Two stress tests examine the resilience of German banks to a drop in real estate prices Research Brief | 19th edition – June 2018

German credit institutions are sufficiently capitalised to deal with potential losses from their residential mortgage exposures that could arise if house prices, which have been rising strongly since 2010, were to fall sharply. This is shown by the results of two current stress tests that have been developed by Bundesbank experts for risk analyses.

In the past seven years, price developments in the German real estate market have garnered more and more public interest. According to recent Bundesbank estimates, overvaluations in German towns and cities have been running at between 15% and 30% (Deutsche Bundesbank, Monthly Report, February 2018). Housing loans constitute a significant proportion (around 30%) of overall lending, which is why systematic defaults on housing loans may lead to heavy losses at banks. In this context, stress tests help banking supervisors to assess whether banks are sufficiently capitalised to cope with such losses when a crisis hits.

Two current Bundesbank studies each present a stress test model that has been developed to assess the risks from real estate mortgage exposures. In both models, we use the same macroeconomic stress scenario in which house prices fall by 30% and the unemployment rate rises from less than 5% to nearly 8%. We simulate the stress effect over a horizon of three years (2017-19). Despite having different approaches, the two studies arrive at very similar results in both qualitative and quantitative terms. In the final year of the stress scenario, the institutions would, on average, suffer losses of 0.7 to 1 cent per euro of outstanding residential mortgage loans. These losses would lead to a considerable reduction in the capitalisation of German credit institutions. On aggregate, their common equity tier 1 capital ratio would fall by around 0.6 to 0.9 percentage point, solely as a result of these losses on housing loans. On average, the common equity tier 1 capital ratio at the end of the stress horizon would be between 14.5% and 14.7%, and thus far above the regulatory minimum capital requirements. The institutions would therefore be sufficiently capitalised to cope with the housing loan losses arising in such a macroeconomic stress scenario.

Complementary strengths of the two models

Like all forecasts, stress tests entail an element of model and estimation uncertainty that cannot be ignored. The results of these tests are also determined in large part by the informative value and granularity of the data used to translate a macroeconomic stress scenario into expected losses for banks. The two stress tests differ in regard to the data used and thus also in regard to their modelling framework. This way, the strengths of both approaches can complement each other and it is possible to mitigate the influence of model-specific inaccuracies on the results. This increases the qualitative and quantitative robustness of the stress test results.

Both analyses are based on the same fundamental idea. We calculate the expected losses for banks by multiplying the probabilities of default and the loss given default – ie the share of uncollateralised exposures in defaulted exposures – with outstanding loans. In both studies, the probability of default and loss given default are modelled conditional on the macroeconomic scenario. As most individuals who have taken out a housing loan derive their income primarily from employment, the probability of default strongly depends on the risk of unemployment. By contrast, loss given default depends on the outstanding amount of the loan and the value of the property serving as collateral for the bank.

Thomas Siemsen and Johannes Vilsmeier, the authors of the first of these Bundesbank studies, draw on the results of the Bundesbank’s survey on residential real estate lending for their model. These data were collected through the Bundesbank’s low-interest-rate environment survey for the first time last year. As part of this survey, all banks supervised by the Bundesbank (banks supervised by the ECB did not take part) provided detailed information on the expected probabilities of default and the loan-to-value ratios (ie the ratio of the loan amount to a given property’s mortgage lending value). Nataliya Barasinska, Philipp Haenle, Anne Koban and Alexander Schmidt, who developed the second stress test, draw on data from the Bundesbank’s reporting system for their model. These data are less granular but are available on a regular basis and also cover a longer period of time. This allows them to assess the risks from housing loan exposures on an ongoing basis. With the new data from the low-interest-rate survey, it is now possible to compare the stress test results based on the real estate survey data with those based on data from ongoing monitoring of risks in the housing loan portfolios.

Model framework reduces influence of model uncertainty on stress test results

General forecasting uncertainty is intensified in the case of stress tests because the projections concern events that have a very low probability of occurrence. There are only very few, if any, historical observations that can be drawn on. For this reason, forecasts, which are usually based on the extrapolation of historical, observed correlations, may be less robust under these circumstances.

