How the German natural gas market responds to supply and demand shocks Research Brief | 71st edition – November 2024

Russia’s invasion of Ukraine triggered an energy crisis in 2022 that posed major challenges to the German economy and sparked broad debate on the economic ramifications of the marked rise in natural gas prices. In a new study, we examine the causes and consequences of this crisis and show how supply shocks and a surge in demand for natural gas storage impacted on natural gas prices and industrial production in Germany.

Natural gas prices in the European Union began to rise sharply in the summer of 2021, ending a two-decade period of low and stable prices. At the height of the energy crisis in 2022, the price of one-month natural gas futures in the European market was twelve times higher than the average for 2019. This presented the German economy with major challenges. While economists have spent decades studying the causes and macroeconomic consequences of oil price fluctuations (for example, Kilian, 2009), the causes and macroeconomic consequences of gas price fluctuations have received far less attention. This is partly because, in the past, natural gas prices were less volatile. However, Germany appears to be particularly vulnerable to gas price fluctuations owing to structural conditions, such as its large industrial sector and its strong dependence on Russian natural gas.

In a new study (Güntner, Reif and Wolters, 2024), we examine the economic drivers behind the turmoil in the German natural gas market. We differentiate between supply-side and demand-side factors and distinguish these by drawing on well-documented evidence of historical events in the natural gas market, amongst other things. Such historical events include, for example, the interruption of Russian gas imports in January 2009 due to a dispute between Ukraine and Russia and the stoppage of natural gas flows through Nord Stream 1 in the summer of 2022.

Dislocations in the gas market lead to strong price effects and small volume effects

