Tighter bank capital requirements do not reduce lending long term Research Brief | 22nd edition – November 2018

Many countries imposed tighter bank capital requirements following the 2008-09 financial crisis in order to repair the structural flaws in the banking system exposed during the crisis and thereby safeguard financial stability. At the same time, there is debate as to whether tighter capital requirements could come with a longer-term cost for the real economy. A new study for the United States explores the macroeconomic effects of a tightening of bank capital requirements. It finds that tighter requirements reduce lending only temporarily: after an adjustment period, the banking system is better capitalised and less risky, with no permanent costs to the macroeconomy.

Many countries around the world responded to the financial crisis of 2008-09 by initiating new microprudential and macroprudential policy measures, the most prominent of which have been tighter bank capital requirements. These measures are designed to mitigate systemic risk and safeguard the long-term stability of the financial system. The intention is to avoid the onerous costs entailed by financial crises (Reinhart and Rogoff, 2009). At the same time, there is debate as to whether tighter capital requirements could potentially come with longer-term costs for the real economy (see Calomiris, 2015; Admati and Hellwig, 2013). In theory, too, the aggregate effects of tighter capital requirements are not clear-cut (see the literature overview in Begenau, 2018 or Bahaj and Malherbe, 2018). What effects tighter capital requirements have on the real economy, and how long-term these are, largely hinges on how banks adjust their balance sheets. They can (i) constrain lending, (ii) use more equity funding and keep lending at a constant level, or (iii) actually increase lending and opt for a more equity-based funding profile. In our study, we examine how the banking system adapts as well as the potential extent and duration of the economic effects of tightening the capital requirements for banks.

For this study, we develop a narrative index of exogenous tightenings of regulatory capital requirements for US banks between 1979 and 2008. We identify those events that led to a tightening of capital requirements. In all cases, a considerable contingent of US banks raised their capital ratios simultaneously and significantly. The reasons for the regulatory measures given in the literature and the often lengthy process of introducing them would appear to indicate that the measures were designed to remedy fundamental flaws in the banking system and were not meant as short-run stabilisers. To that extent, these are not measures designed to smooth the financial or business cycle. For this reason, we can use these policy measures to identify cause-and-effect relationships regarding the channels of adjustment to tighter capital requirements.

In our analysis, we focus mainly on the points in time at which the new regimes came into effect. We also look at the administrative sequence of the introduction of specific regulatory measures. These analyses show that information on new regulations was already available to banks and other market participants prior to their entry into effect. We also use this information and, in our econometric model, allow market players to already adapt to the new rules even before they become legally binding.

