How financial shocks affect inflation Research Brief | 9th edition – January 2017

Demand in the USA and other industrial nations collapsed dramatically during the financial crisis and yet this did not lead to deflation. The reasons for this have still not been fully explained. A new study examines the extent to which financial shocks have a bearing on the path of inflation.

In economic theory, there is some dispute over whether financial shocks influence the aggregate inflation rate positively or negatively. "Financial shocks" refer to those unexpected macroeconomic developments which drive up credit growth and asset prices and reduce borrowing costs. The results produced by models depend on the transmission channels they incorporate. In our new study, we attempt to resolve the problem empirically; that is, we permit various transmission channels and, unlike many other studies, do not limit the response of inflation to financial shocks from the outset.

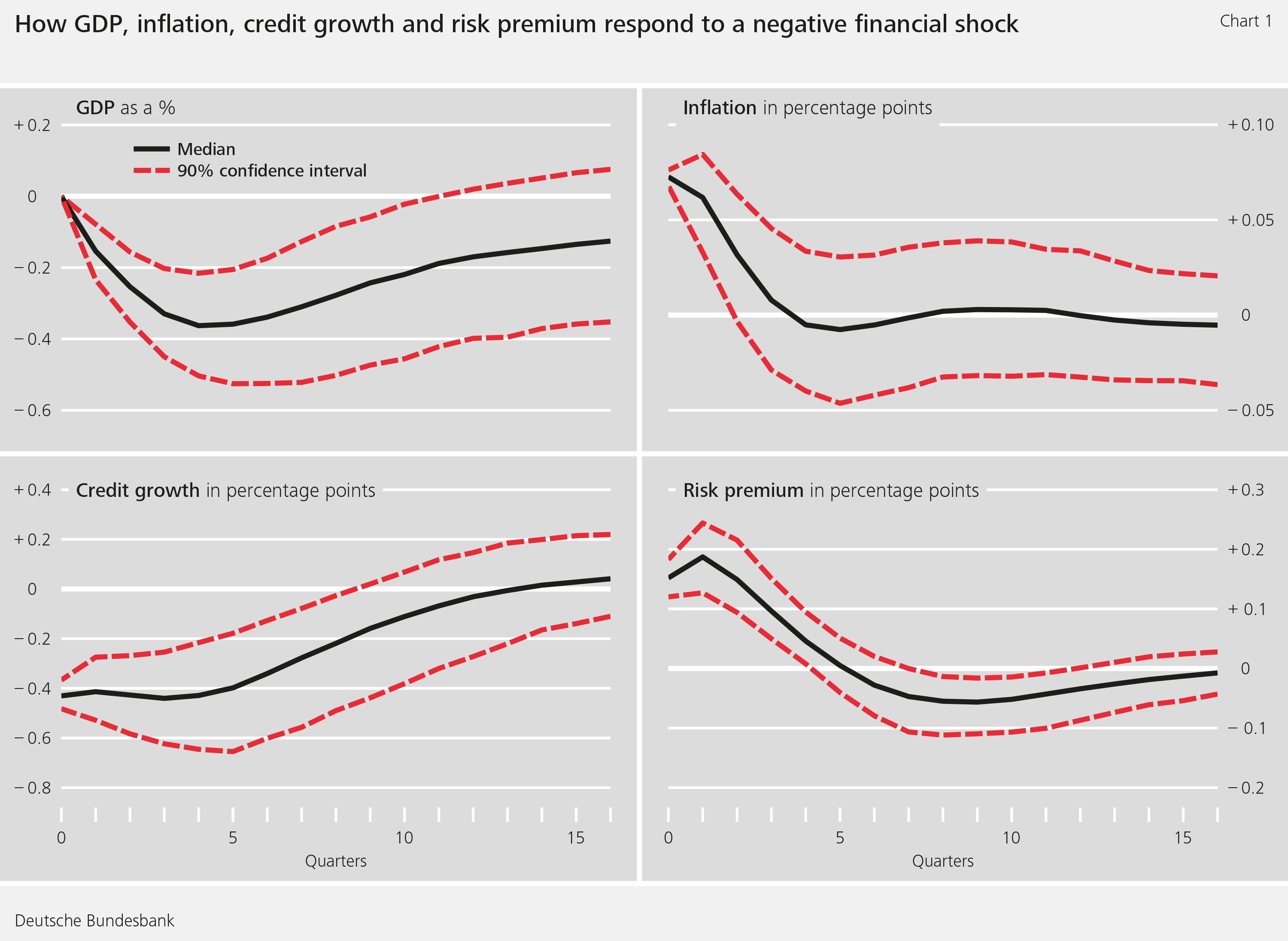

Our study uses a vector autoregressive model with data from the US economy and financial markets since 1988, such as gross domestic product, inflation and credit growth. This method permits a wide variety of interaction between the variables used and allows us to examine the effects of unexpected shocks on these variables. Chart 1 shows that a negative financial shock triggers a significant drop in credit growth and sends the risk premium for corporate bonds sharply higher. This, in turn, causes gross domestic product (GDP) to slump. Interestingly, the negative financial shock temporarily lifts the core inflation rate (CPI excluding food and energy).

The model also allows us to calculate the contributions made by financial shocks to the path of inflation: over the entire horizon, financial shocks explain 14% of the path of inflation. Between 2008 and 2011, they prevented a sharper decline in inflation. In other words, in the absence of financial shocks, the inflation rate during this period would have been around 0.1 percentage point lower on average, as shown in Chart 2. This means that other factors were behind the drop in inflation during the financial crisis.