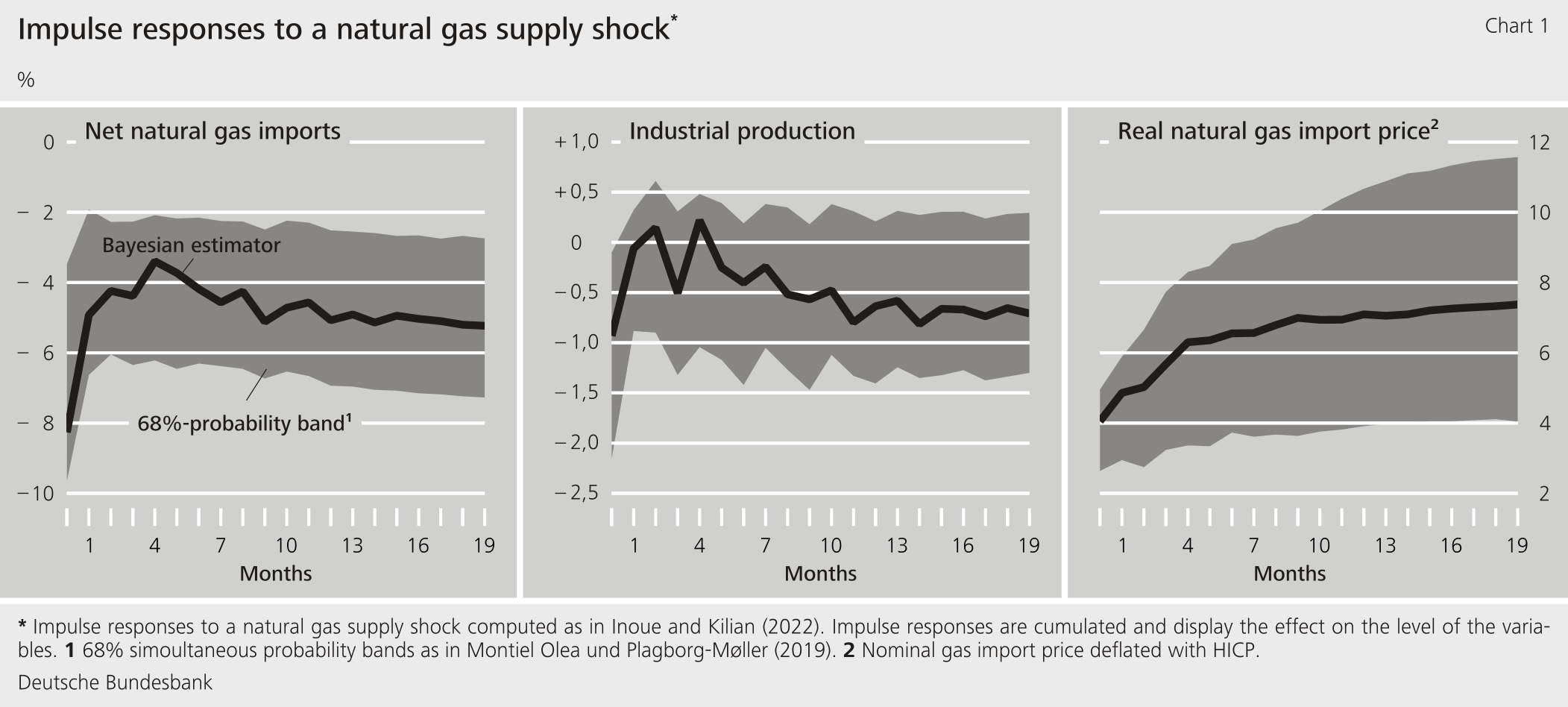

In order to determine the drivers and their economic consequences, we estimate a structural vector autoregressive model for the German natural gas market. Our estimation shows that supply and demand shocks in the gas market lead to significant and persistent price effects for natural gas. By contrast, industrial output responds significantly less strongly to these shocks (Chart 1). Overall, we find that German industry has been fairly adaptable to energy supply disruptions. In particular, only a small part of the fluctuations in industrial production can be attributed to unexpected developments in the supply of gas.