Tightening of capital requirements produces marked, but temporary effects

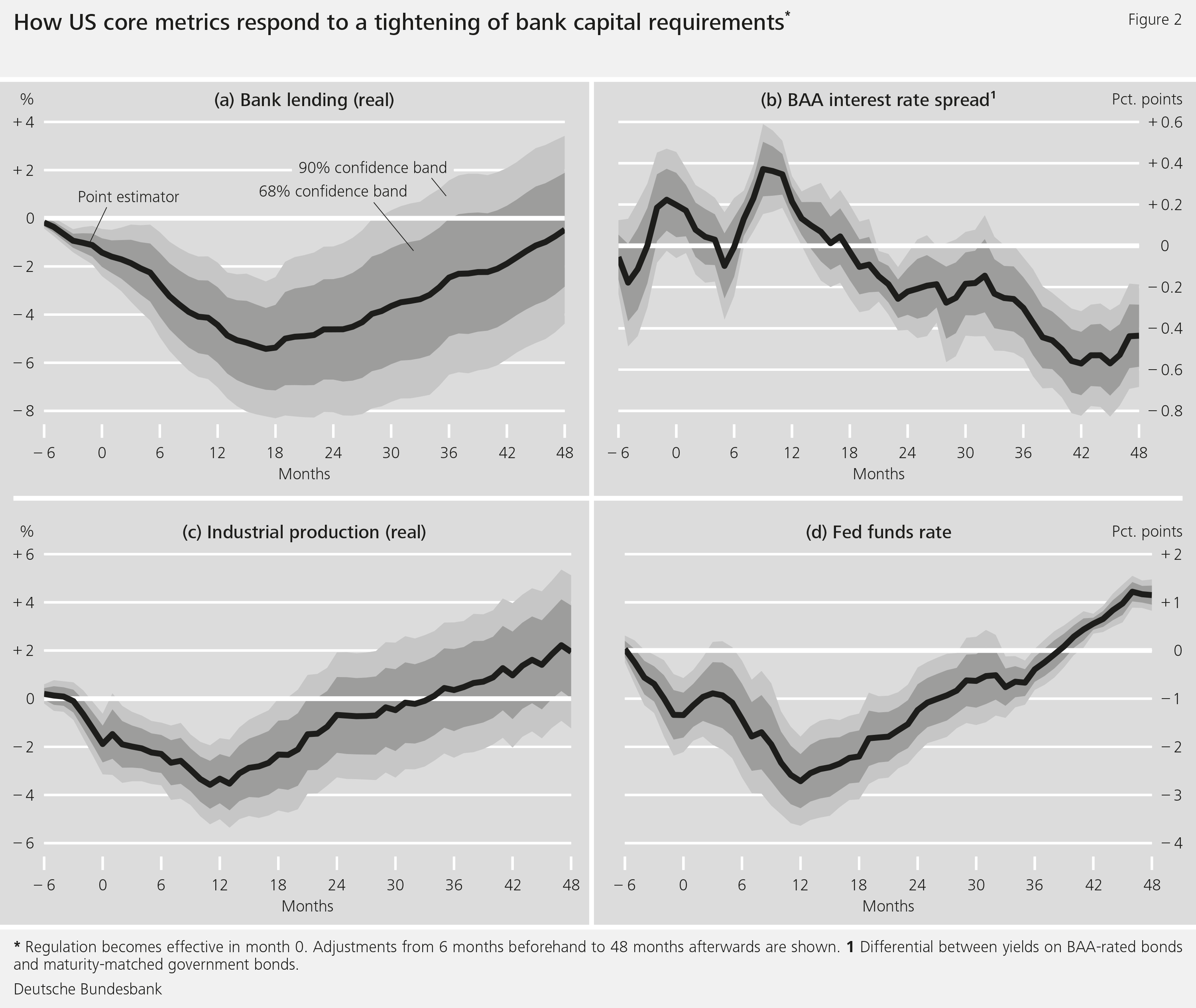

We use local projections in order to study the impact of tighter capital requirements on the US economy. Figure 1 shows the results of the empirical analysis in detail. As intended by regulation, tighter capital requirements lead to a lagged, yet permanent increase in the aggregate, unweighted capital ratio (Figure 1a). The balance sheet adjustments made by banks play a pivotal role for the macroeconomic effects. According to our estimates, banks quickly reduce their assets (Figure 1b) and increase their capital only after around one year (Figure 1c). At the end of the adjustment process, banks have a more equity-based long-term funding profile, with their business volume remaining unchanged.

In the process of adjusting to a more equity-based funding profile, banks temporarily reduce their credit supply (Figure 2). They crimp their lending and the interest rate spread rises at the same time (Figures 2a and 2b). The temporary decline in credit causes industrial production to contract initially; however, about two years after the introduction of the new regulation, it reverts to its previous level (Figure 2c). The effects are non-negligible (being in the magnitude of those found by recent microeconomic studies, such as Aiyar et al., 2014), but are merely temporary. The US central bank subsequently responds to the regulations by reducing its policy rate in order to stimulate economic activity (Figure 2d).

We also find evidence for anticipatory effects: as early as around six months before the new rules become effective, bank assets, industrial production and the monetary policy rate all start to decline.