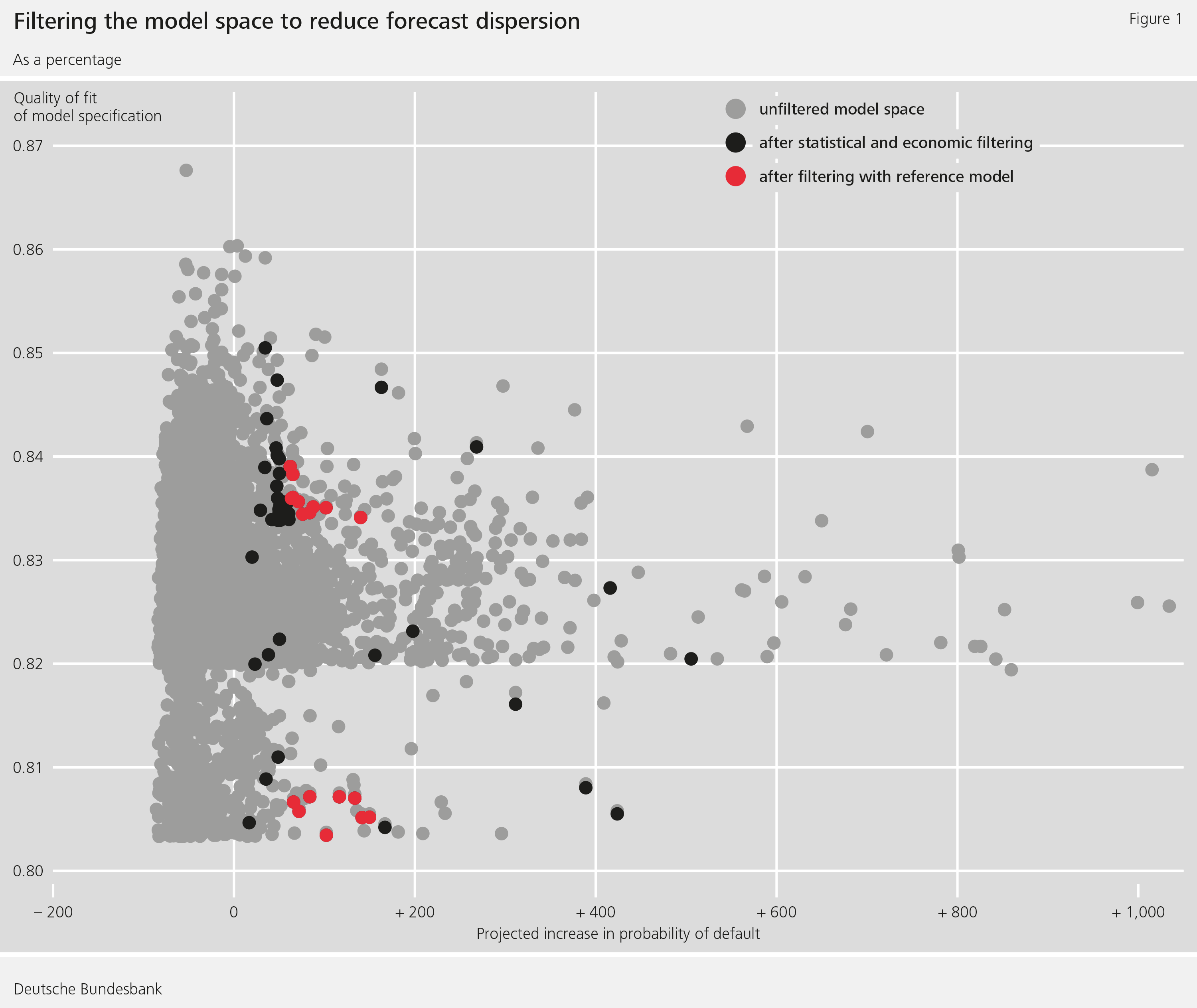

To address this issue, Siemsen and Vilsmeier develop a model framework that adds a second model-theoretical component to the usually purely econometric component of stress test forecasts. In modelling the bank-specific probabilities of default in the stress scenario, they first estimate a large number of different model specifications (rather than one single specification) of an econometric standard model. These are subsequently filtered for statistical and economic plausibility, as well as for “stress test plausibility” and finally combined to one single model specification.

The idea is to disregard those specifications that lead to distorted estimation coefficients (lack of statistical plausibility) or which, say, forecast a fall in the probability of default after a sharp rise in the unemployment rate (lack of economic plausibility).

In addition, the stress forecasts are compared to those of a second credit risk model (Merton-Vasicek one factor model), which produces forecasts less reliant on historical correlations but rather on economic mechanisms. Specifications that do not appear plausible relative to this reference model are also filtered out. The model therefore combines an econometric and a theoretical perspective, thus reducing the degree to which the stress test forecast depends on observed historical correlations which, owing to the adverse nature of the stress scenario, have less informative value than they do for normal economic forecasts.

