which would appear detrimental. The authors stress that the calculations for the simulations did not focus on the current high inflation rates. In fact, the calculations only start from 2026. In their simulations, the experts assume that inflation will reach its target of 2% over the medium term again and that any fluctuations above or below this will offset each other in the long term.

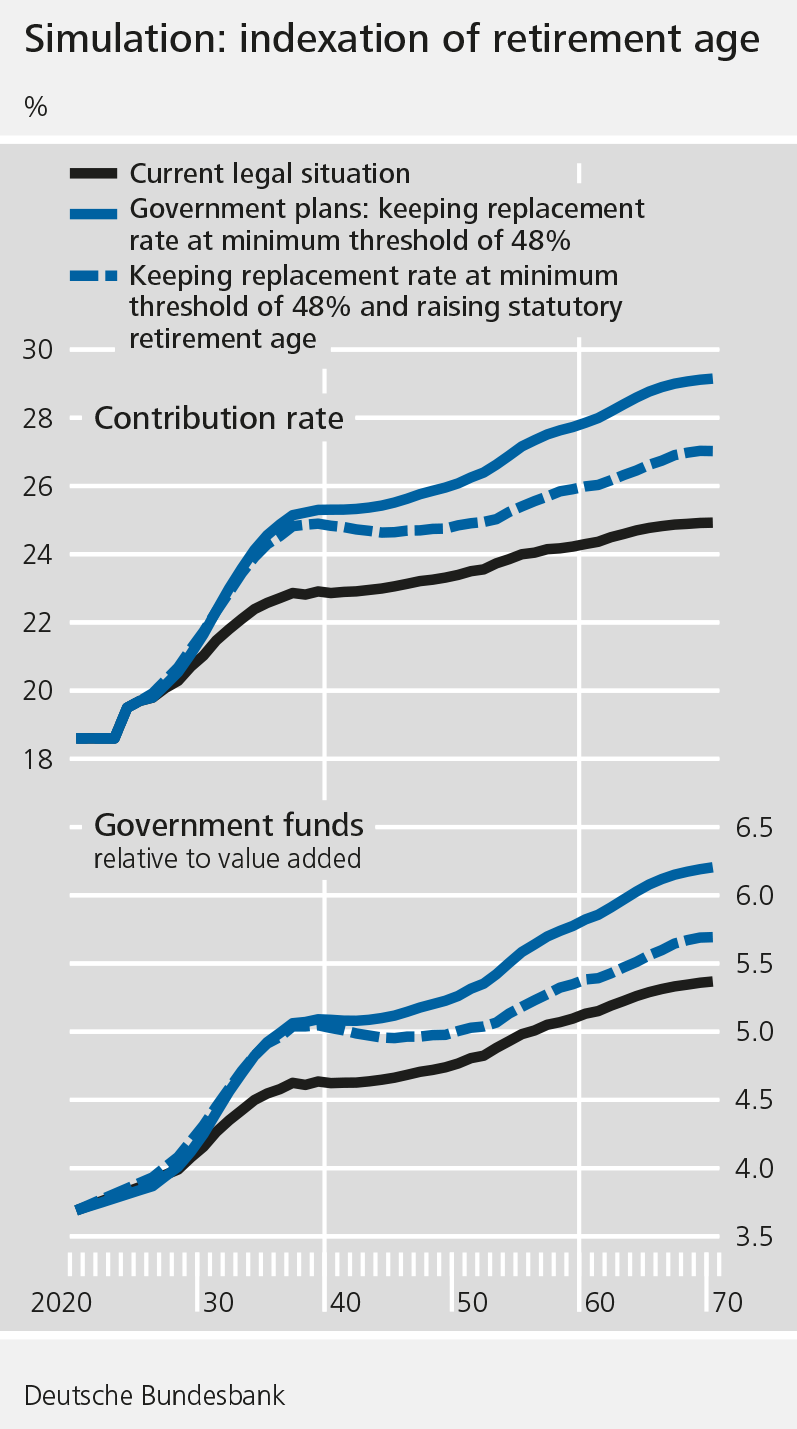

Linking the statutory retirement age to life expectancy

A longer period of employment would see both individual pension benefits and employment rise, thus increasing economic output and tax revenue

,” the economists write. “On the whole, it is clear why a number of national and international advisory bodies recommend that Germany adopt an approach of this kind.

”

The experts stress that because such long-term projections are, by nature, highly uncertain, the simulations are not to be understood as forecasts. “The options for pension approaches presented do not constitute requirements or recommendations,

” the Monthly Report article explains. “The aim is rather to highlight key trends in the individual variables and their relationships.

” The authors note that it is ultimately up to policymakers to decide how demographic burdens should be shared between employed persons, taxpayers and pension recipients.