Short sellers anticipate governments’ fiscal space during the COVID-19 pandemic Research Brief | 41st edition – August 2021

The outbreak of the COVID-19 pandemic had an unprecedented impact on the global economy, forcing governments to take rapid fiscal action. However, generous government support programmes depend on the government having a good credit rating. How do financial market players take fiscal constraints into account in their investment decisions? A new study looks into this question by analysing developments in short positions in the first few months of the COVID-19 pandemic in Europe.

In a short sale, an investor sells an asset that they have previously borrowed for a specific period, with the intention of buying it back at a later point in time. If the price of that security falls during that period, the investor makes a profit; otherwise, they suffer a loss. Although short selling is a controversial topic in public debate, several studies suggest that short sellers are informed investors (Boehmer, Jones and Zhang, 2008; Wang, Yan and Zheng, 2020). They have an important role to play in the financial market as they contribute to efficient price discovery. Above all, they ensure that negative information is reflected in lower prices (Engelberg, Reed and Ringgenberg, 2012; Ljungqvist and Qian, 2016).

The COVID-19 pandemic is an opportunity to examine how short sellers behave in an unprecedented “black swan” event. For our analysis, we use European data on public short positions reflecting significant short positions above a threshold of 0.5% of a company’s shares outstanding. Disclosure includes the name of the investor, the amount of their short position as well as the name and ISIN of the stock in question. This amount of detail and the daily availability of the data help us to observe how short sellers acted during the outbreak of the pandemic and the subsequent stock market crash. In particular, we analyse how financial market players incorporated individual governments’ fiscal space as an important factor in cushioning the plummeting sales at the affected firms, into their decisions.

In our current working paper (Grepinitr, Jank and Smajlbegovic, 2021) we examine the role played by (a country’s) fiscal space for short sellers during the COVID-19 pandemic. In doing so, we proceed in two stages. First, we measure countries’ respective fiscal space based on their credit rating (Kose, Kurlat, Ohnsorge, and Sugawara, 2017). Second, we categorise companies by how much liquidity they had at the beginning of the pandemic (Fahlenbrach, Rageth, and Stulz, 2020). The hypothesis is that firms with little short-term liquidity cannot absorb the revenue shock and are therefore reliant on generous domestic support programmes. However, if such programmes can be set up only by countries with sufficient fiscal space, we would expect short sales to occur primarily in companies with low liquidity that are headquartered in countries with a low credit rating.

Figures 1 and 2 illustrate the results of our analysis. Figure 1 shows countries with a low rating (lower than “AA”), and Figure 2 shows countries with a high rating (greater than or equal to “AA”). In addition, we differentiate between firms with large and those with small liquidity reserves. Before the crisis, there was no clear difference in short selling activity between these two groups of companies (see Figure 1). During the stock market collapse in February 2020 and also shortly beforehand, we see a clear rise in short positions in companies with low liquidity headquartered in countries with a poor credit rating. Many of these short positions were closed again before the end of the market crash (between February and March 2020). Nonetheless, the number is elevated as compared with short positions in firms with a large share of liquid assets. For these, short positions fell significantly in this period. Only in the second market recovery period (between May and June 2020) did short selling activity in the two groups converge again. In countries with a high credit rating (see Figure 2), we do not observe this change in short sellers’ strategy. This finding suggests that short sellers have incorporated the limited ability of fiscally constrained governments to support firms with liquidity problems into their decisions.

Further analyses in the form of detailed panel regression analyses back up this interpretation of the results. We show that short sellers’ trading behaviour can be explained neither by the severity of the COVID-19 pandemic and the measures taken to contain it nor by the liquidity of the banking system in the respective countries. Controlling for these alternative explanations, short sellers appear to have reacted to the heterogeneity of the affected countries’ fiscal space in combination with firms’ liquidity. Further tests suggest that short sellers have pursued this strategy mainly for firms with a largely local sales market. These firms are particularly reliant on domestic stimulus programmes.

