Monetary policy effectiveness in times of financial market volatility Research Brief | 11th edition – March 2017

The years following the 2007-08 financial crisis saw central banks in the United States and other industrialized countries adopt highly expansionary monetary policy measures in an effort to stimulate the economy. But how effective have those policies been? A new study explores how effective an expansionary monetary policy stance can be in such turbulent times.

The period following the financial crisis saw the US Federal Reserve adopt an expansionary monetary policy stance – an extremely low federal funds rate in tandem with a raft of non-standard measures – in an effort to stimulate the economy. And yet in spite of these highly accommodative monetary policy measures, the economy has only recovered at quite a sluggish pace from the crisis. This sparked a debate over whether the effectiveness of monetary policy during spells of heightened financial market volatility might be overstated. Our study investigates whether monetary policy is less effective in times of high volatility in financial markets than it is during quieter spells.

Our empirical analysis uses a regime-switching vector autoregression model and is based on US data such as gross domestic product (GDP), investment, the federal funds rate and the credit spread. The model distinguishes between two recurring regimes: one that is characterised by strong financial market volatility and one that isn’t. The procedure permits a wide variety of interactions between the variables used and thereby enables us to identify how the two scenarios differ in terms of monetary policy effectiveness.

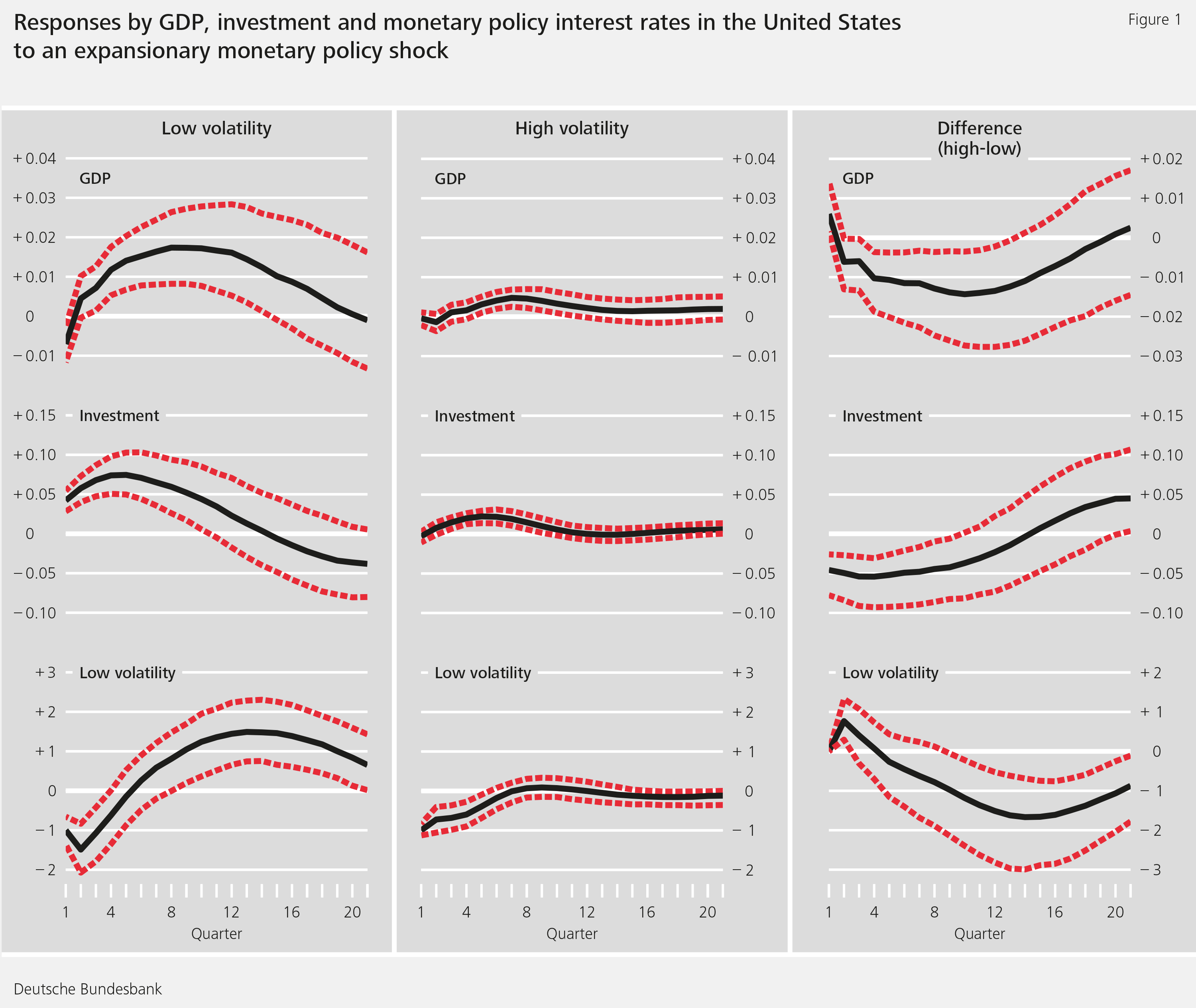

The results of our empirical analysis show that, in the United States, an expansionary monetary policy stance in the shape of an unexpected reduction in the federal funds rate in times of low volatility leads to a boom in investment and output, while an identical reduction in interest rates in times of high volatility has far less of an impact on investment and output (Figure 1). We also find that the differences in the responses shown by the variables are statistically different from each other.

Expansionary monetary policy more effective when financial market volatility is low

