Banks as investors in government bonds during the crisis – central bank-funded search for yield or de-risking? Research Brief | 36th edition – November 2020

Did German banks take on a particularly high level of risk during the financial crisis by investing in risky government bonds? A new study examines the behaviour of German banks between 2008 and 2014 and reveals that German banks – especially those that received government support and were comparatively undercapitalised – de-risked. This finding contrasts with the results of similar studies for banks in the euro area periphery countries.

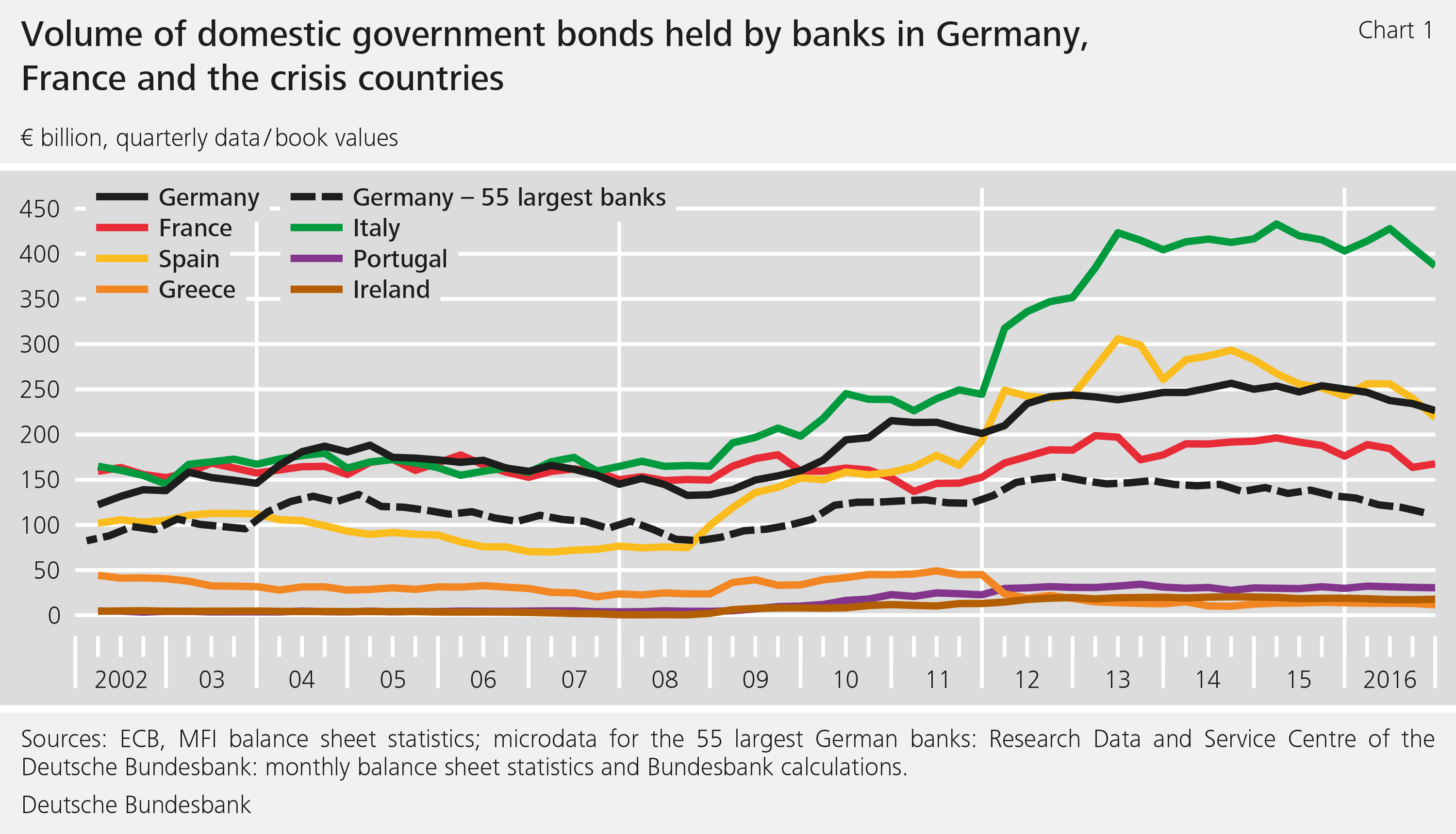

Government bonds have traditionally played an important role in European banks’ portfolios. They were and remain so popular because they are generally considered immune to default. In addition, they receive preferential regulatory treatment compared to bonds issued by private issuers in the sense that it is not necessary to hold capital against them provided they are issued within the euro area. Government bonds accounted for up to 10% of total assets in national banking systems at the end of 2010, when the European sovereign debt crisis had already reached a critical stage. During the debt crisis, banks in the euro area periphery countries continued to increase their holdings of domestic government bonds, which – due in part to the risk they carried – were higher-yielding. Particularly hard hit by the crisis were Italy, Spain, Portugal, Greece and Ireland, which are referred to in this research brief as “crisis countries” (see Chart 1).

