October results of the Bank Lending Survey (BLS) in Germany

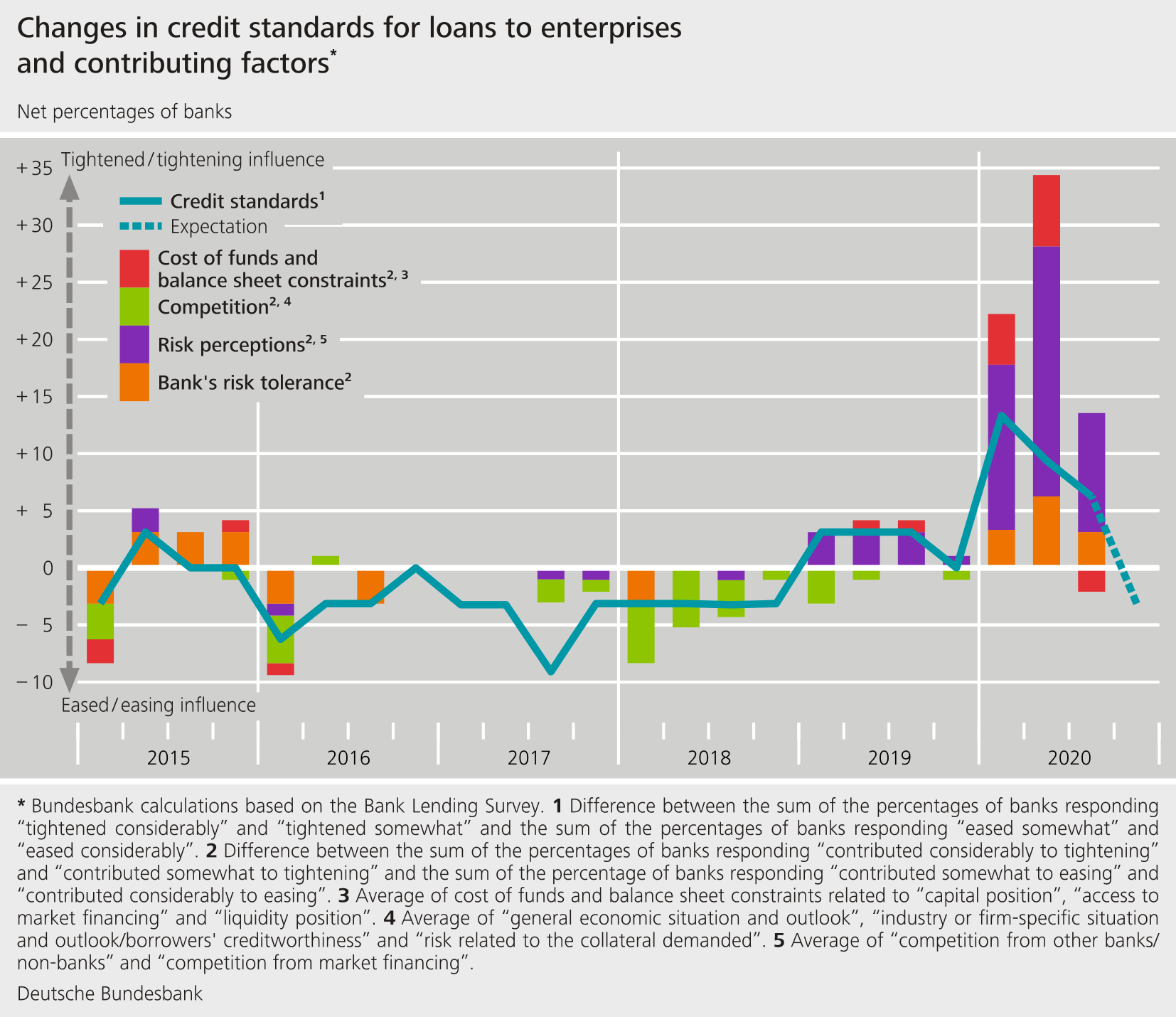

- The German banks taking part in the Bank Lending Survey (BLS) again tightened their credit standards in all surveyed loan categories (loans to enterprises, loans to households for house purchase, and consumer credit and other lending to households) in the third quarter of 2020. However, the tightening remained less pronounced than in the previous quarter.

