Banks that trade securities grant fewer loans Research Brief | 3rd edition – April 2016

In the United States and Europe, efforts are being made to limit banks' proprietary trading of securities. A key argument is that if banks invest in securities, they reduce the credit supply to the real economy. A new study uses microdata to examine the role of proprietary trading in times of crisis and its impact on lending activity.

Banks' proprietary trading of securities plays an important role in the international financial system. In Germany, for example, around 19% of commercial banks' total assets are invested in securities; in the United States, this figure is 20%. German credit institutions hold up to 89% of these securities for proprietary trading purposes (Langfield and Pagano, 2014). Concerns have often been raised that this practice – especially in times of crisis – could result in banks issuing fewer loans to the real economy (Shleifer and Vishny, 2010; Diamond and Rajan, 2011; Stein, 2013).

This criticism is based on the notion that, if their funds are limited, banks must make a choice regarding the asset class in which they invest. This is particularly true in times of crisis (Uhlig, 2010). The trade-off between risk and return is an important consideration here. If banks interpret crisis-related price volatility, distortions and panic selling on securities markets as temporary market developments, the purchase of these securities could promise a greater return and therefore encourage the banks to buy. Every euro used to purchase these securities is a euro that the banks no longer have available to invest in other asset classes – lending to the real economy, for instance.

This is one of the reasons why policymakers in both the United States and in Europe have drawn up, and in some cases already implemented, reform options such as the Volcker Rule (United States), the Vickers Report (United Kingdom) and the Liikanen Report (European Union) to restrict proprietary trading by banks.

However, there is no empirical evidence to date that demonstrates exactly how banks' proprietary trading changes in times of crisis and whether this does, in actual fact, reduce the credit supply to the real economy. These questions are the main focus of our analysis.

Data on securities and credit registers

In order to clarify the role played by banks' proprietary trading, data must be examined at the individual bank and borrower level.

This analysis requires, for example, that banks' proprietary trading be separated from securities-specific changes (such as outstanding volume, issuer risk, maturity, rating). In order to answer to the question as to whether and to what extent banks' proprietary trading of securities crowds out lending, information on which banks finance which borrowers at what point in time is also required. This is the only way of determining whether a potential decrease in lending by one bank to a borrower was not counteracted by another bank. Such a scenario would merely constitute a redistribution rather than a crowding-out. In our study, we therefore use a microdataset on commercial banks' securities and credit registers for the period from 2005 to 2012.