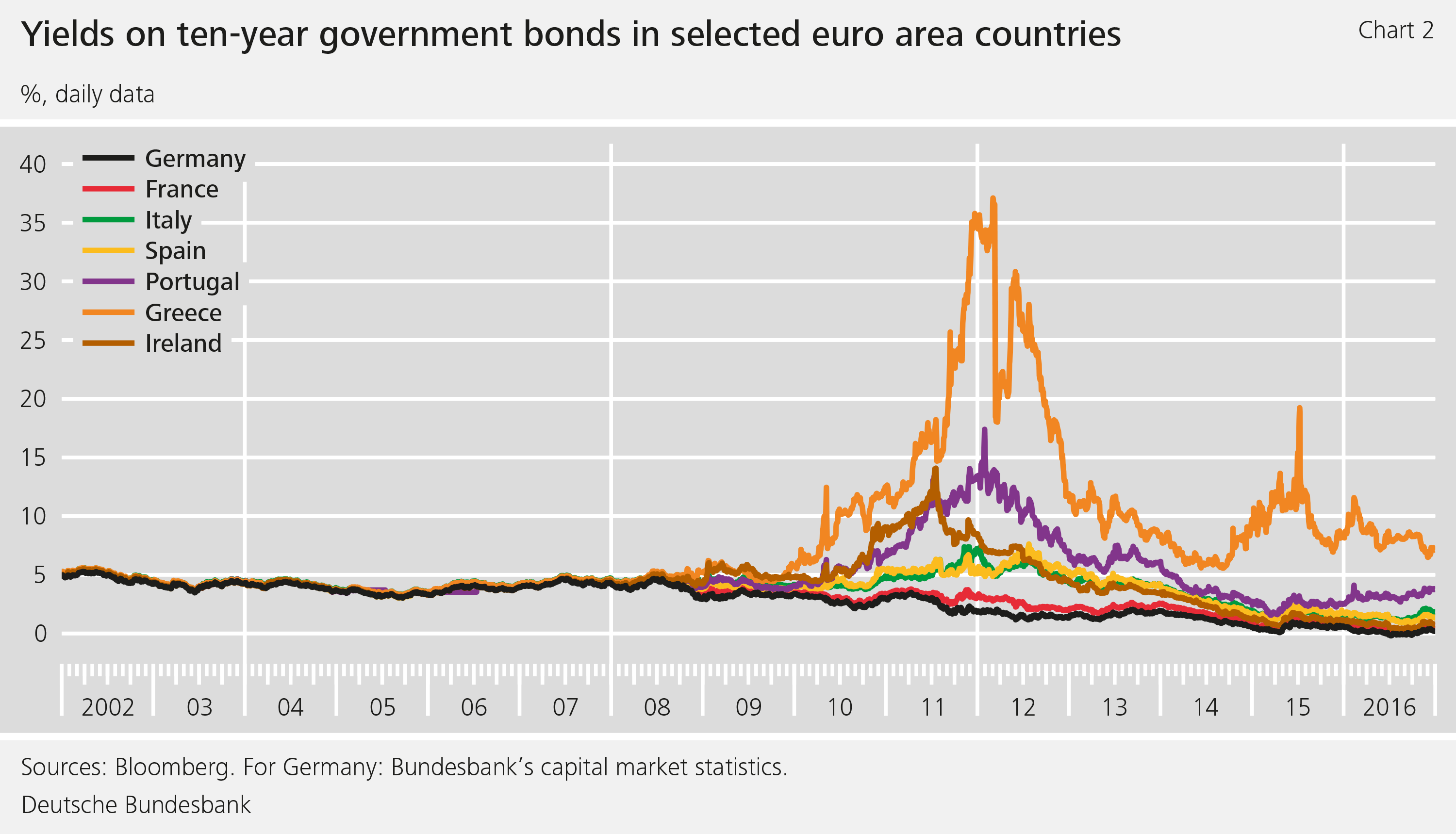

This increase is explained in the literature by various behavioural patterns. First, publicly owned banks and banks in receipt of government support during the crisis could have purchased domestic government bonds in response to government pressure (“moral suasion”). What this means is that governments could have leaned on these banks to purchase their own sovereign debt – in an effort to limit the cost of their debt as capital market yields rise. As a result, in the aftermath of the sovereign debt crisis (starting in 2010), there was a spread in yields on euro area government bonds, which was due mainly to the sharp rise in yields on government bonds issued by the crisis countries (see Chart 2).

Second, undercapitalised banks increased their holdings of these high-yielding bonds. Such behaviour may have been driven by the search for yield in connection with speculation about a government bail-out if they were in crisis (“gambling for resurrection” or “moral hazard”) (see Acharya et al. (2015), Becker and Ivashina (2018), and also Ongena et al. (2019)). In addition, it can be worth banks’ while to invest in risky government bonds even without the prospect of a government bailout. This option is ultimately weighed up based on their limited liability. The search for yield is also appealing for those banks whose survival is intertwined with their sovereigns’ solvency, e.g. because the survival of their borrowers depends directly or indirectly on the government (see Anand and Mankart (2020).

