How firm productivity impacts on the optimal inflation rate Research Brief | 14th edition – August 2017

The productivity of many firms evolves over time. This impacts on the optimal inflation rate – the rate of price increase with the least distortionary effect on relative goods prices. Our estimates for the United States suggest that, due to firm-level productivity changes, the optimal inflation rate has dropped from somewhat over 2% in the mid-1980s to a current level of roughly 1%.

What is the optimal inflation rate – the rate of price increase with the least distortionary effect on relative prices? This is a classic question in the field of macroeconomics which has, unsurprisingly, attracted broad debate in the literature. But there is one factor which has been disregarded hitherto – firm-level productivity trends. To gain a clear picture of the role these trends play, our paper concentrates on how they interact with optimal trend inflation and disregards other determinants of the optimal inflation rate such as the effective zero lower bound on interest rates, downward rigidity in nominal wages, or price index mismeasurement. Other issues we have chosen not to explore in our paper include the question whether monetary policy needs to move the inflation target into line with these trends, and which inherent problems (eg in terms of credibility) this would involve.

We use a conventional model framework in which the optimal inflation rate is zero if no firm-level productivity trends are present. If we then extend this framework by adding productivity trends which firms and their goods experience during their lifetime, the optimal inflation rate climbs to levels well above zero. Our estimate for the United States, based on this extended model framework, has found that firm-level productivity trends do indeed impact positively on the optimal inflation rate, which has dropped from somewhat over 2% in the mid-1980s to a current level of around 1%.

Life cycles and the inflation rate

Goods and firms undergo life cycles. This manifests itself in two ways. One is that new products or products with substantial quality improvements are often manufactured using state-of-the-art technology, meaning they are potentially produced in a highly efficient manner. This technology becomes outdated over time, however, causing the relative productivity of the formerly new products to diminish. Another is that new technologies often require extended learning phases before their efficiency gains come to full fruition. What this suggests, on the other hand, is that new products are initially manufactured less efficiently than established products, and only benefit from efficiency gains over time.

The net effect of these two productivity development paths at firm level needs to be measured empirically, and is reflected, at least in part, in the price of a given good. This is set by a firm when it launches the product, but it is only adjusted infrequently in most cases thereafter.

The aggregate inflation rate is composed of changes in the prices of a representative basket of goods; these changes can occur for a wide variety of reasons. One possible reason is product substitution, where goods in the basket are replaced by newer ones because, for instance, demand for the substituted good has evaporated. Assuming the new good is initially produced less efficiently and thus has a relatively higher price tag than the good it is replacing, product substitution will drive up the inflation rate.

In our study, we show that price changes caused by product substitution alter the optimal inflation rate in the same manner as the actually observed inflation rate. There are two reasons for this. One is that price changes caused by product substitution reflect differences in productivity between new and substituted goods. Therefore, these price changes do not lead to relative price distortions but are justified. The other is that price changes caused by product substitution do not generate any additional costs as firms will, at any rate, have to set new prices for new goods. Normal changes in the prices of already existing goods, however, often create additional costs since, for instance, dissatisfied customers stop buying these goods or the relative prices are distorted.

New goods often have only a small market share and come at prices which start out relatively high and only come down over time. What these observations mean in our model framework is that new goods are, at the outset, manufactured relatively inefficiently, with efficiency gains in production being achieved only with the passage of time. This suggests that product substitution often leads to price increases, thereby raising the optimal inflation rate.

How strong is the effect?

We use a detailed dataset for the United States, one that provides information on firm-level employment for the entire private sector. We also make various assumptions so that, by means of these data, we can measure physical firm productivity. It would be better, of course, to measure this directly. However, the necessary data, if they do exist, are available only for niche sectors. We therefore use our own productivity measure to estimate the optimal US inflation rate.