Theoretical literature puts forward different approaches

This surprising result calls for a general explanation of the transmission channels through which financial shocks affect inflation. The theoretical literature approaches this topic in different ways: the transmission channels incorporated into the models help determine whether financial shocks will increase or lower inflation.

Our study investigates the question empirically while allowing all the transmission channels identified in the theoretical literature.

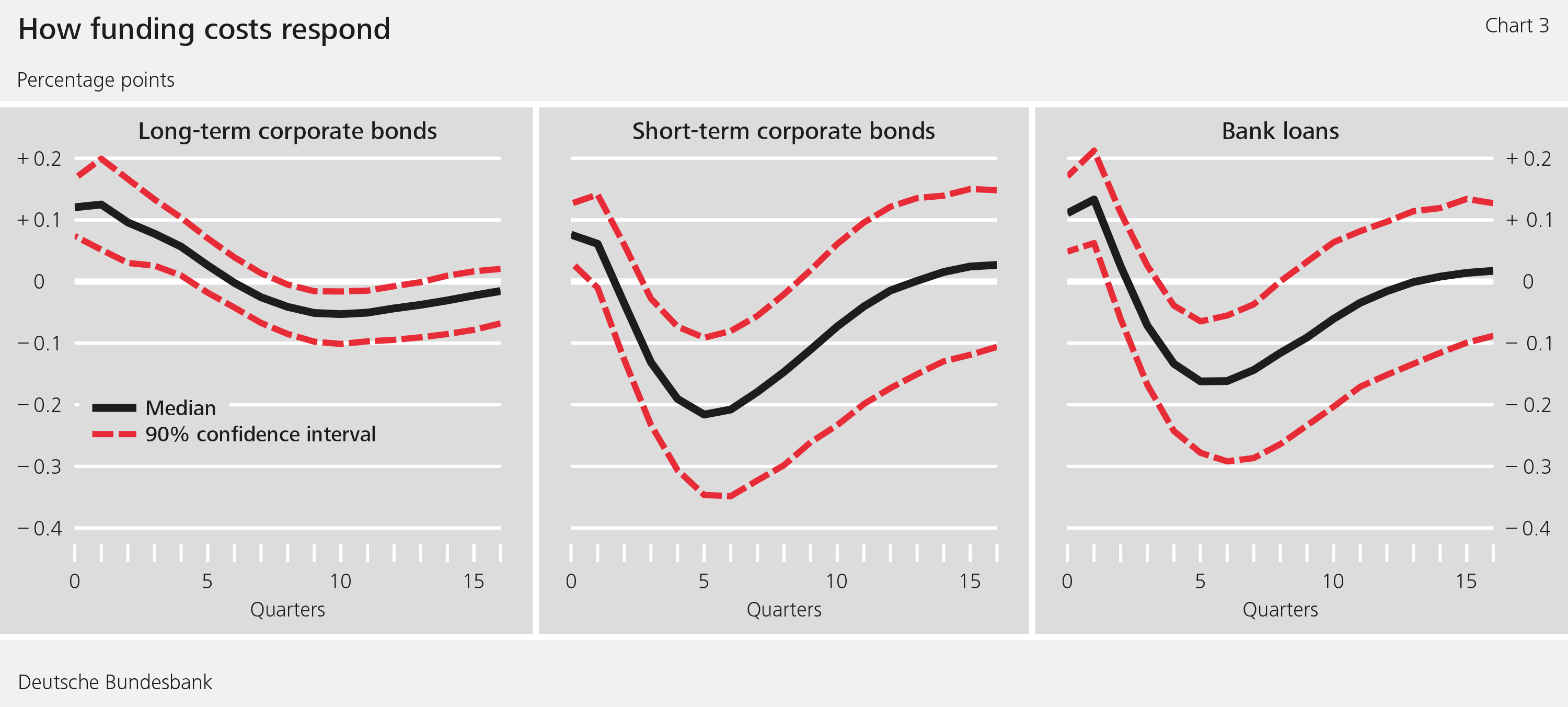

The study shows that it is the effects of the financial shock on enterprises' funding costs which explain the positive response by inflation to a negative financial shock. As shown in Chart 3, various credit instruments with differing maturity profiles (long-term and short-term corporate bonds and bank loans to enterprises) have interest rates which rise immediately after the financial shock before returning to their initial level a few quarters later. The higher funding costs, in turn, drive up enterprises' marginal costs, thus indirectly raising the sales prices, which causes the temporary increase in inflation (De Fiore and Tristani, 2013; Gilchrist et al., 2015).

Conclusion

Our study has two main findings: first, GDP and inflation move in different directions after financial shocks. GDP falls, while inflation rises slightly in the short term. This makes it more difficult for a central bank to pursue the right policies if it is looking to stabilise both inflation and the real economy. Second, a monetary policy which, say, aims to shore up financial markets in times of turmoil has to take into account a temporary drop in inflation when it reduces enterprises' funding costs.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Abbate, A, S Eickmeier, and E Prieto (2016): Financial shocks and inflation dynamics, Bundesbank Discussion Paper (41) and CAMA Working Paper 2016-53.

- De Fiore, F and O Tristani (2013), Optimal monetary policy in a model of the credit channel, Economic Journal, 123(571), 906-931.

- Gilchrist, S, R Schoenle, J W Sim, and E Zakrajsek (2015), Inflation dynamics during the financial crisis, Finance and Economics Discussion Paper Series 2015-12, Board of Governors of the Federal Reserve System.

| The authors | ||

Angela Abbate | Sandra Eickmeier Research economist, | Esteban Prieto Research economist, |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

3 MB, PDF