German banks acted differently to banks in the crisis countries

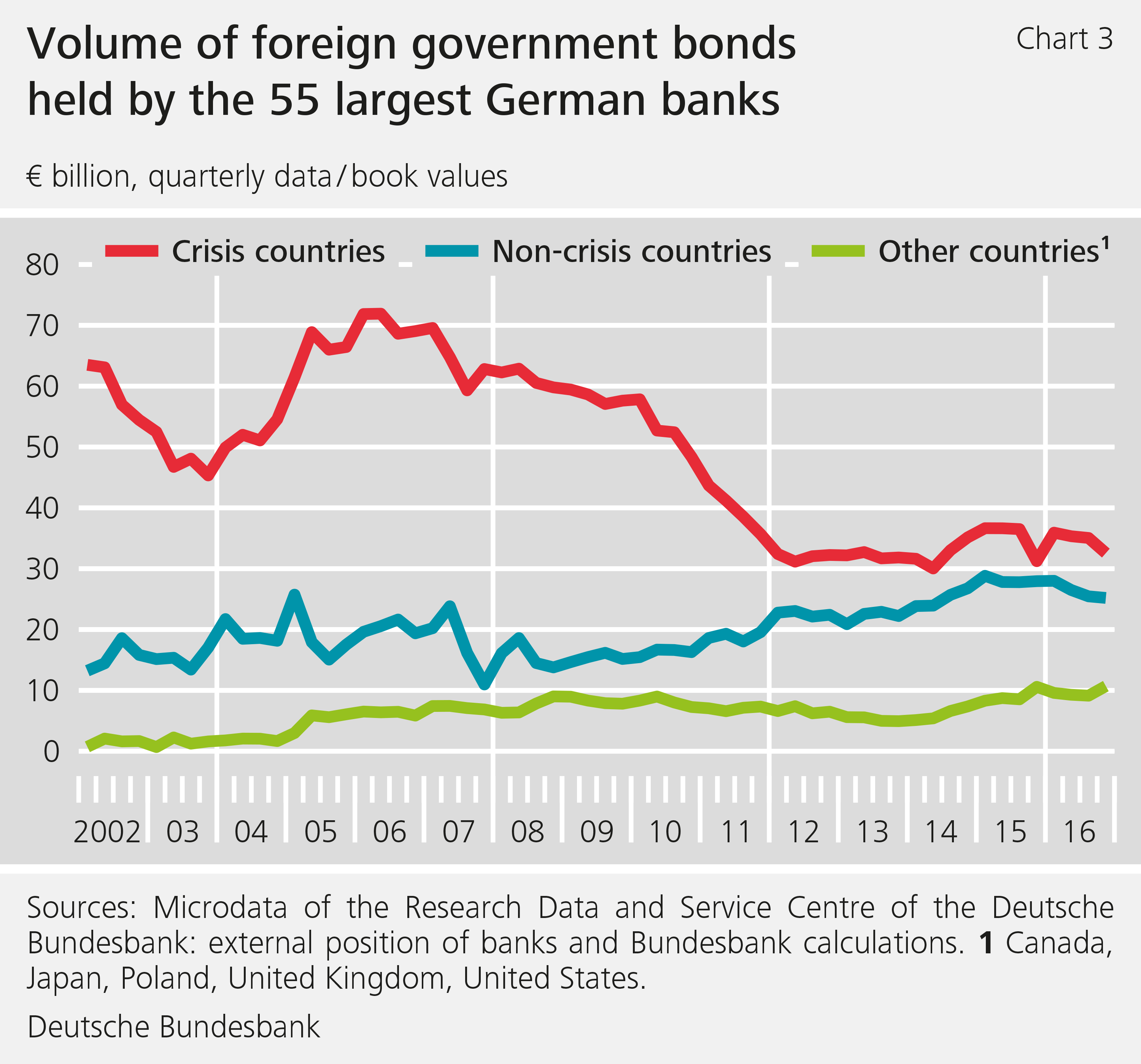

Many German banks reduced their exposure to government bonds issued by crisis countries from 2008 onwards and trimmed their holdings even further as of the second quarter of 2010. They increasingly shifted their investment to bonds issued by other countries both inside and outside the euro area (see Chart 3). The present study (see Frey and Weth (2019)) therefore examines, with a focus on German banks, whether search-for-yield strategies played a role in investment in risky government bonds even in the absence of moral suasion. In this context, this research brief will look at the extent to which banks’ investment decisions depended on government support, central bank funding and their capitalisation. Previous studies found that better-capitalised German securities trading banks invested more in risky securities (see Abbassi et al. (2015)). With regards to moral suasion, there is evidence that certain regional bank types in Germany hold more of their regional government’s public debt than other banks (see Ohls (2017) and Koetter and Popov (2020)). However, there is no such evidence for bonds issued by the Federal Government (Bunds).

Search for yield initially confined to strong banks

Using the bank-specific microdata collected by the Bundesbank, we use panel estimates with fixed bank-specific and country-specific effects to examine how German banks’ exposure to risky and safe government bonds changes as bond prices change. Specifically, the question is whether – and when – banks chose procyclical or countercyclical trading strategies. A countercyclical strategy refers to the purchase (sale) of securities when their prices fall (rise); by the same