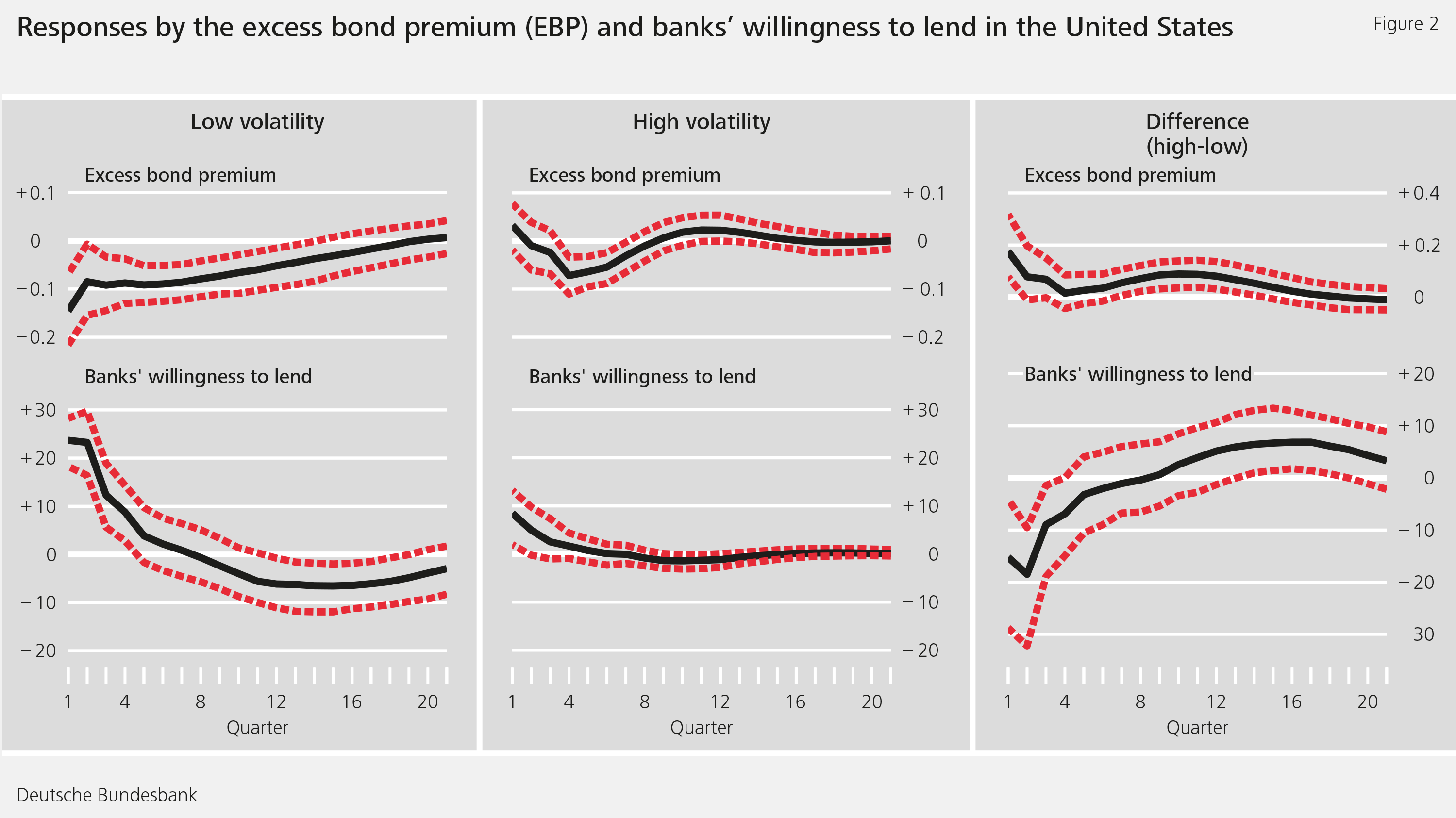

The differences between the regimes can be explained by the fact that unexpected reductions in the federal funds rate in times of low volatility are more effective at improving funding and credit conditions. This is demonstrated by Figure 2, which shows that both the excess bond premium (EBP) and banks’ willingness to lend are more responsive to the reduction in the federal funds rate in times of low volatility than they are when volatility is high.

