Cash remains the most favoured means of payment

As in the past, German consumers prefer to pay for most of their purchases using cash. This is revealed by the Bundesbank's recent 2017 survey on "Payment behaviour in Germany". Upon presenting the survey in Frankfurt, Executive Board member Carl-Ludwig Thiele reported that "Cash remains the most favoured means of payment in Germany", before adding that cashless forms of payment were steadily gaining ground.

The Bundesbank has conducted a household survey on "Payment behaviour in Germany" every three years since 2008. The aim is to examine the way in which households use cash and cashless payment instruments when making their purchases.

According to the survey, German consumers carry around an average amount of €107 in their wallets, including about €6 in loose change. The amount of cash they hold on their person has therefore barely changed since the survey was introduced in 2008. Back then, respondents were found to keep an average amount of €118 at hand, including €7 in coins.

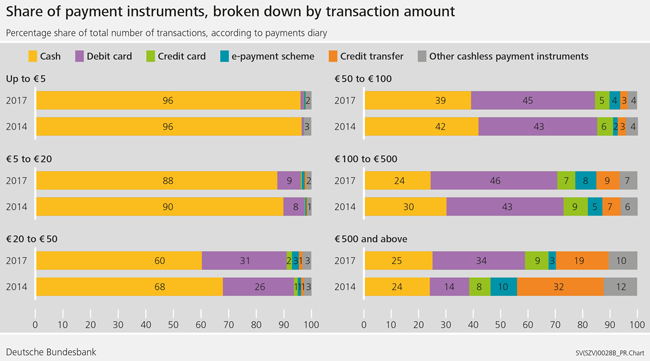

Small amounts almost always settled in cash

In 2017, consumers settled around three-quarters of payments (74%) using banknotes and coins. This is 5 percentage points down on the 2014 figure. The survey found that most purchases costing up to €50 continued to be settled using cash, with cash being favoured to pay small amounts up to €5 in 96% of cases. By contrast, about one in five purchases (19%) were paid for using cards such as girocard.

The survey reveals that, in terms of volume, the share of cash payments has fallen below the 50% mark for the first time since this research was initiated. Compared with the previous 2014 survey, the proportion of payments settled using cash has declined from more than 53% to less than 48%, whereas the use of debit cards, such as girocard, has increased. Compared with its 2015 level, the share of debit card payment has risen by just under 6 percentage points, reaching 35% in 2017. Credit cards were likewise used more frequently than before, mainly for larger amounts averaging €81. Even so, credit card payments still accounted for less than 5% of the total volume.

New payment methods on the rise

According to the survey, and despite their limited use overall, there was an upsurge in contactless card payments which, as a share of the whole, went up for the first time to over 1%. If use is to become more widespread, Mr Thiele believes that all credit institutions will have to issue contactless girocards as standard and the level of acceptance among retailers will have to be improved.

Internet payment systems like PayPal have now become an established part of the online shopping setup. The survey found that, in 2017, these platforms expanded their share of the total volume of payments to almost 4%. Measured in terms of the number of transactions, the share of internet payment systems stood at 2%, with 44% of those surveyed stating that they made use of these systems, albeit often due to a lack of cost-free alternatives.

Majority against the abolition of cash

The vast majority of respondents (88%) voiced an unchanged preference for cash payment, both now and in the future, strongly rejecting the idea of abolishing cash or limiting its use. In this context, 96% fear that, in the absence of cash, certain groups in society, for instance the elderly, would have difficulty effecting payments. An overwhelming majority also regarded cash as an important factor in controlling personal spending and preserving anonymity. According to the survey, four out of five respondents believed that getting rid of cash would greatly inhibit them.

All four of the surveys on payment behaviour conducted thus far show that overall satisfaction with the classic payment methods is high. Nonetheless, the most recent survey reveals high growth rates for state-of-the-art payment systems such as contactless card payment. Young consumers, in particular, are looking for alternatives to classic payment instruments. Overall, 15% of respondents can imagine holding their current account with, for instance, an internet provider rather than a bank or direct bank. Among the 18-to-24 age group, around one in four of those surveyed said they would like to be able to send money to friends and acquaintances using their mobile phones in a simple, easy-to-use manner.