token, a procyclical strategy entails purchases (sales) as prices rise (fall). Here we follow the approach of Altavilla et al. (2017). Their main finding is that bailed-out banks in the crisis countries as well as weakly capitalised banks in these countries pursued a countercyclical investment strategy and invested heavily in risky domestic government bonds during the crisis.

Of the 55 largest German banks, the institutions that did not have to resort to government assistance during the crisis or had high capital adequacy pursued a countercyclical trading strategy during the first estimation period from the beginning of 2008 to mid-2011. This result contrasts with the findings of Altavilla et al. (2017). Another difference from banks in the crisis countries is that, for German banks, there is no link between increased recourse to central bank funding and exposure to risky securities from the periphery. Instead, the factors that encouraged such exposures included pronounced short-term refinancing in the interbank and capital markets (wholesale funding) and a high level of foreign security trading activity, both in proprietary trading and on behalf of clients.

In the subsequent estimation period from autumn 2011 to the end of 2014, German banks, irrespective of their level of capitalisation, increasingly pursued a procyclical strategy characterised by the sale of risky government bonds. We interpret this withdrawal as “de-risking motivated by regulation and reputation”. By contrast, German banks expanded their exposure to high-quality foreign government bonds over the same period. Procyclical purchasing activity is found mainly in bonds from Austria, Belgium, Finland, France, Slovakia and the Netherlands, but also from the United States and Canada.