Structural model helps explain empirical results

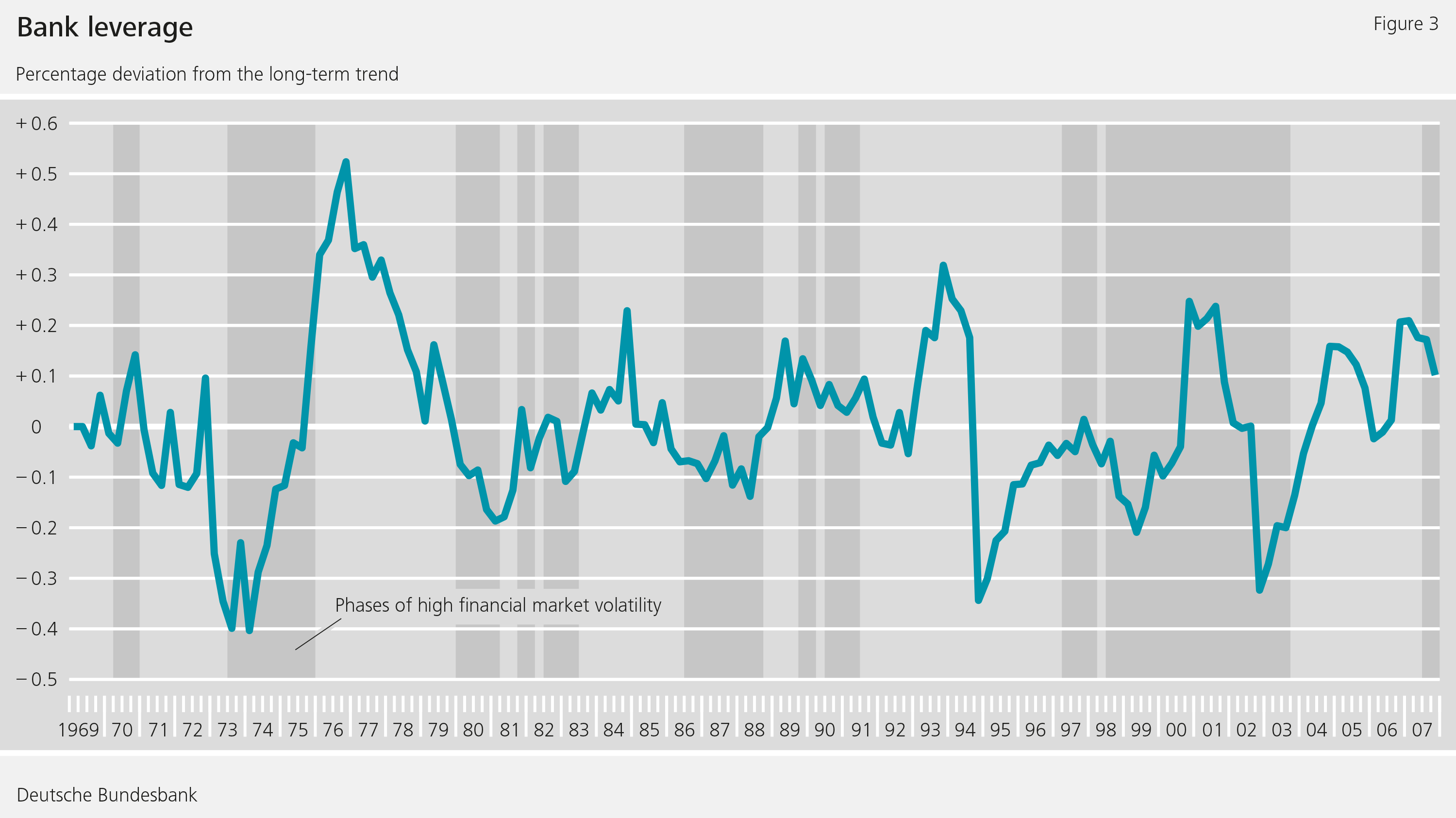

We use a general equilibrium model to provide a structural explanation for our empirical results and show that our empirical results are consistent with the implications of this theoretical model. The model assumes that banks opt for low leverage in times of high volatility and for high leverage when volatility is low. As Figure 3 shows, this procyclical behaviour on the part of banks is a hallmark of the US financial system.