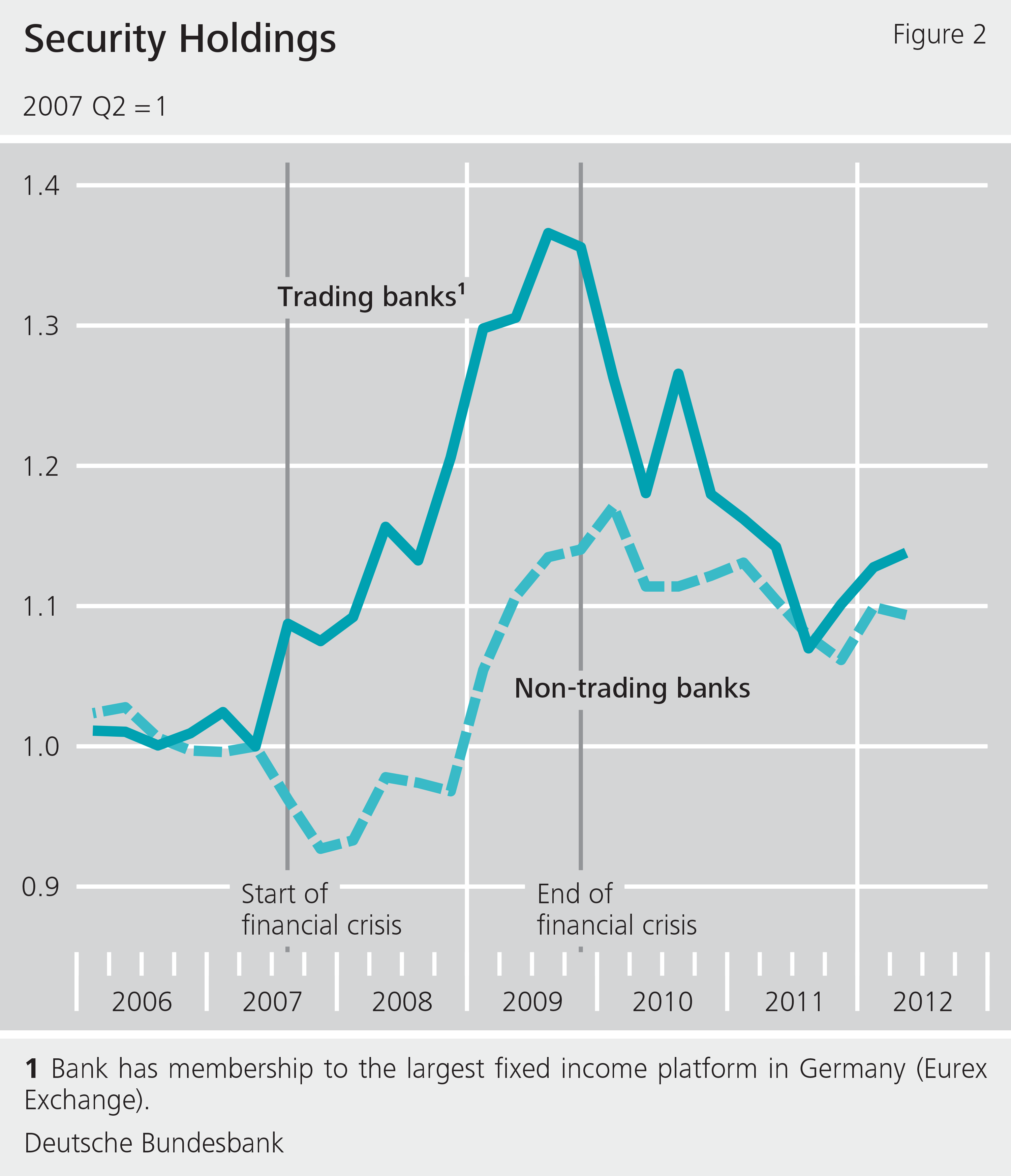

We find that banks with greater trading expertise ("more experienced trading banks") indeed expanded their securities investments in times of crisis more than other institutions. This applies especially to securities that fell in price. Banks that have a larger presence in the securities markets presumably have greater expertise in these markets and therefore are better able to identify undervalued or overvalued assets. We approximate trading expertise based on whether or not the institutions are direct members of the largest trading platform for bonds in Germany (Eurex Exchange).