A decline in risk and loose monetary policy cushion adverse effects

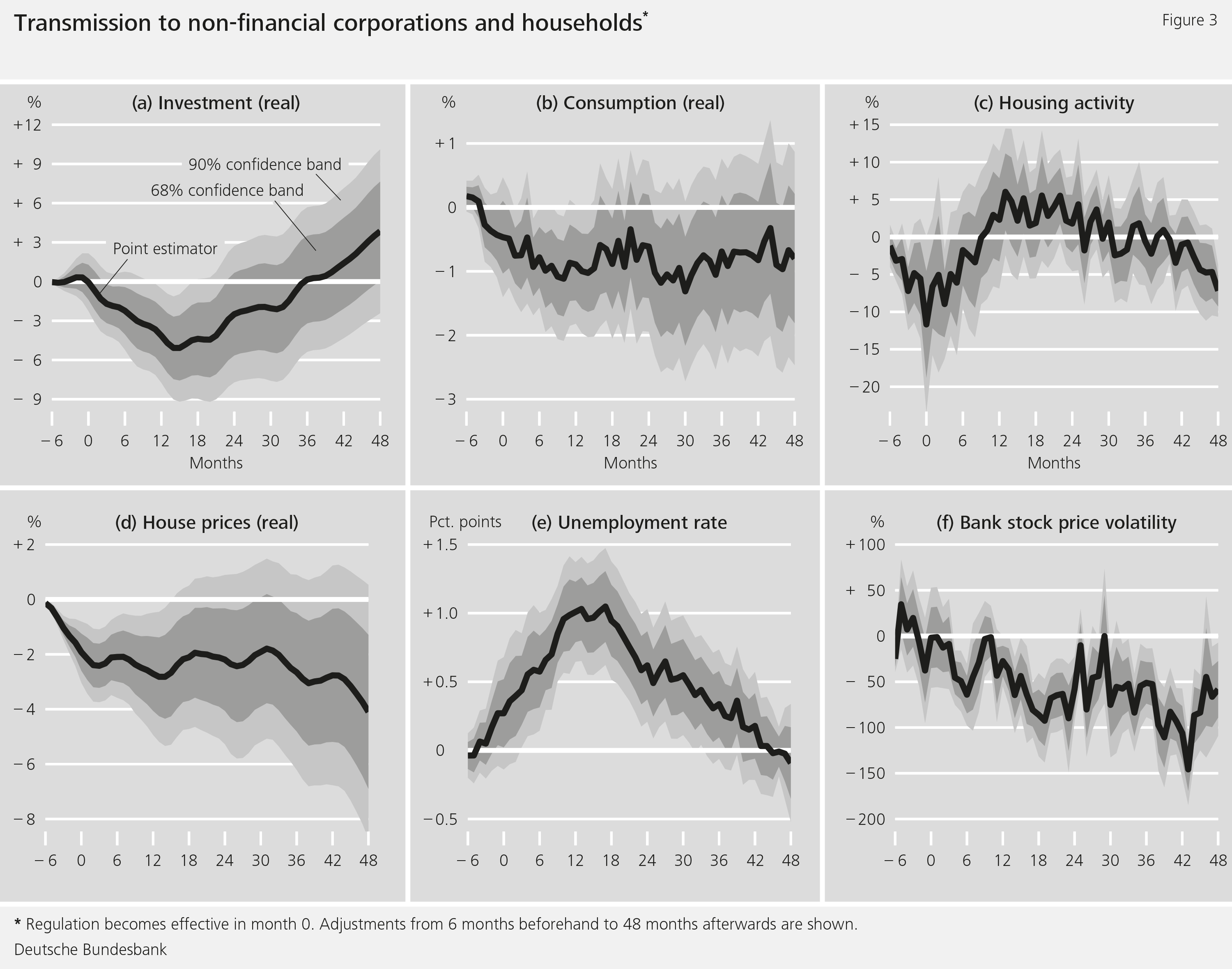

Lastly, we analyse the transmission mechanism, i.e. how the tightening of capital requirements impacts on the macroeconomy – such as property prices. Figure 3 shows that negative loan supply effects trigger a temporary decline in investment, consumption and housing starts (Figures 3a to 3c). The drop in household spending can be explained by falling house prices and a rise in the unemployment rate, which impact adversely on household wealth and income (Figures 3d and 3e). On the other hand, a decline in risk in the financial sector (measured by bank stock market volatility) helps sustain spending in the medium run (Figure 3f).