These findings regarding German credit institutions are in contrast to the existing empirical evidence for banks in the euro area crisis countries indicating that poorly capitalised banks and public banks steadily stepped up their holdings of domestic government bonds. According to our study, German credit institutions show a different pattern: highly capitalised institutions emerge in particular as purchasers of government bonds from the crisis countries in the period from 2008 to mid-2011. After mid-2011, however, they reduced their holdings of sovereign bonds issued by crisis countries irrespective of their level of capitalisation. This finding is corroborated by Ben-David et al. (2019), who discovered that, in the case of US banks, poorly capitalised institutions reduced their balance sheet positions and did not seek yields on the assumption that the government would bail them out in an emergency.

This raises the question of whether weakly capitalised institutions in the crisis countries are purchasing domestic securities solely for yield-seeking purposes, as shown by Altavilla et al. (2017) and Acharya et al. (2015) or whether they could have been under subliminal pressure from the home country (Drechsler et al. (2016) and Ongena et al. (2019)). Thus, the purchasing behaviour of poorly capitalised banks could be indicative of an indirect form of moral suasion if the government does not yet have direct access to weakened institutions, although these institutions can certainly expect a future bail-out by the government.

Finally, a look at the period prior to the start of the financial crisis – in this case from 2002 to 2007 – shows that German banks that subsequently received government support had increasingly taken bonds from the periphery countries into their own holdings between 2005 and 2007. By contrast, in the period from 2014 to 2016, during which the Eurosystem’s public sector purchase programme (PSPP) also took effect in the market from March 2015, we are unable to identify a clear investment pattern for German institutions with regard to periphery bonds.

Conclusion

We note that German banks reduced their holdings of government bonds, especially from the periphery countries, in the period from mid-2011 to the end of 2014 in particular – a period which encompasses the peak of the sovereign debt crisis. This result is independent of whether an institution received government support or made greater use of central bank funding, and capital adequacy did not play a role, either. This result contrasts with the empirical evidence for banks in crisis countries, which increasingly bought domestic – and thus risky – government bonds during this period. This discrepancy in the evidence between German institutions and those from crisis countries raises the question as to whether the behaviour of the latter group can be explained by a pure economic search for yield. The hypothesis of a – possibly indirect – influence by governments, the role of the Eurosystem’s new long-term financing facilities, and the role of the preferential regulatory treatment of government bonds are all avenues for future research.

| Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Abbassi, P., R. Iyer, J.-L. Peydró and F. R. Tous, 2016, Securities trading by banks and credit supply: micro-evidence from the crisis, Journal of Financial Economics, Vol. 121, No. 3, pp. 569-594.

- Acharya, V. and S. Steffen, 2015, “The Greatest Carry Trade Ever? Understanding Eurozone Bank Risks,” Journal of Financial Economics, Vol. 115, pp. 215-236.

- Altavilla, C., M. Pagano and S. Simonelli, 2017, Bank Exposures and Sovereign Stress Transmission, Review of Finance, Vol. 21, No 6, pp. 2103-2139.

- Anand, K. and J. Mankart, 2020, Sovereign risk and bank fragility, Deutsche Bundesbank Discussion Paper No 54/2020.

- Becker, B. and V. Ivashina, 2018, Financial Repression in the European Sovereign Debt Crisis, Review of Finance, Vol. 22, No 1, pp. 83-115.

- Ben-David, I., A. Palvia and R. Stulz, 2019, Do Distressed Banks Really Gamble for Resurrection?, NBER Working Paper No 25794.

- Drechsler, I., T. Drechsel, D. Marques-Ibanez, and P. Schnabl, 2016, Who Borrows from the Lender of Last Resort?, Journal of Finance, Vol. 71, No 5, pp. 1933-1974.

- Frey, R. and M. Weth, 2019, Banks’ holdings of risky sovereign bonds in the absence of the nexus – yield seeking with central bank funding or de-risking?, Deutsche Bundesbank Discussion Paper No 19/2019.

- Koetter, M., and A. Popov, 2020, Political Cycles in Bank Lending to the Government, Review of Financial Studies, forthcoming.

- Ohls, J., 2017, Moral suasion in regional government bond markets, Deutsche Bundesbank Discussion Paper No. 33/2017.

- Ongena, S, A. Popov and N. Van Horen, 2019, The invisible hand of the government: Moral suasion during the European sovereign debt crisis, American Economic Journal: Macroeconomics, Vol. 11, No 4, pp. 346-379.

| The authors | |

|

|

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

2 MB, PDF