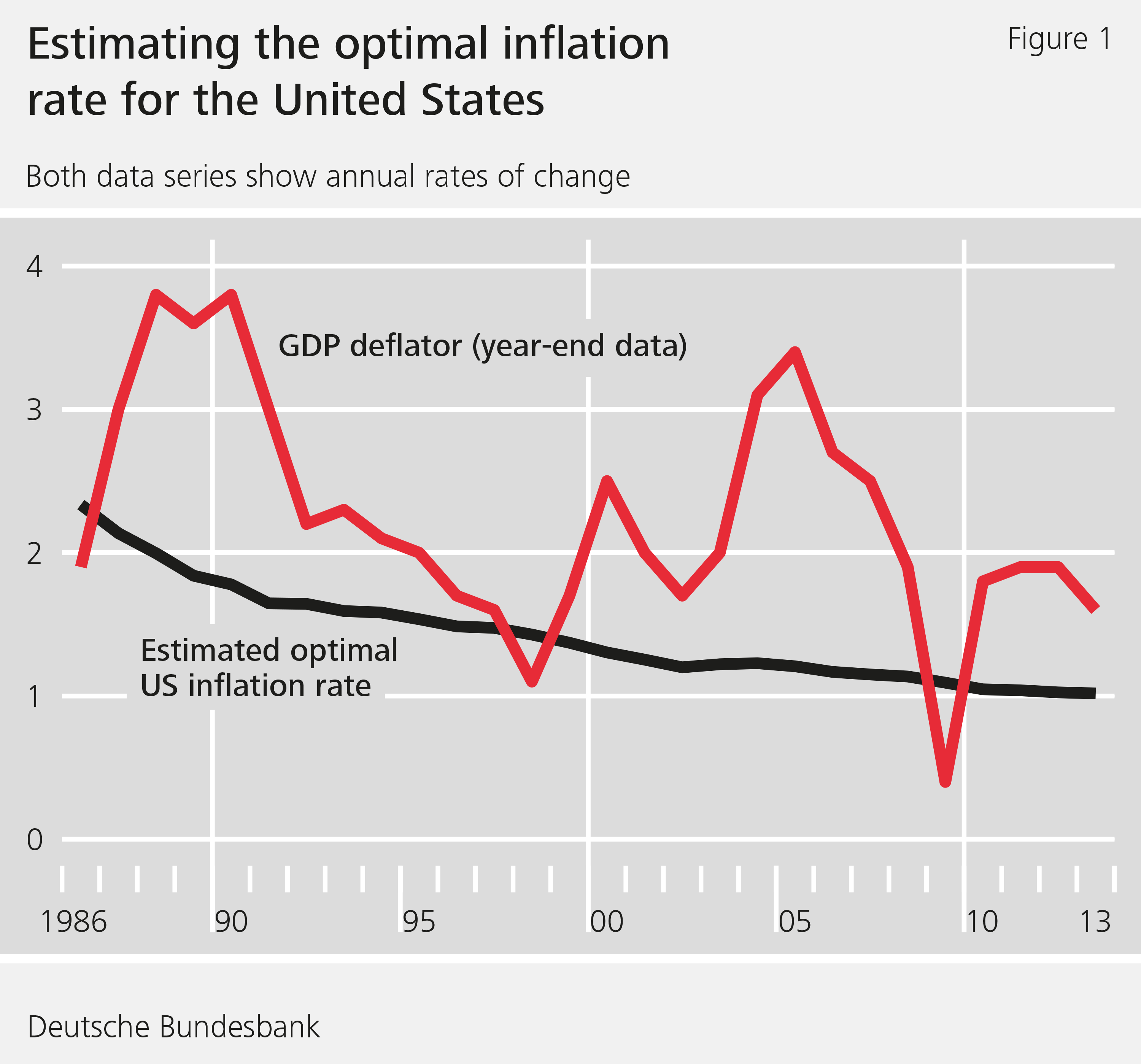

Figure 1 shows our estimate of the optimal inflation rate together with the growth rate of the GDP deflator, a measure of inflation, for the United States. For the mid-1980s, our estimate gives us a figure of slightly over 2% per year, which is very close to today’s inflation targets. From the mid-1980s to 2013, according to our estimates, the optimal inflation rate for the United States dropped to roughly 1% per year, however (estimation uncertainty comes to just a few basis points and is therefore not shown). This downward trend appears to coincide with a downward trend in the growth rate of the GDP deflator.

What does this estimate of the optimal US inflation rate tell us? It shows that while new goods are produced less efficiently than mature ones, this efficiency gap has narrowed considerably and to a statistically significant extent in the past few decades. Price inflation caused by product substitution should therefore ideally diminish over time. The product substitution rate has two counterbalancing effects which, in our model framework, cancel each other out and should therefore be empirically negligible. Although more product substitution increases the optimal inflation rate because more goods with relatively high prices appear, at the same time it shortens the life cycle of existing goods, capping the potential efficiency gains in production and therefore reducing the optimal inflation rate.

The downward trend in our estimate of the optimal inflation rate provides a further potential approach to explaining the persistently low rates of inflation: technological advances, which slowly feed into the economy through, in particular, new goods and firms, lead to protracted downward pressure on aggregate price levels.

Conclusion

Further research will be necessary to understand whether these findings are borne out by alternative measurement methods and datasets, and whether similar developments can be identified for other countries, especially in Europe. Nonetheless, our analysis does give some food for thought. One thing it shows us is that aggregated data only go so far in helping to identify the optimal inflation rate. Firm-level microdata, which allow inferences as to which price changes are fundamentally justified and which are not, are generally more useful in this regard. Our analysis also indicates that structural change and structural policy, which impact on firm-level technological progress, can have a prolonged impact on the optimal inflation rate.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Adam, K & Weber, H, 2017. "Optimal trend inflation", Deutsche Bundesbank Discussion Paper (25).

| Die Autoren | |

|

|

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

135 KB, PDF