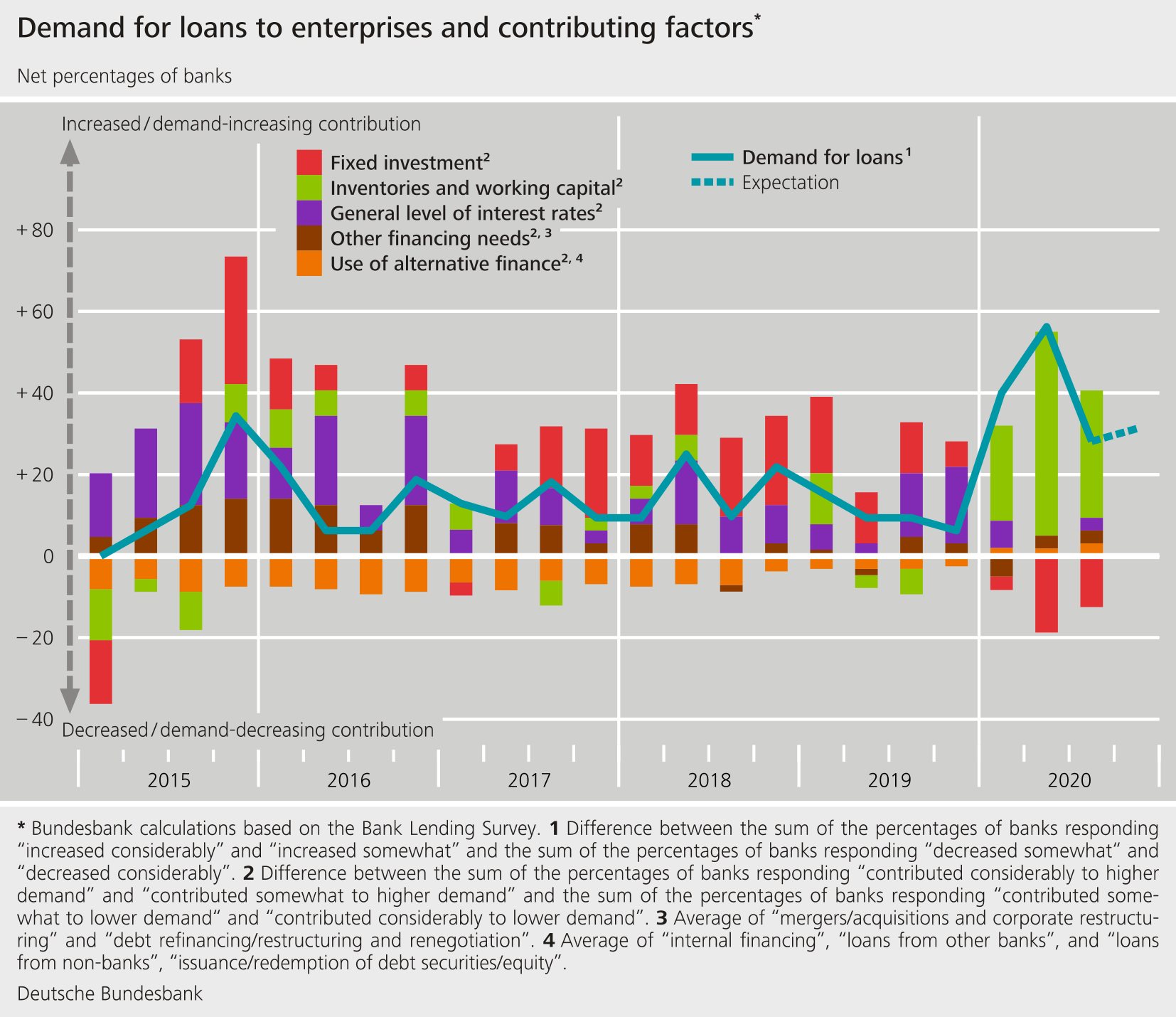

- Higher demand for loans to enterprises was reported once more. However, this fell short of the strong rise in the second quarter. Demand for loans for house purchase also went back up following the slump reported in the previous quarter.