Model framework takes into account regional differences

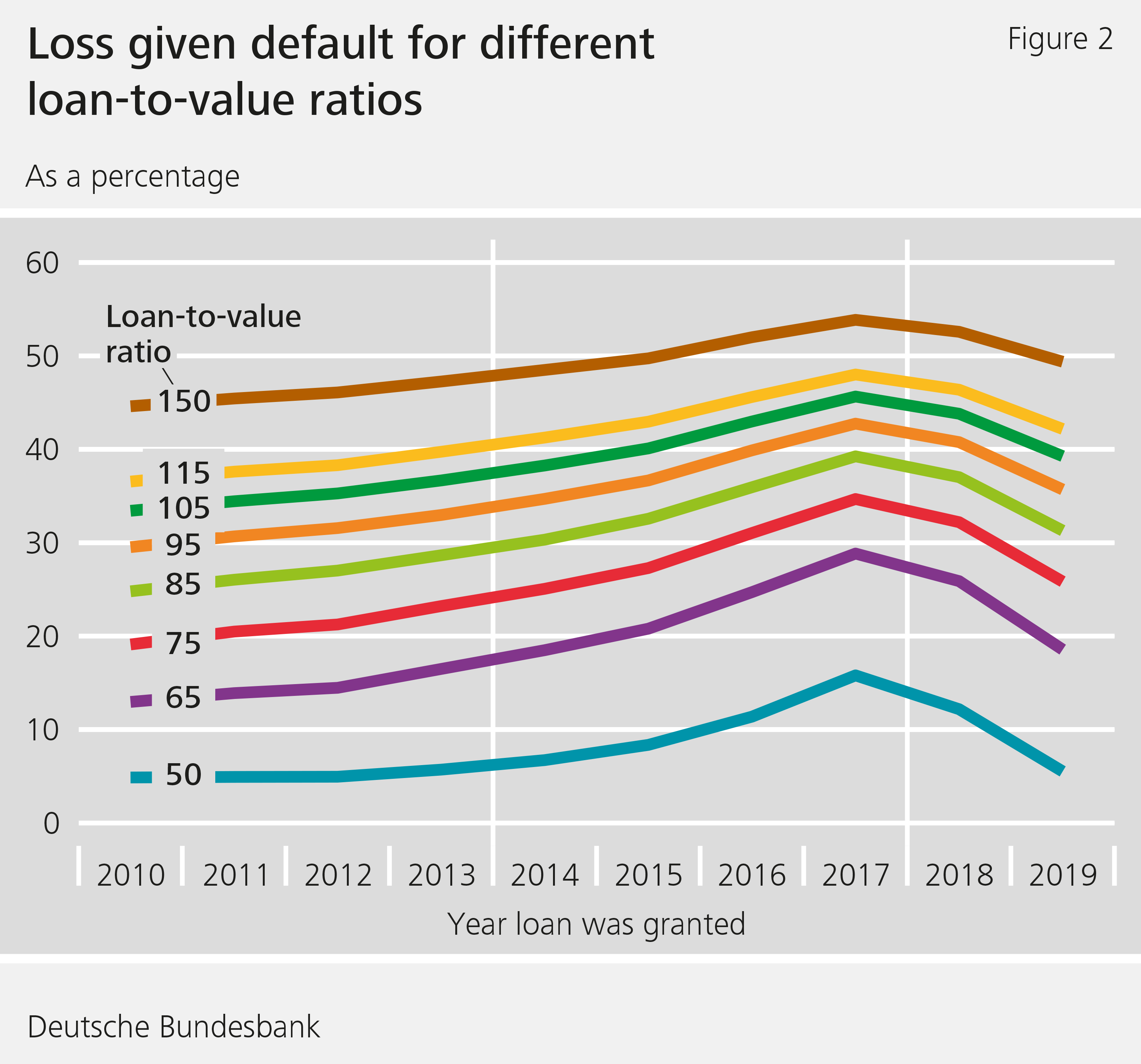

Besides probability of default, loss given default plays a key role when it comes to analysing credit risk. If a loan defaults, the property assigned as collateral for the loan is repossessed. If the selling price is lower than the outstanding loan amount and no other assets can be drawn upon, the bank suffers a loss. Here, Barasinska et al use only the value of the property in their estimates, meaning that the estimated loss represents an upper limit. The principal repayments reduce the outstanding loan amount over time, thereby reducing the potential loss for the bank. At the same time, however, the value of the property also changes. In turn, this has an impact on the size of the potential losses: when the economy is in good shape, demand for housing, and thus also prices, are likely to be higher, and the loss given default lower. In economic downturns, prices are likely to be lower, meaning that losses are higher. Barasinska et al take this into account and also factor regional differences into their stress test. They consider whether the property is in an area in which prices have risen sharply, or where they have grown more moderately, over the last few years.

Principal repayments and fluctuations in property prices therefore influence the loss a bank would suffer if a borrower could no longer service their loan.

Taking these relationships into account, Barasinska et al find that the loss given default calculated in the assumed negative macroeconomic scenario would be around 22 percentage points higher on average than under normal conditions. Together with a simulated rise of around 2 percentage points in the probability of default, this would cause banks’ common equity tier 1 capital ratio to fall by around 0.8 percentage point on average to roughly 14.7%. Overall, the projected losses of German banks would be sustainable, as the minimum capital requirements would still be met.

Conclusion

The results of our stress tests show that German credit institutions have sufficient capital to withstand a decline in real estate prices of 30% without encountering serious problems; the regulatory minimum capital requirements would not be breached. The close similarity between the results of both tests, despite the differences in data and modelling, suggests that the findings are not biased by the data or modelling choice. It should be noted that the tests only capture the stress effect on the portfolios of housing loans. Potential spillover effects between loan portfolios and institutions are not taken into account. The results of the stress tests thus represent a lower bound in terms of stress impact and remain largely silent on implications for financial stability.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Barasinska, Nataliya, Philipp Haenle, Anne Koban & Alexander Schmidt (2018), Stress testing the German mortgage market, Bundesbank Discussion paper (forthcoming)

- Siemsen, Thomas & Johannes Vilsmeier (2017), A stress test framework for the German residential mortgage market – methodology and application, Bundesbank Discussion Paper No 37/2017

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

3 MB, PDF