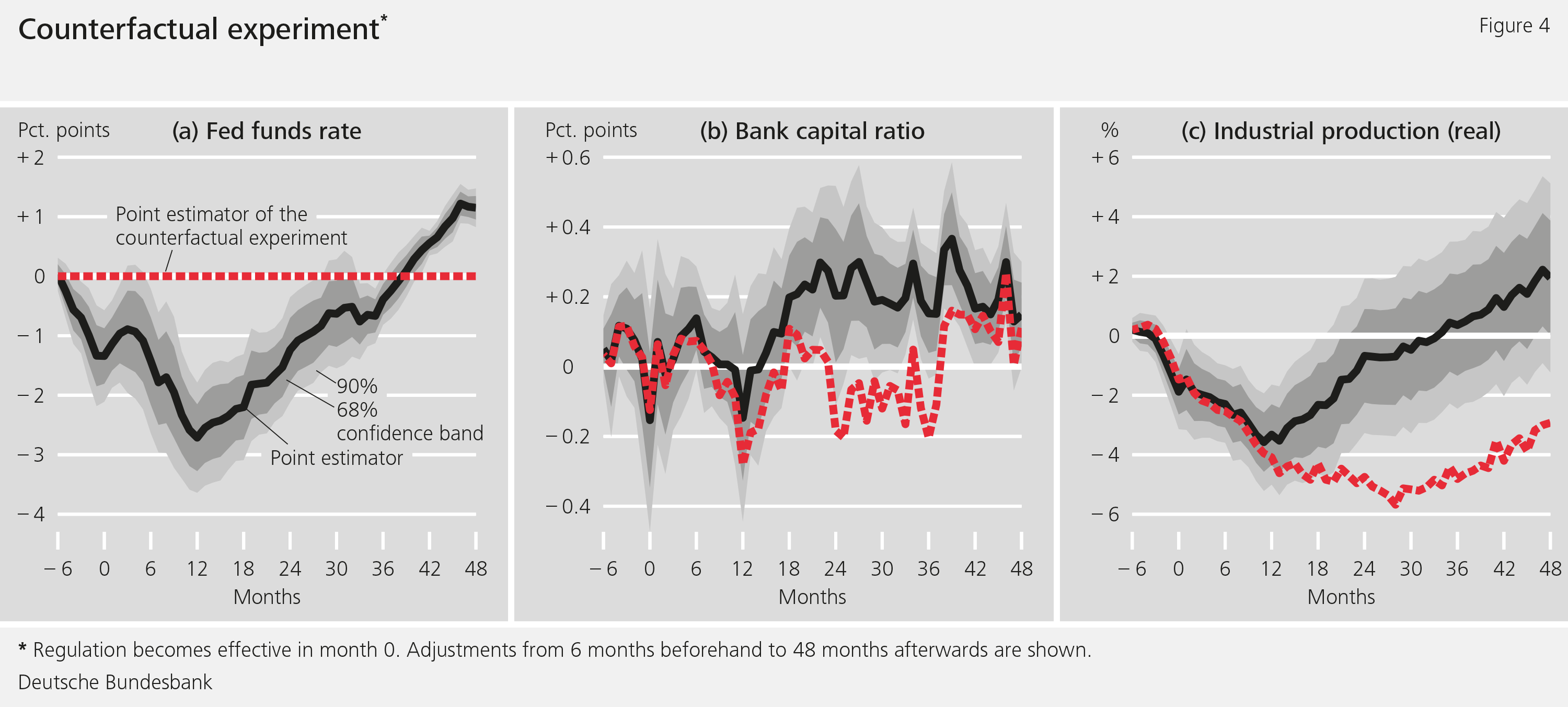

In a counterfactual experiment, we assume that the US fed funds rate is restricted not to move after the regulatory events. The result of this can be seen in Figure 4, in which the red dotted line shows the results of our experiment without a policy rate cut, while the black line shows our previous findings (Figure 4a). Had the Federal Reserve not reduced the fed funds rate, the bank capital ratio would not have gone up until much later (Figure 4b). In this case, industrial production would have fallen more and for a longer period of time (Figure 4c). Thus, by stimulating the economy, a policy rate cut gives banks the scope to increase their capital ratio more quickly and also cushions the negative effects of a capital requirement tightening on the loan supply (not shown) and industrial production. Monetary policy is effective with a time lag because a change in the policy rate has a delayed effect on the economy.

Conclusion

Tighter capital requirements are an important instrument in order to stabilise the financial system and thus avoid the onerous economic cost of financial crises. Our analysis for the United States suggests that a permanent increase in bank capital ratios has only a temporary effect on the credit market and the real economy. After an adjustment period, the banking system is better capitalised and less risky with no additional running costs to the macroeconomy. Because the better capitalisation of the banking system cuts the costs of financial crises, this also means that tighter capital requirements could have positive effects in the long run. What our results also imply is that the temporary negative effects of tighter capital requirements could be larger if policy rates are already very low and cannot be reduced any further.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Admati, A. and M. Hellwig (2013): The Bankers’ New Clothes, Princeton: Princeton University Press.

- Aiyar, S., C. W. Calomiris, and T. Wieladek (2014): Does Macro-Prudential Regulation Leak? Evidence from a UK Policy Experiment, Journal of Money, Credit and Banking, 46(1), pp. 181-214.

- Bahaj, S. and F. Malherbe (2018): The Forced Safety Effect: How Higher Capital Requirements Can Increase Bank Lending, London School of Economics, mimeo.

- Begenau, J. (2018): Capital Requirements, Risk Choice, and Liquidity Provision in a Business Cycle Model, Stanford GSB, mimeo.

- Calomiris, C.W. (2015): Is a 25% bank equity requirement really a no-brainer?, in J. Danielson (ed.), Post-Crisis Banking Regulation, CEPR – VoxEU.org eBook, 2015, Chapter 2.5, pp. 73-79.

- Eickmeier, S., B. Kolb and E. Prieto (2018): The macroeconomic effects of bank capital regulation, Deutsche Bundesbank Discussion Paper No 44/2018.

- Reinhart, C. M., and K. S. Rogoff (2009): This Time Is Different: Eight Centuries of Financial Folly, Princeton: Princeton University Press.

| The authors | ||

| Sandra Eickmeier Research economist at the Research Centre of the Deutsche Bundesbank | Benedikt Kolb Research economist at the Deutsche Bundesbank, Directorate General Financial Stability | Esteban Prieto Research economist at the Research Centre of the Deutsche Bundesbank |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

487 KB, PDF