July results of the Bank Lending Survey in Germany

- The German banks taking part in the Bank Lending Survey (BLS) again tightened their lending policies in all surveyed credit segments (loans to enterprises, loans to households for house purchase, and consumer credit and other lending to households) in the second quarter of 2020.

- The banks tightened their lending policies for all major sectors of the economy in the first half of the year. For the second half of the year, they are planning to tighten their policies further for nearly all the sectors.

- The NPL ratio played only a marginal role in the tightening of lending policies in the first half of the year. The banks are expecting it to have a significantly more restrictive impact for the second half of the year, however.

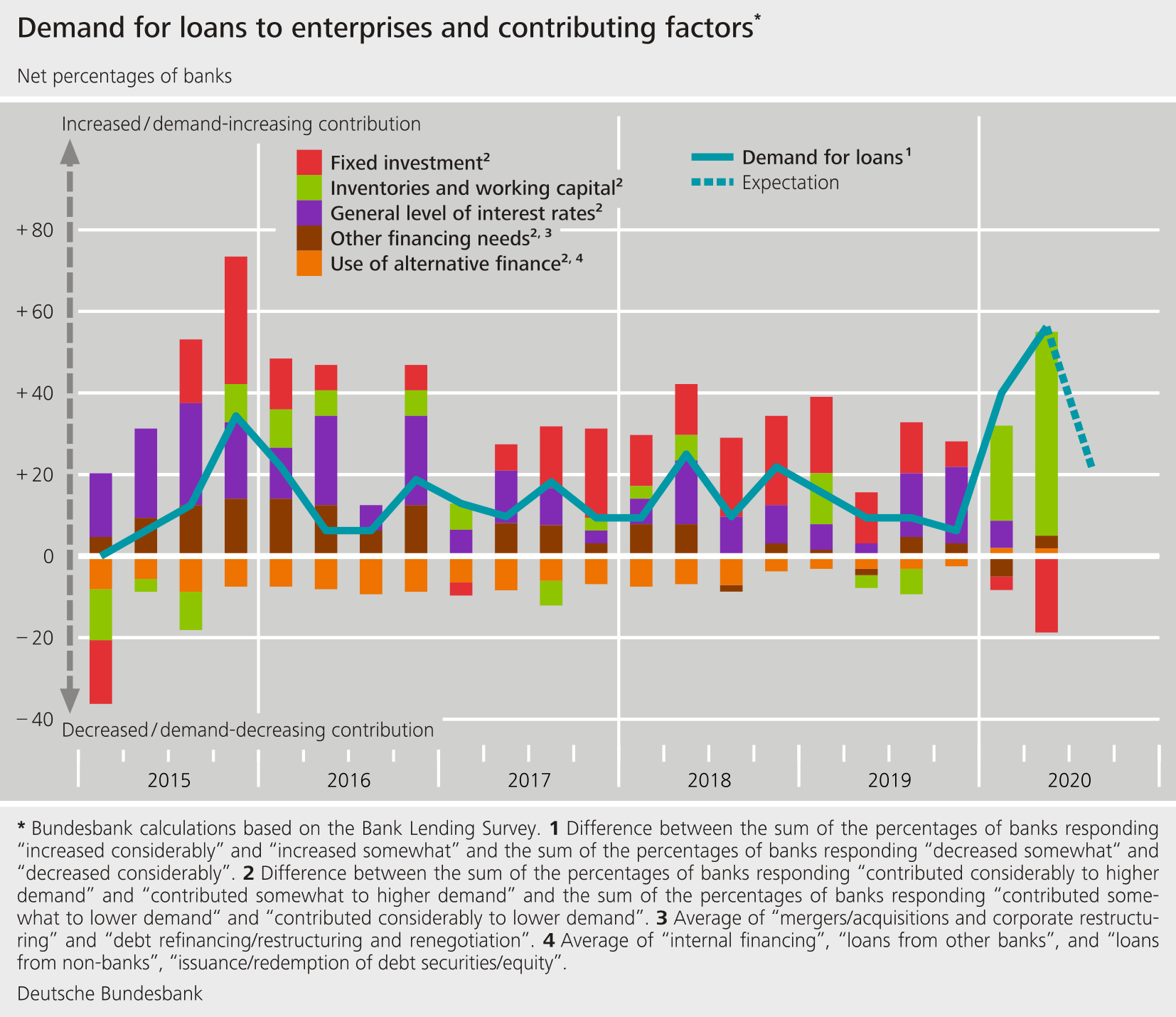

- There was a marked rise in demand for loans to enterprises; this was also boosted by the coronavirus aid programmes of the Kreditanstalt für Wiederaufbau (KfW) and the promotional banks of the Länder. The banks are expecting an increase in demand in the coming three months as well.

- Demand for loans for house purchase fell for the first time since 2017.

- The banks reported a general deterioration in their funding environment.