- The banks reported a general improvement in their wholesale funding environment.

- The interest rate-reducing impact of the Eurosystem’s expanded asset purchase program (APP) and the Pandemic Emergency Purchase Programme (PEPP) weighed on banks’ profitability. At the same time, these programmes have contributed to an increase in loans for house purchase over the past six months.

- The negative interest rate on the deposit facility once again put a strain on banks’ net interest income. The negative earnings effect was tempered by the two-tier system for remunerating excess liquidity holdings, however.

- Banks’ interest in the third series of targeted longer-term refinancing operations (TLTRO-III) of June and September 2020 was higher than for previous series owing to the attractive design of these operations. The funds raised were mainly used for lending, the substitution of TLTRO-II funds and liquidity holding in the Eurosystem.

{kind=link}

{kind=link}

Demand for loans to enterprises continued to climb. However, as expected by banks, the increase failed to match the strong second-quarter rise. As in the previous quarter, the increase in demand was driven by high financing needs for inventories and working capital. Demand was also boosted by the increased need for funds for refinancing, debt restructuring and renegotiation of existing loans or credit lines. The bolstering of demand for loans to enterprises by the coronavirus aid programmes of the KfW Group and the promotional banks of the Länder abated somewhat in the third quarter. Demand for loans for house purchase rebounded following the slump in the preceding quarter. Banks responded to the increased demand for loans to enterprises and loans for house purchase with a relatively high rejection rate. It was enterprises from sectors especially hard hit by the crisis and new customers, in particular, which had poorer access to credit. On balance, banks reported no change in funding needs in the case of consumer credit and other loans. Over the next three months, banks expect a further increase in demand for loans to enterprises as well as for consumer credit and other loans. By contrast, they do not expect any change in the need for loans to households for house purchase.

The October survey contained ad hoc questions on banks’ funding conditions and on the impact of the Eurosystem’s expanded APP, including the PEPP. Other questions addressed the effects of the negative interest rate on the Eurosystem deposit facility and the two-tier system for remunerating excess liquidity holdings. The survey additionally contained questions on the Eurosystem’s third series of targeted longer-term refinancing operations (TLTRO-III).

Against the backdrop of conditions in financial markets, German banks reported an improvement in their funding situation compared with the previous quarter. Funding through debt securities, in particular, improved in all maturity segments. Over the past six months, the Eurosystem’s purchase programmes have helped to improve banks’ liquidity position and market financing terms. However, their impact on net interest income continued to weigh on banks’ profitability. It was only in the area of loans to households for house purchase where the programmes made a major contribution to credit growth. The negative interest rate on the deposit facility, too, once again made a negative contribution to the growth of banks’ net interest income. The interest rate-reducing impact on lending rates was more pronounced than the effect on deposit rates. Banks reported that the negative interest rate enhanced volumes significantly only in the case of loans to enterprises. The negative earnings effect was tempered by the two-tier system for remunerating excess liquidity holdings, however. 24 banks from the German sample participated in the TLTRO-III operation in June 2020, and 14 in the September 2020 operation. The last two operations thus encountered greater interest on the part of banks than the previous operations. Participation in the June and September TLTRO-III operations was chiefly due to their attractive design. The banks reported using the uptake in funds primarily for lending, the substitution of TLTRO-II funds and liquidity holding in the Eurosystem. The surveyed banks would participate in future operations as well, mainly because of the attractive design of TLTRO-III. The TLTRO-III operations had barely any impact on banks’ lending policies.

The Bank Lending Survey, which is conducted four times a year, took place between 21 September and 6 October 2020. In Germany, 34 banks took part in the survey. The response rate was 100%.