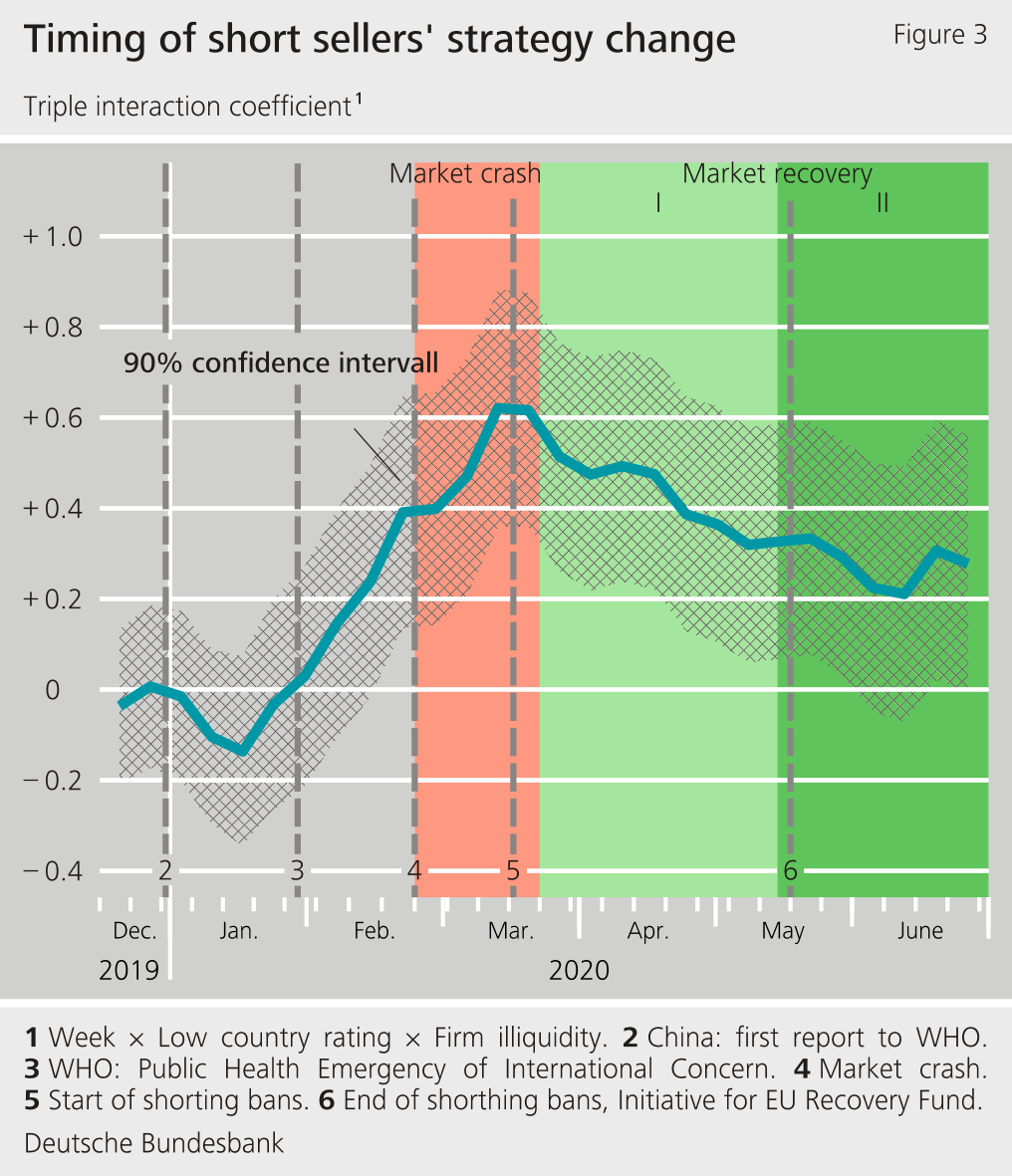

In the next step, we observe short sellers’ exact timing in order to answer the following question: in countries with a low credit rating, how much does the share of short positions change in illiquid as compared to liquid firms? The reference group is composed of short positions in countries with a high credit rating, and the reference period is from 1 July 2019 to 15 December 2020.

This anticipation is also evident in the profitability of the short sales: during the market crash period of the pandemic, positions with a focus on illiquid firms headquartered in countries with a weak credit rating generated a risk-adjusted return of around 15 percent. Relative to the movements of the overall market, we see no significant decline of this return in the three months following the market crash. In line with the academic literature (e.g. Boehmer, Jones and Zhang, 2008; Wang, Yan and Zheng, 2020), this evidence suggests that short sellers have not driven prices below their new fundamental value, but rather that they are actively involved in the price discovery process as informed financial market participants. In this context, the findings of our work show a new dimension to short sellers’ abilities: even in an unprecedented global pandemic, short sellers appear to process new public information quickly and to align their positions correspondingly even before the market crash.

Conclusion

Our study suggests that during the COVID-19 crisis short sellers anticipated the importance of fiscal space, which is crucial for allowing governments to provide sufficient stimulus for badly affected firms, and that short sellers reacted to this information early on. The fact that this short selling strategy produced clear portfolio gains shows that short sellers process information exceptionally quickly even in an unprecedented crisis.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Boehmer, E., Jones, C. M., Wu, J., & Zhang, X. (2020). What do short sellers know? Review of Finance 24(6), 1203-1235.

- Engelberg, J. E., Reed, A. V., & Ringgenberg, M. C. (2012). How are shorts informed? Short sellers, news, and information processing. Journal of Financial Economics 105(2), 260-278.

- Fahlenbrach, R., Rageth, K., & Stulz, R. M. (2020). How valuable is financial flexibility when revenue stops? Evidence from the Covid-19 crisis. NBER Working Paper 27106.

- Grepinitr, S., Jank, S., & Smajlbegovic, E. (2021). On the Importance of Fiscal Space: Evidence from Short Sellers during the COVID-19 Pandemic. Deutsche Bundesbank Discussion Paper 29/2021.

- Kose, M. A., Kurlat, S., Ohnsorge, F., & Sugawara, N. (2017). A cross-country database of fiscal space. Policy Research Working Paper 8157, World Bank.

- Ljungqvist, A., & Qian, W. (2016). How constraining are limits to arbitrage? The Review of Financial Studies 29(8), 1975-2028.

- Wang, X., Yan, X. S., & Zheng, L. (2020). Shorting flows, public disclosure, and market efficiency. Journal of Financial Economics 135(1), 191-212.

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

979 KB, PDF