January results of the Bank Lending Survey in Germany

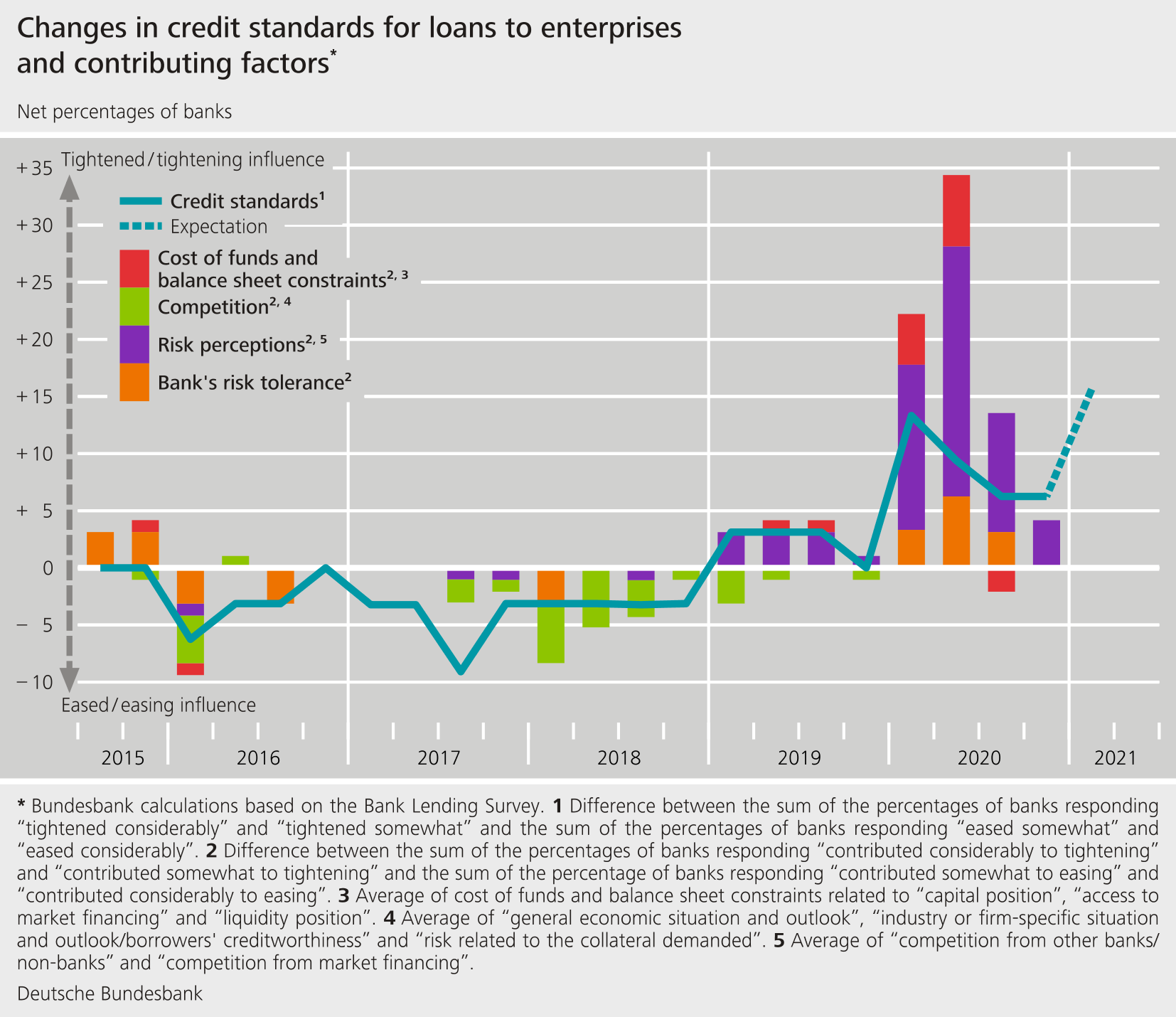

- The German banks responding to the Bank Lending Survey (BLS) once again tightened their lending policies in loans to enterprises in the fourth quarter of 2020. The standards for loans to households for house purchase remained unchanged.

- The actual terms and conditions for loans to enterprises and to households for house purchase were likewise tightened. This was reflected (primarily) in widening margins.

- The NPL ratio played only a marginal role in the tightening of lending policies in the second half of the year. The banks are expecting it to have a significantly more restrictive impact in the first half of 2021, however.

- The surveyed banks assume that enterprises used government-guaranteed loans extended under coronavirus assistance programmes chiefly to meet acute liquidity needs and for liquidity provisioning purposes.