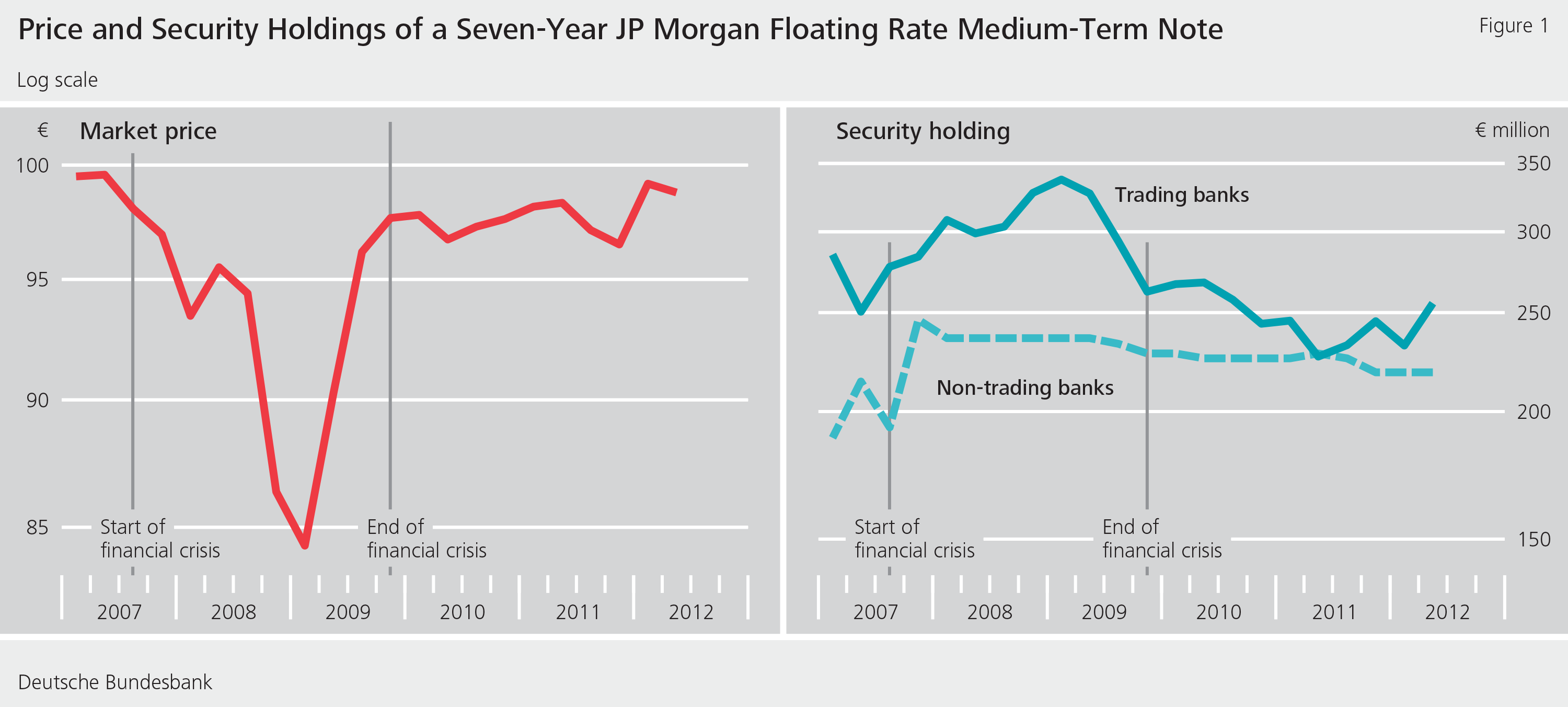

Figure 1 provides an example of this pattern, using the investments of German banks in a seven-year J P Morgan floating-rate medium-term note. Medium-term notes refer to debt securities with a maturity of one to ten years. Chart (a) shows the price development of the bond. Chart (b) depicts the total nominal holdings of that security by banks in Germany (in euro million). When the bond price fell after the collapse of the American investment bank Lehman Brothers in September 2008, those banks in Germany with greater trading expertise started increasing their holdings of the aforementioned security. After several quarters, the security reverted to its nominal value and the banks sold their holdings. Remarkably, we were unable to identify this development with other institutions, ie institutions with less trading expertise.

This is, of course, just one example, but our analysis of all the securities investments by banks in Germany painted a similar picture: banks with trading expertise increased their securities investments in times of crisis substantially more overall than other institutions (see Figure 2).

This effect was most visible for securities that had previously experienced a larger drop in price. The same was true for lower-rated and longer-term securities. Furthermore, we found that, of the banks with trading expertise, those with higher levels of equity capital engaged more in these trading activities. These trading activities indicate that banks potentially take on substantial risks. So did this strategy pay off in the crisis?

Analysis of lending activity

As things currently stand, banks with trading expertise that bought securities that had fallen in price were able to achieve an average return of 12% pa in the first quarter of 2009. The typical loan interest rate of these banks stood at around 5% pa during this same period. This suggests that, for banks, buying securities potentially led to higher returns than lending to the real economy.

The dataset we used also enabled us to study the potential effects of securities trading on the supply of credit. To this end, we used a specialised methodology (see, for example, Khwaja and Mian, 2008) to separate demand from credit supply, and analysed banks' lending to the real economy. In particular, we compared lending by different banks to the same enterprise during the same quarter. This enabled us to establish that the credit supply of "experienced trading banks" – in particular, institutions with a higher level of capitalisation – declined more sharply. Enterprises were not able to fully compensate for this lower supply by borrowing from other banks or issuing debt securities.

But do our results also suggest that restricting banks from trading in securities would ensure more loans are granted? This question ultimately focuses on the aggregate benefit of taking such a step, in connection with which other indirect effects also need to be considered. For example, banks take on risks if, in times of crisis, they buy securities that record greater declines in prices or have a low rating or longer maturity. These banks provide liquidity to the market and impede further devaluation, which means that these purchases could ultimately have a stabilising effect on the financial system. Moreover, this behaviour is more prevalent for institutions with higher levels of equity capital. If these banks are important players in the securities markets, our results suggest that restrictions on securities trading by banks could adversely affect the liquidity of these markets. There would then, for example, be fewer sellers in relation to buyers (or vice versa), which would increase the market risk and reduce the opportunities to buy or sell at a desired price.

Conclusion

In conclusion, our findings indicate that banks' securities trading activities during the crisis did, in actual fact, partially lead to the crowding-out of lending to the real economy. However, we also find evidence to suggest that these banks could be important players in the securities markets, whose proprietary trading activities provide liquidity to the market.

| Disclaimer |

| The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- P Abbassi, R Iyer, J-L Peydró and F R Tous (2015), Securities trading by banks and credit supply: micro-evidence, Journal of Financial Economics (forthcoming).

- D W Diamond and R G Rajan (2011), Fear of fire sales, illiquidity seeking, and credit freezes, Quarterly Journal of Economics, Vol 126, No 2, pp 557-591.

- A I Khwaja and A Mian (2008), Tracing the impact of bank liquidity shocks: evidence from an emerging market, American Economic Review, Vol 98, No 4, pp 1413-42.

- S Langfield and M Pagano (2014), Bank bias in Europe: effects on systemic risk and growth, ECB Working Paper, No 1797.

- A Shleifer and R W Vishny (2010), Unstable banking, Journal of Financial Economics, Vol 97, No 3, pp 306-318.

- J C Stein (2013), The fire-sales problem and securities financing transactions, Speech by Governor Jeremy C Stein at the Federal Reserve Bank of New York Workshop on Fire sales as a driver of systemic risk in triparty repo and other secured funding markets, New York, 4 October 2013.

- H Uhlig (2010), A model of a systemic bank run, Journal of Monetary Economics, Vol 57, pp 78-96.

{kind=link}

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein

1 MB, PDF