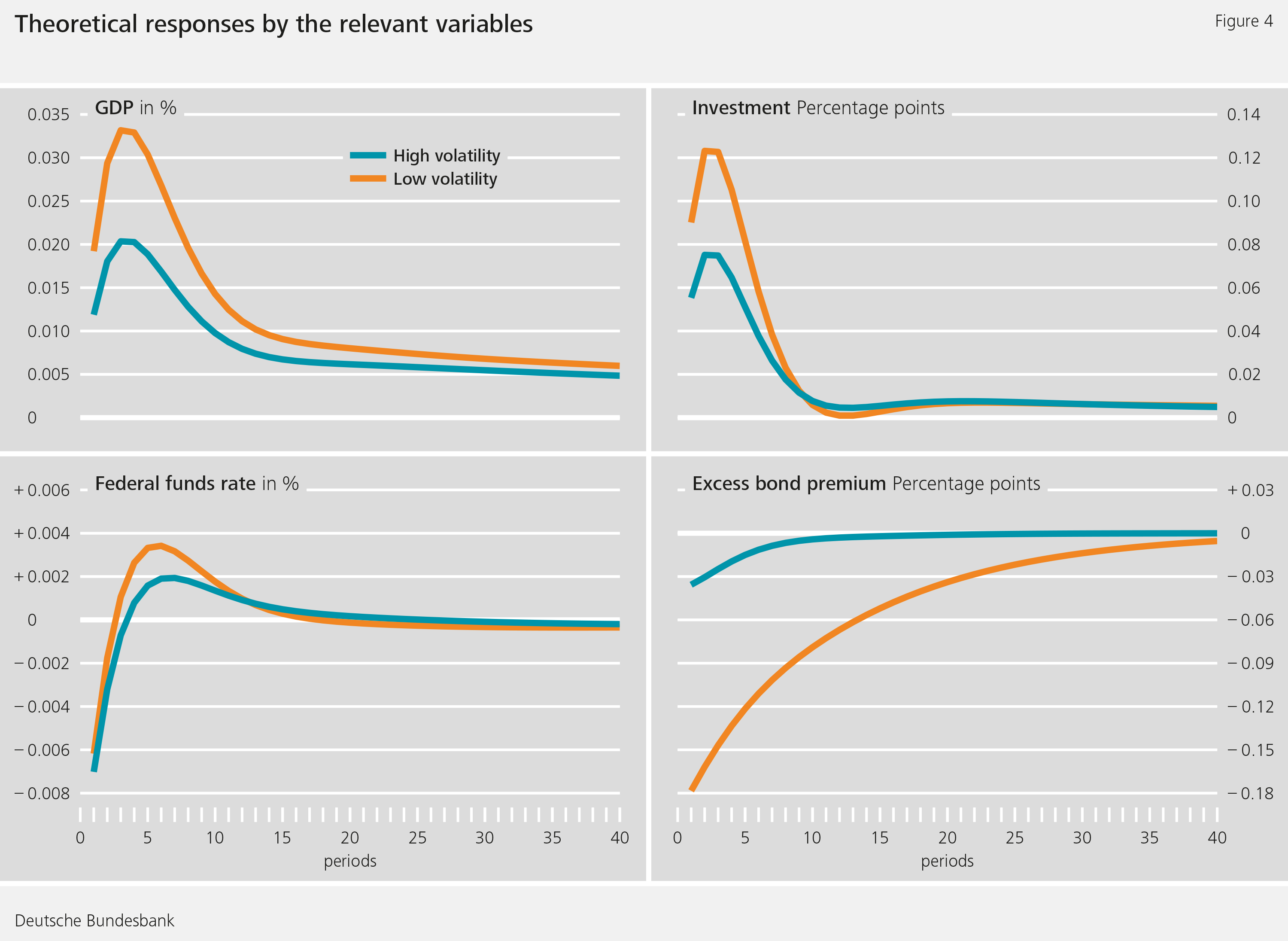

Banks run down their leverage in times of strong volatility since a higher level of equity capital hedges them against fluctuations in asset values. The consequence of this, however, is that an unexpected reduction in the federal funds rate causes the present value of banks’ future income flows to rise at a flatter pace, relatively speaking. This, in turn, pushes down the rate at which they raise their supply of credit. In times of low volatility, on the other hand, banks increase their leverage since they consider risk to be low. In this case, an unexpected reduction in the federal funds rate yields a relatively strong increase in the present value of future income flows. This then allows banks to take on even more debt and boost their supply of credit to a much greater degree, see Figure 4.

Conclusion

Our study uses empirical evidence to demonstrate that reductions in the federal funds rate in times of heightened volatility are less effective at stimulating the economy. This finding can be explained with the aid of a theoretical model in which banks strengthen their capital positions and supply less credit during spells of uncertainty. That is not to say that expansionary monetary policy is completely ineffective in supporting the economy in times of high volatility. Instead, a higher degree of monetary policy stimulation would be needed in times of elevated volatility to achieve the same effects on the real economy as in times of low volatility. Our study does not, however, explore the effectiveness of asset purchase programmes. A number of new papers indicate for the United States that fiscal policy is more effective in times of high volatility than it is in times of low volatility (Auerbach and Gorodnichenko, 2012; Canzoneri et al, 2016). Fiscal policy could therefore play a supplementary role in stimulating the economy during such periods.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Auerbach, A J and Y Gorodnichenko (2012): Measuring the output responses to fiscal policy, American Economic Journal: Economic Policy, Vol 4, pp 1-27.

- Canzoneri, M, F Collard, H Dellas and B Diba (2016): Fiscal multipliers in recessions, The Economic Journal, Vol 126, pp 75-108.

- Eickmeier, S, N Metiu and E Prieto (2016): Time-varying volatility, financial intermediation and monetary policy, Bundesbank Discussion Paper No 46/2016 and CAMA Working Paper 2016-32.

The authors | ||

Norbert Metiu | Sandra Eickmeier | Esteban Prieto |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

170 KB, PDF