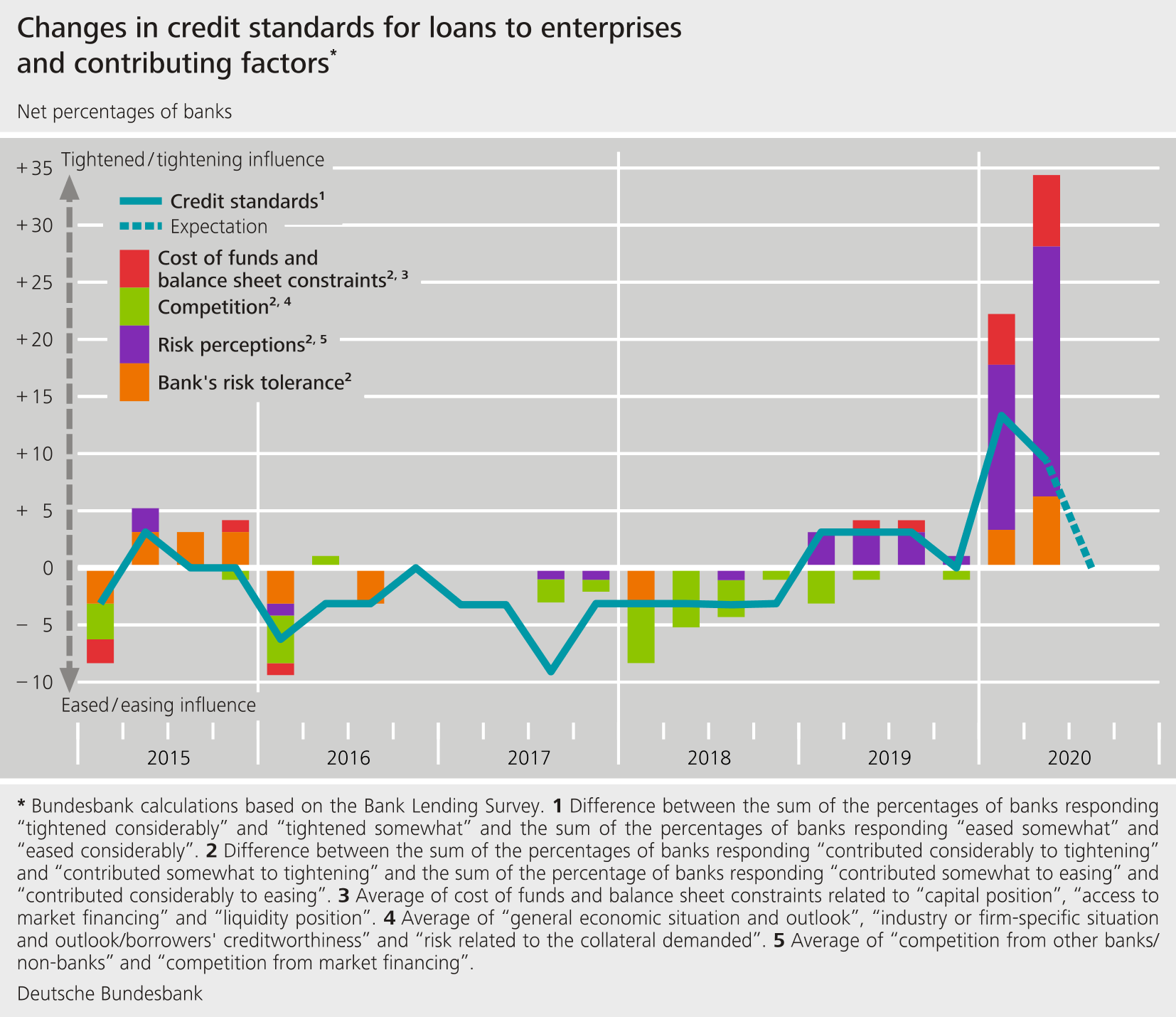

The BLS covers three loan categories: loans to enterprises, loans to households for house purchase, and consumer credit and other lending to households. The surveyed banks tightened their credit standards (i.e. their internal guidelines or loan approval criteria) for loans to enterprises on a larger scale once again (a net percentage of +9% of the surveyed banks, compared with a net share of +13% of the banks which tightened their standards in the previous quarter). The impact of the pandemic was also reflected in tighter credit standards in the case of loans to households for house purchase (a net percentage of +21% of the surveyed banks, compared with +3% in the previous quarter) and in consumer credit and other lending (a net percentage of +20% of the surveyed banks, compared with +10% in the previous quarter). For the coming three months, the banks are not planning any significant changes in standards in any of the surveyed segments. At the same time, the surveyed institutions tightened their terms and conditions (i.e. the actual terms and conditions agreed in the loan contracts) in all surveyed lines of business. Institutions cited the fact that credit risk was rated higher and lower risk tolerance as the main reasons for tightening credit standards and credit terms and conditions. In the case of loans to enterprises, a deterioration in banks’ wholesale funding costs and balance sheet constraints also contributed to the tightening.

{kind=link}

{kind=link}

Against the backdrop of conditions in the financial markets, German banks reported a broad deterioration in their funding situation. In particular, banks assessed access to the short-term unsecured interbank money market and funding through medium to long-term debt securities as poorer than in the previous quarter. The surveyed banks reported that the size of the NPL ratio (percentage ratio of (gross) non-performing loans to the gross book value of the loans) nevertheless made no more than a marginal contribution to a tightening of their lending policies in the first half of 2020. For the second half of the year, the banks are anticipating a significantly more restrictive impact, however, especially in the case of loans to enterprises. In the first half of the year, the interviewed banks tightened their lending policies for all the surveyed economic sectors. For the second half of the year, they are planning a further cross-sector tightening of their lending policies. One exception to this is the residential real estate sector, where an easing of credit conditions is planned. Loan demand increased in all sectors in the first six months of this year. For the next six months, the banks are anticipating a further rise in demand in the manufacturing sector. For the other sectors, they are expecting the demand for borrowing to remain very largely unchanged. Given the possibility of a resurgence of coronavirus infections from autumn onwards, uncertainty among banks is very high with regard to ongoing demand up to the end of the year.

The Bank Lending Survey, which is conducted four times a year, took place between 5 June and 23 June 2020. In Germany, 34 banks took part in the survey. The response rate was 100%.