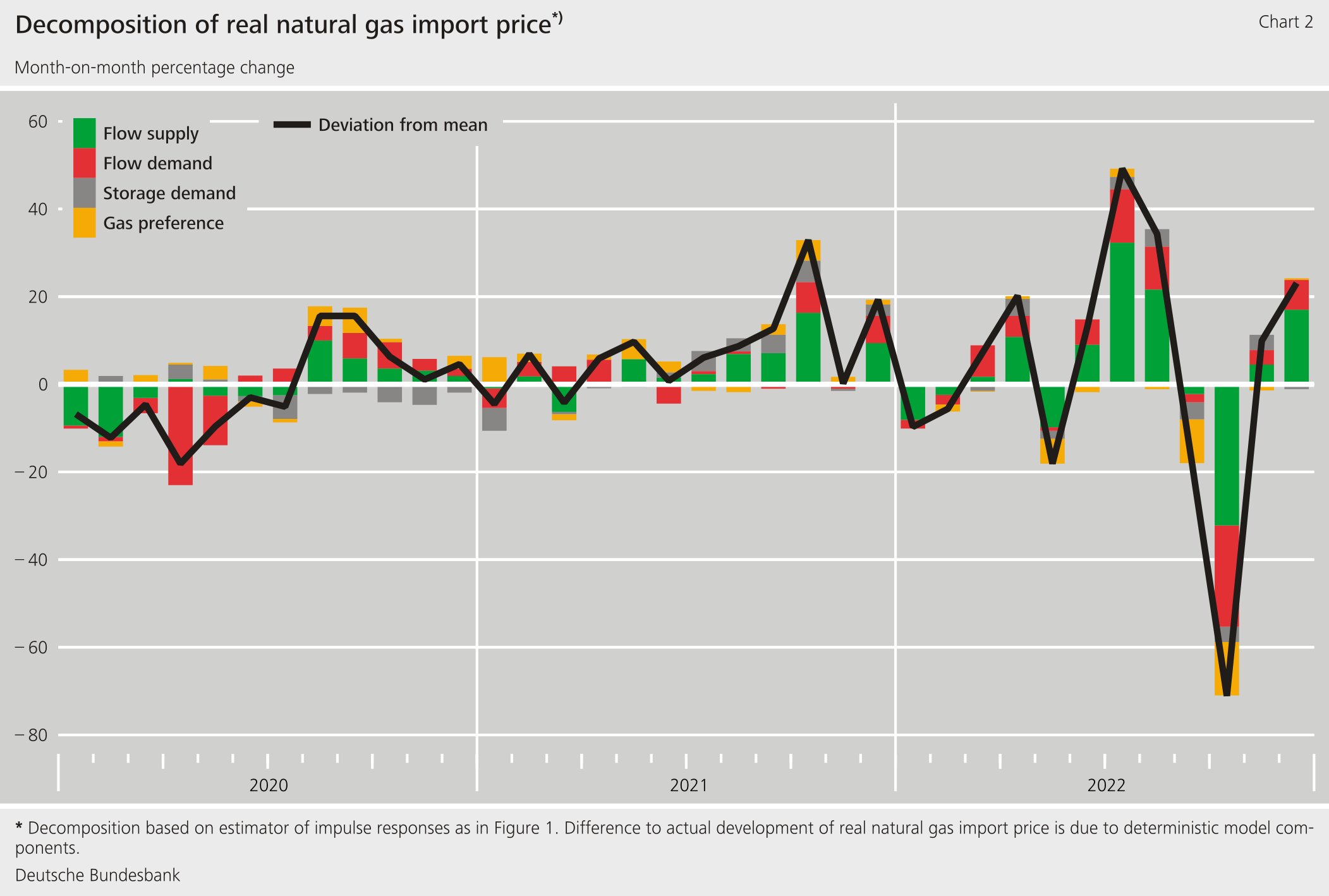

In 2022, the strong fluctuations in the price for natural gas in Germany were mainly due to gas supply shocks (Chart 2). Without the impact of unfavourable supply shocks, the real gas price would have been just over 30 % lower in July 2022. In October 2022, when unexpectedly high gas imports from other countries had largely compensated for halted imports from Russia, the price of gas would have been around 25 % higher without the impact of these favourable supply shocks. However, fluctuations in natural gas demand also contributed to the price developments here. The unexpectedly strong demand in the summer of 2022 is likely to reflect catch-up effects in the aftermath of the pandemic and fiscal support measures (see Hinterlang et al., 2024). The price-dampening demand shocks in the following autumn are related to the gas-saving measures taken by German industry. The contribution to the rise in natural gas prices attributable to the politically driven, rapid filling of German natural gas storage facilities prior to the start of the winter of 2022‑23 is also evident.

The interruption of the gas supply in 2022 could have had significant consequences

Our model also allows for the computation of hypothetical scenarios. For example, we analyse how natural gas prices, storage levels, and industrial production would have developed if total natural gas imports had fallen by 49 % in April 2022. This decline could have occurred if the share of the gas supply attributable to Russian imports at that time had been abruptly cut off. According to the model, this reduction in natural gas imports, when viewed in isolation, would have resulted in energy prices being temporarily somewhat higher than they actually already were. Industrial production would have fallen somewhat more sharply in the short term, while gas storage capacity utilisation would have been lower on a sustained basis. Without comparing the influence of key transmission channels and levers – for example, the substitutability of natural gas – our results are in line with the theoretical work of Bachmann et al. (2022). In another scenario, we look at the effects of the unusually mild winter of 2022‑23. This temperature scenario suggests that the unusually mild winter contributed, in particular, to higher gas storage levels and lower price pressures – in a cold winter, natural gas import prices would have been up to a little more than 19 % higher and gas storage capacity utilisation would have been around 15 % lower. A combination of these two scenarios might have posed considerable problems for the German economy. In particular, a gas shortage – i.e. a complete emptying of gas storage facilities – could not be ruled out in this case, according to the model.

Conclusion

Our study contributes to a better understanding of the macroeconomic effects of gas price shocks and thus provides useful economic policy insights. It shows that the German economy is vulnerable to disruptions in energy supply, but also has a remarkable capacity to adapt to such external shocks.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

References

- Bachmann, R., D. Baqaee, C. Bayer, M. Kuhn, A. Löschel, B. Moll, A. Peichl, K. Pittel and M. Schularick (2024). What if? The macroeconomic and distributional effects for Germany of a stop of energy imports from Russia. Economica, Vol. 91(364), pp. 1157‑1200.

- Güntner, J., M. Reif and M. W. Wolters (2024). Sudden Stop: Supply and Demand Shocks in the German Natural Gas Market. Journal of Applied Econometrics, forthcoming.

- Hinterlang, N., M. Jäger, N. Stähler and J. Strobel (2024). On curbing the rise in energy prices: An examination of different mitigation approaches. Deutsche Bundesbank Discussion Paper No 09/2024.

- Inoue, A. and L. Kilian (2022). Joint Bayesian Inference about Impulse Responses in VAR Models. Journal of Econometrics 231(2), pp. 457‑476.

- Kilian, L. (2009). Not All Oil Price Shocks Are Alike: Disentangling Demand And Supply Shocks in the Crude Oil Market. American Economic Review 99(3), pp. 1053‑69.

- Montiel Olea, J. L. and M. Plagborg-Møller (2019). Simultaneous Confidence Bands: Theory, Implementation, and an Application to SVARs. Journal of Applied Econometrics 34(1), pp. 1‑17.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

194 KB, PDF