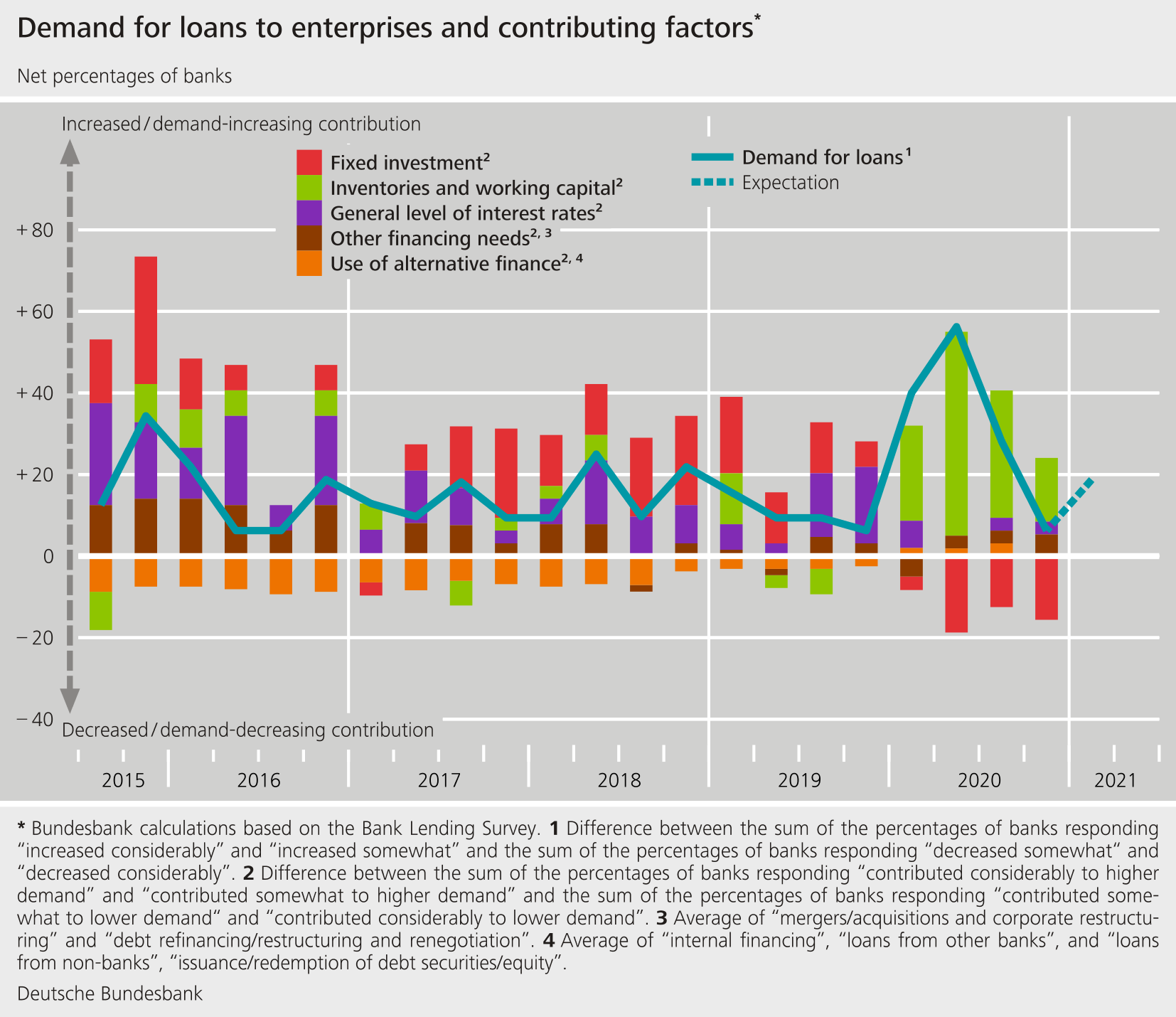

- Demand for loans to enterprises and for house purchase continued to rise.

{kind=link}

{kind=link}

The January BLS round contained ad hoc questions on the banks’ funding conditions and the impact of the new regulatory and supervisory activities (including the capital adequacy requirements defined in CRR/CRD IV and the requirements resulting from the ECB’s comprehensive assessment), as well as on the impact of NPLs on banks’ lending policy. It also contained a question on lending policy and loan demand in the key economic sectors as well as, for the first time, a question on loans with COVID-19-related government guarantees.

Against the backdrop of conditions in financial markets, German banks reported an improvement in their funding situation compared with the previous quarter. Funding through debt securities and in the unsecured money market, in particular, improved. In the wake of the new regulatory and supervisory activities, banks continued to strengthen their capital position last year. The surveyed banks reported that the size of the NPL ratio (percentage ratio of (gross) non-performing loans to the gross book value of the loans) made only a marginal contribution to a tightening of their lending policies in the second half of 2020. In the first half of 2021, however, banks are anticipating an increase in the restrictive impact, especially with regard to loans to enterprises. In the second half of the year, the interviewed banks tightened their lending policies for all major economic sectors. Credit standards for government-guaranteed coronavirus assistance loans were eased in 2020 in contrast to those for normal loans. Such loans were in demand in order to meet acute liquidity needs and to build up precautionary liquidity buffers.

The Bank Lending Survey, which is conducted four times a year, took place between 4 December and 29 December 2020. In Germany, 34 banks took part in the survey. The response rate was 100%.