Institutional investors on the move

Private and institutional investors have changed their investment behaviour since the beginning of the crisis, which has had an impact on the market for mutual funds. Insurance companies and pension fund institutions play an important role.

Change in investment behaviour

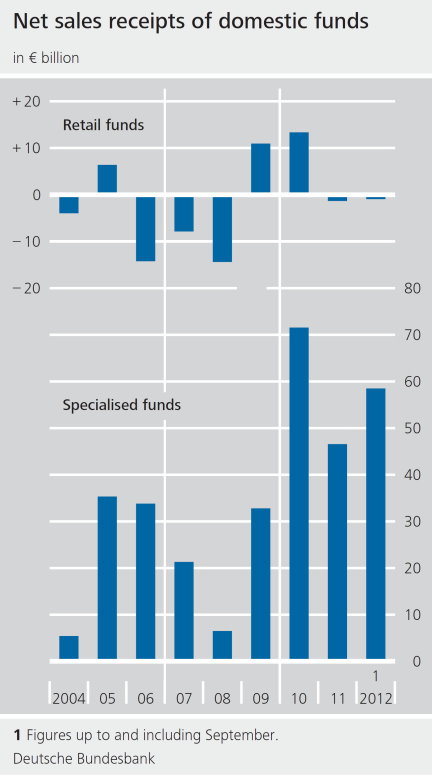

In the crisis year of 2008, institutional investors were considerably more restrained with additional mutual fund investments. They only began to increase their investment activity in the following years. Institutional investors include banks, for example, but also insurance companies, pension fund institutions, pension funds or foundations.

Private investors have also changed their investment behaviour. They began to take a more critical view of investment products, particularly those that were risky, complex and less liquid.[1] As a result they shunned mutual funds, which were exposed to products with these features, and preferred to invest in other products.

Overall the financial crisis is likely to have intensified private investors’ reluctance to invest in retail funds – not least because fund assets, unlike bank deposits, were not guaranteed by the government at the height of the turbulence on the financial markets. Retail funds are mutual funds which are open to every investor – also private individuals. Nonetheless, private investors are still investing substantial amounts in mutual funds indirectly via institutional investors.

Reasons for the subdued investment in retail funds may be, amongst others, a more critical approach towards fund managers and a greater awareness of the contract and administrative costs for private investments. Some investors possibly doubt whether these are reasonable in relation to the expected return.

The market for mutual funds

What do these developments mean for the mutual fund market? Since 2007, retail funds have achieved hardly any positive inflow, that is the difference between inflows of capital from the sale and the redemption of fund units within a certain time period.

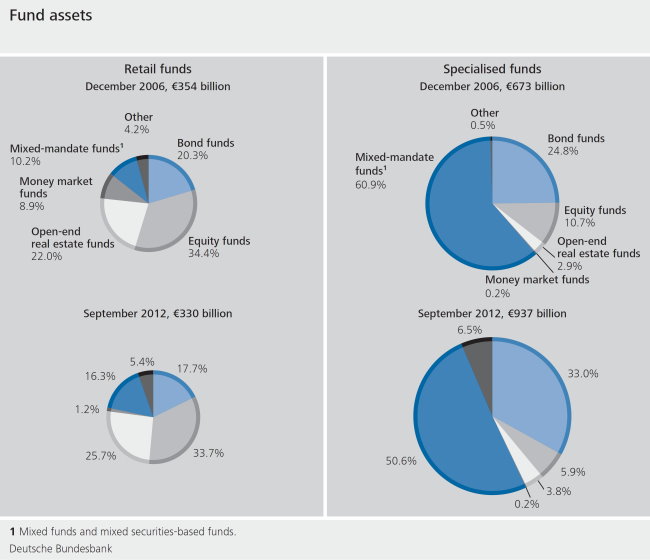

Share-based funds play the most important role amongst the retail funds, which is why the total inflow of funds is strongly dependent on the investments in them. Bond and money market funds also recorded net outflows of capital overall during the financial crisis. Although demand for retail funds stabilised in 2009 and 2010, the sovereign debt crisis in subsequent years led to a renewed dampening effect.[2]

Insurance companies and pension funds

Insurance companies and pension fund institutions are the most important investors in specialised funds. Since 2007, insurance companies have purchased specialised fund units worth €109 billion or more than 50% of the net units issued. Their large-scale investments therefore made a considerable contribution to the stabilisation of the market for specialised funds during the crisis. In light of demographic trends and a greater need for households to invest in private retirement schemes, pension fund institutions have also played a predominant role in the positive inflow of funds. They include inter alia company pension organisations such as Pensionskassen and pension funds as well as occupational pension schemes. Alongside the insurance companies, they have significantly increased their exposure to specialised funds. Since the beginning of 2007, they have accounted for almost a third of the net sales receipts of specialised funds overall. By contrast, credit institutions reduced their exposure to mutual fund units indefinitely during the financial crisis.

Footnotes:

- An investment product is considered all the more liquid depending on how simply and quickly it can be converted into cash – investment on accounts from which money can be withdrawn at any time are considered to be very liquid, for example / an illiquid form of investment is real estate, for example, as it can generally no longer be exchanged into money.

- By contrast, open-end real estate funds and mixed funds, which can shift their assets between the equity and bond markets, experienced net inflows.